“It does not matter how slowly you go so long as you do not stop.”

-Confucius

I started making short sales into yesterday’s US stock market close by re-shorting Spain (EWP) and US Industrials (XLI). During last week’s market down moves to fresh YTD lows I was on the sidelines from a short selling perspective. On market rallies, my strategy has been to start shorting slowly.

There is no other way to explain why I do what I do other than to tell you I have learned how to play this short selling game by doing. In my mid-20’s (the year 2000) I was tasked by a major hedge fund in Connecticut to do one thing – make money. Given that my first 3 years managing risk with real-ammo were in down markets (2000, 2001, and 2002), I learned pretty quickly that the primary path towards making money was not losing it.

A lot of people lose money in down markets. Then they blame a “great depression” or something that “everybody missed.” The truth is that most people aren’t experienced/competent short sellers. I have witnessed this both in analyzing the short selling processes of former colleagues and by generally observing markets. In order to make money on the short side, you have to trade.

From a purist “long term” investor’s perspective, “trading” is often considered a bad word. It doesn’t quite fit the storytelling in the marketing flip book that some asset managers who are too big to perform need to uphold. I use this modern day institutionalization of Duration Dogma to my advantage.

This isn’t to say that I am always right on the short side. I’m more focused on not losing money than anything else and that’s just how I think about risk management. As the interconnectedness of global markets continues to drive volatility in daily prices, I need to change our positioning alongside that. As far as I know, the only way to change a position in your portfolio is to “trade” it.

Let’s go back to the top and consider a real-time example of managing risk around what I consider a “core” Hedgeye 2010 short position – shorting Spain (EWP). For practical transparency/accountability purposes, here are the 3 most recent time stamps in the Hedgeye Virtual Portfolio:

- 5/18/10 re-shorted EWP at $34.74

- 5/24/10 covered EWP for a gain at $33.47

- 7/7/10 re-shorted EWP at 331PM EST at $36.93

What you should quickly notice here is that as bearish as Daryl Jones and my Macro Men were on Spain in Q2, I wasn’t able to hold onto the short position and pick the bottom (the EWP put in a YTD low at $30.14 on June 7th, a few weeks after I covered our short position).

What you’ll also notice is that I didn’t get squeezed for the +23% rally in the ETF from that June 7th low to yesterday’s close or the +12.5% rally we saw in the local Spain stock index (Spain’s IBEX YTD low was registered on 6/8/10 at 8869).

Altogether, the absolutist in me is satisfied with the outcome – we didn’t lose our clients’ money by adhering to the “this is our best idea, so we are going to let it ride because we are smarter than you” strategy. Short-And-Hold is not a long term risk management process. Shorting for absolute return is.

Shorting Slowly is another way to communicate how I think about getting back into short positions that I’ve recently covered with accurate, rather than emotional, timing. When you are bearish in a market that’s going up like yesterday’s did, the hardest thing to do is not hit the SHORT button.

I think I am sufficiently bearish (email for the slides we have on our Q3 Bear Market Macro theme). But that doesn’t mean I have to be short the SP500 (SPY) at any price. I wasn’t short the SPY for yesterday’s +3.1% melt-up and I’m not short it this morning either. I am waiting and watching.

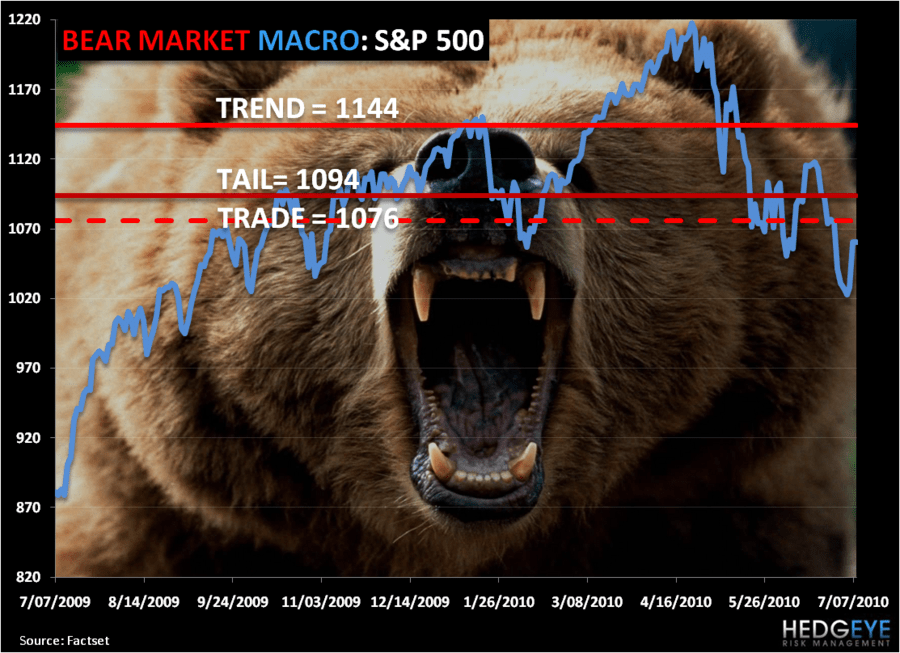

What am I waiting and watching for? That’s easy – time and price. Across all 3 of the Hedgeye Risks Management durations (TRADE, TREND, and TAIL), the SP500 is broken – we call this a Bearish Formation and here are the lines that matter:

- TRADE = 1076

- TREND = 1144

- TAIL = 1094

So, why not wait and watch for my most immediate term line of resistance (1076) to confirm that this market is immediate term bearish from a TRADE perspective before I hit the button? I guess if you don’t have a line, it’s harder to adhere to planning your risk management process this way.

Most of yesterday’s melt-up in the US stock market has to do with the gravitational forces associated with chaos theory, not a Buy-And-Hope forecast by a conflicted IMF that both US and global economic growth is setting up to accelerate. Bear markets often bounce higher than bull markets do.

It’s mathematically impossible for us to get to this IMF 2010 GDP forecast for the US of 3.3% (upped from 3.1% last night) unless growth accelerates in the back half of the year. Don’t forget that Q1 GDP for 2010 was recently downwardly revised to 2.7% and 1.9% of that 2.7% was inventories. Our Q3 estimate for US GDP growth is 1.7% and this is why we shorted the Industrials (XLI) instead of another sector in the US into yesterday’s close.

On yesterday’s strength (which was the 1st up day of more than +0.54% in the last 12 - hooray) I sold all of our US Equity exposure in the Hedgeye Asset Allocation Model again taking our allocation to US stocks back to the “risk free” rate of return that the US Government is promoting – ZERO percent.

My immediate term support and resistance lines for the SP500 are now 1005 and 1076, respectively. If you’re looking to get short out there today, take your time and short slowly.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer