While there is precedent for a lower multiple, we think the Street is too low on margins. The next year should validate the Board’s decision to replace Dan Lee.

Why is PNK getting demolished? Potential exposure to the Gulf oil spill, an economic wall of worry, high leverage, Baton Rouge concerns, a lousy May in the regional markets; the list goes on and on. The stock is down almost 40% in two months with no real announcements from the company. That brings the valuation multiple down to 6x our 2011 EV/EBITDA. One could take it a few steps further and point out that multiple includes $50 million in capex related to the construction of Baton Rouge (almost $1 per share) and doesn’t include non-EBITDA producing assets such as BR, Reno, and AC land that we value at $200 million or over $3 per share of equity value.

So the stock is cheap. Blah, blah, blah. After the market nose dive, a lot of stocks are cheap. Besides, we’ve seen these regionals trade into the 5xs. There has to be catalysts to buy a cheap stock these days. We think better margins will be the main catalyst this year and next, although a completely revamped marketing program could boost top line as well.

Earlier this year, the PNK Board replaced the developer/empire builder Dan Lee with the operator Anthony Sanfilippo as CEO. Mr. Sanfilippo, who has been buying stock recently, cut his teeth in the Harrah’s organization so he knows a little about database marketing. He also seems to know a little about cost cutting. We detailed the cost cutting plan first back in April in our Q4 earnings preview note so we don’t want to rehash the components here. We did see evidence of the plan in Q1 where PNK surprised on the upside due to margins.

In looking at the following charts the potential for margin improvement is obvious. We’ve compared PNK to the other pure regional gaming operators in terms of overall EBITDA margin and a more apples to apples comparison of EBITDA margin less gaming taxes. PNK under Dan Lee clearly trailed the industry in this very important metric. The other companies began to cut costs in 2008 when the industry turned, so their margin comparisons are much more difficult than PNK. ISLE probably has more room to cut, although there are structural issues with some of their properties. We believe PNK will still be comping against a higher cost structure through 2011.

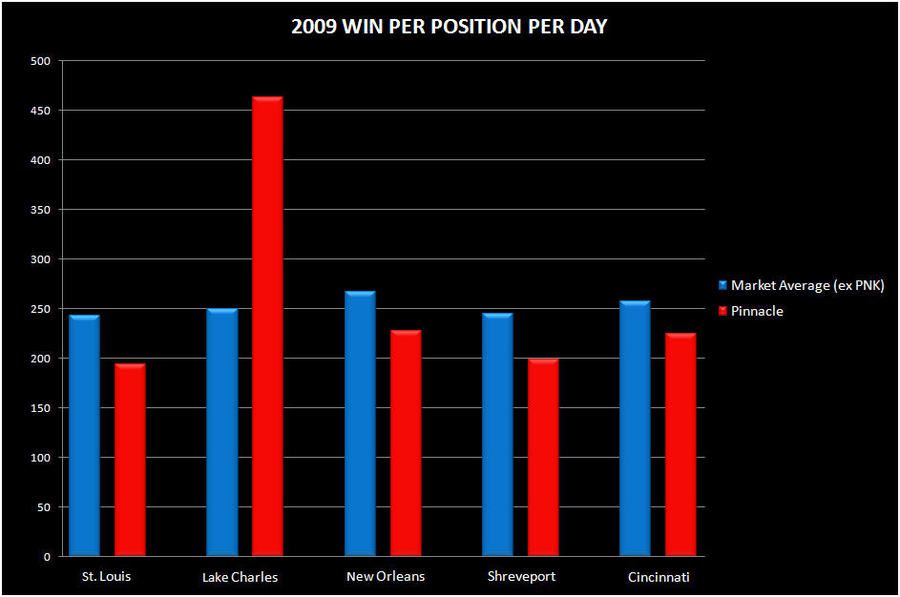

As we mentioned, cost cutting shouldn’t be the only area of significant improvement. Marketing is Mr. Sanfilippo’s specialty. The chart below shows that PNK has trailed the industry on the operating side as well. It compares PNK’s revenue per position in each of its major markets to the competition. With the exception of PNK’s L’Auberge, PNK trails the market badly in win per position per day, presenting significant room for improvement for a good operating team. L’Auberge, of course, is a much newer and better product than the weak Lake Charles competition.

We understand the market’s concern surrounding consumer spending in general and very discretionary gaming spend in particular. Meaningful leverage only adds to the risk. At least PNK has a few major levers left to pull vis-à-vis the rest of the industry. Of course, if the economy double dips, no casino operator will emerge unscathed.