For the last weeks we’ve been staring at the outperformance of the Ukrainian equity index, PFTS, which has held the top spot in year-to-date performance among global indices, and currently stands at +39.5% YTD.

While we expect that Ukraine’s equity market is not front and center on your screen, the country did make headlines yesterday after Fitch Ratings upgraded Ukraine’s sovereign credit grade one step to B from B-. More broadly, Ukraine, much like Hungary and Romania, has jockeyed with the IMF over funding to maintain its “fiscal and financial stability” over the last months. And while its lifeline with the “West” is important for market confidence, it’s clear that Ukraine’s attention is to the East, despite recent efforts by the US to “reset” relations with Moscow and the former Soviet states. Note that Secretary of State Hilary Clinton visited Ukraine’s President Viktor Yanukovych last week on a five-nation tour that also included Poland, Azerbaijan, Armenia, and Georgia.

Washington may be playing a game of catch-up it can’t win.

Irrespective of Washington’s goals, the election of Moscow-backed Yanukovych in February of this year has set the political tone for the country, one in which the Kremlin is pulling the strings. In that light, President Yanukovych has abandoned his predecessor’s commitment to join the North Atlantic Treaty Organization (NATO) and secured gas subsides with President Medvedev that should bring an end to gas disputes for him at home. (Remember the critical role Ukraine plays as the main transit supplier of Russian gas to Europe, moving up to 80%, with the remainder channeled via Belarus.)

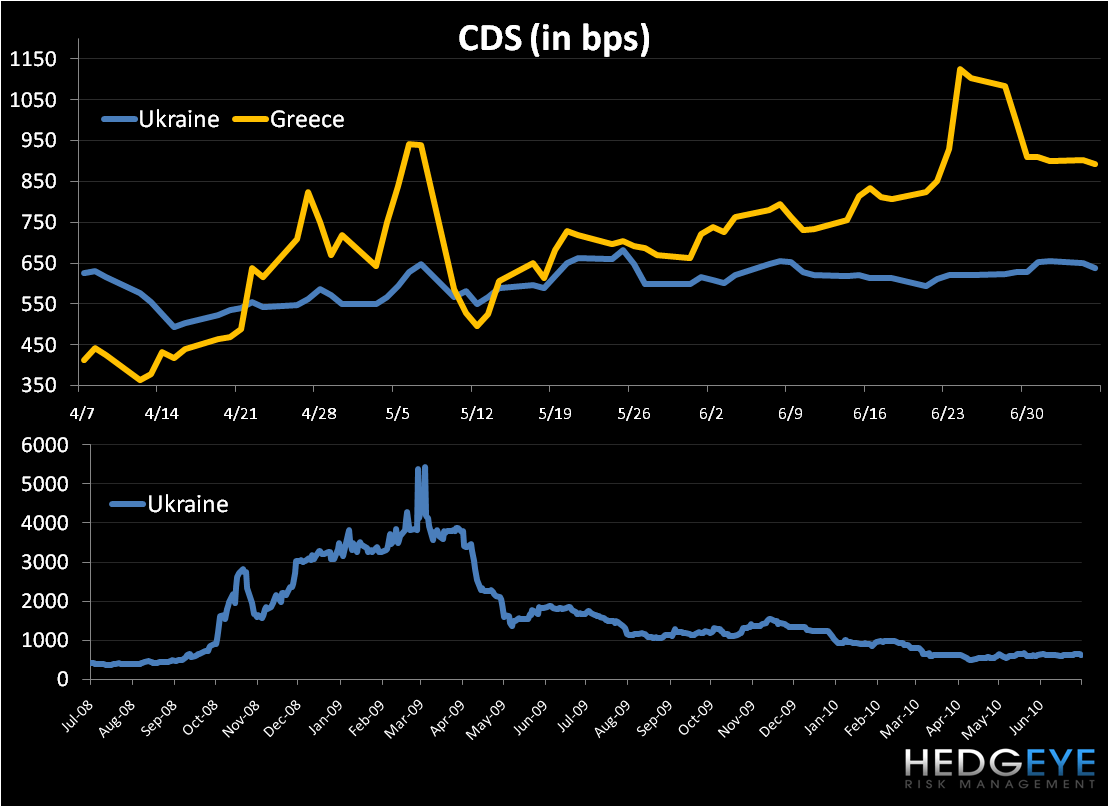

Perhaps it is the confluence of optimism from an agreement with the IMF on July 3rd for a new $14.9 Billion loan tranche; the hope of the country's upcoming road show for its first Eurobond sales since 2007 (to raise $1.3 Billion); and a more secure geopolitical environment with its near unilateral ties to Moscow, which could continue to drive Ukraine’s equity market and local currency, the Hryvnia, higher. The charts below give context to the equity and currency moves over the last three years, while CDS prices indicate a waning in the risk premium YTD.

After the economy slid 15.1% last year, Fitch expects the economy to expand 4.5% this year, driven by stronger external demand. We don’t have an investment position in Ukraine, but monitor the country due to its geopolitical impact.

Matthew Hedrick

Analyst