This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

There is a great fuss and bother in Washington about whether the Federal Reserve Board should “allow” banks to pay dividends to their shareholders. Even former FDIC Chairman Sheila Bair has gotten into the act, saying that we don’t know "how bad things will get."

Of course, none of the people worried about bank dividends offer any numbers or analysis to put an actual scale to the worry. In this issue of The Institutional Risk Analyst, let’s see if we can help, yes?

As we’ve noted in past comments, merely ending bank share repurchases is worth about $130 billion per year of capital retention for the 125 members of Peer Group 1, which is basically every bank above $10 billion in total assets.

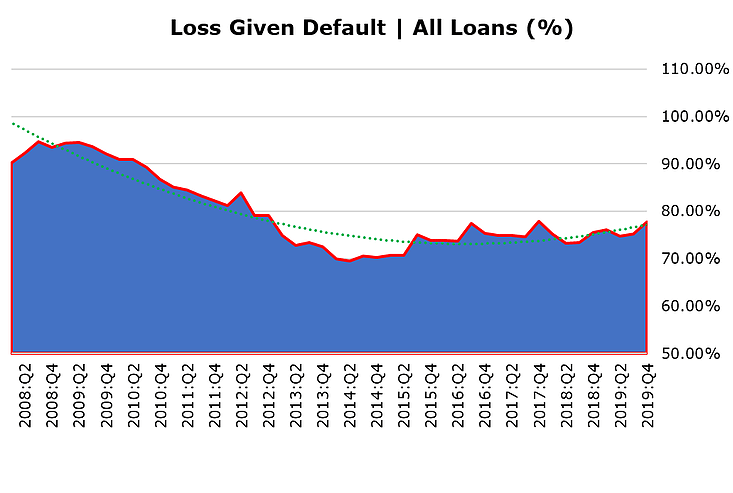

Between Q4 of 2008 and Q4 of 2009, US banks charged off $116 billion on total loan losses net of recoveries. Net charge offs as a percentage of total loans and leases topped out at 3% in Q4 of 2009. Loss given default on all US banks climbed into the 90% range, but quickly fell as the economy and property values recovered through the 2010s, as shown in the chart below.

So, let’s assume for a moment that the great COVID19 lockdown is going to drive up bank loan loss rates to 2x 2008 levels. Loss rates on residential exposures will probably be a lot lower than some of the worst-case scenarios, but multifamily and commercial loan exposures seem destined to blow out previous metrics for net loss rates.

Loss severities on some smaller multifamily residential and commercial properties could exceed 100%, suggesting that abandonment may become a problem in some localities. Yet despite the horrific unemployment figures, the credit losses could be lower than expected because low income households don’t use much credit. The chart below shows historic data from the FDIC and our best guess for the rest of 2020.

If US banks see loan loss rates rise to 2x 2009 levels, does that mean that banks will need to suspend dividends? Maybe. First, in addition to the cash available from ending share repurchases, the US banking industry has about $50 billion in quarterly income to use to fund provisions. Call the total funds available per quarter $80 billion. Should banks still suspend dividends? Maybe, but not because of some bureaucratic edict from Washington.

Some banks may choose to cut dividends, but other may just go to the market and raise equity. There are more than a few large banks still trading above book value, so issuance is something we should expect in coming months. Members of The IRA Bank Dead Pool, however, are unlikely to be in the markets raising common equity anytime soon.

Each bank is best able to assess its own credit loss profile and act accordingly. Banks with lots of consumer exposures such as Capital One (COF) as well as Citigroup (C) may see higher loss rates than in 2009, when net charge off rates for credit cards peaked about 10% for the industry. Given the current levels of unemployment nationally and dislocation visible in many sectors, we could easily see consumer loss rates for banks well above 2009 levels. Here's an idea: Rather than asking some bureaucrat in Washington, let’s let the market decide.

If your bank’s equity is trading below book value over the previous 90 days, then you must suspend dividends and build capital. Hopefully that will satisfy our favorite left-wing Republican from Kansas. Hey, we could leave this rule in place permanently and suspend the Fed’s annual stress test circus. If your bank’s stock trades at a premium to book, you may pay dividends.

Zombie Love

Meanwhile at Deutsche Bank AG’s (DB) New York unit, the hits just keep on coming. Laura Noonan of the FT last week reported that DB’s US unit, which happens to be one of the more important players in the world of custody and administration for agency mortgage loans, is still rated a “4” by federal examiners. In the world of prudential regulation, "1" is excellent, "3" is acceptable, and "4" is on the skids -- especially when you've been rated "4" or lower for years.

As we noted in our review of David Enrich’s new book (“Dark Towers: Deutsche Bank, Donald Trump, and an Epic Trail of Destruction”): “Everyone in the Federal Reserve System needs to read this book and ask a basic question: why was this bank not shut down? The simple answer is politics. The Fed and other agencies would not or could not do their jobs as required by US law for fear of the political ramifications in Germany.”

The question remains. The situation at DB is a classic example of moral hazard in operation. A smaller bank would have already been sold to another institution, but Deutsche Bank Trust Co of New York continues in operation. The list of material weaknesses in the bank’s operations is long and apparently has been unresolved for years, according to one executive close to the matter. Deutsche Bank apparently either cannot or will not comply with US law and regulation, yet the Federal Reserve Board refuses to act in an area where it has primary responsibility.

American regulators should have nothing further to say about bank capital or safety and soundness until the DB situation is resolved with finality. As we wrote in January 2020 in our IRA Bank Profile of DB: “We view the prospect of DB doubling down in markets such as investment banking and CDS trading with alarm and wonder whether prudential regulators in the EU and the US fully understand the implications of the latest strategy pronouncements by DB’s leadership.”

While some may see the Fed’s leniency as a sign of political conflict due to the continuing business ties between Deutsche Bank and President Donald Trump, in fact the reasons are far more profound. Were the US to follow its own laws and force the sale or wind down Deutsche Bank’s US operations, the ramifications in European markets would be extremely serious.

With Europe’s banking system already hanging by a thread in terms of capital and profits, the demise of DB would force a wholesale consolidation of EU banks into several explicitly state supported zombies. You can be pretty sure that German Chancellor Angela Merkel does not want to see a state rescue of DB as the last chapter of her glorious political career.

Moving from the sublime to the truly silly, last week saw a bit of a ruckus in the financial media when an enterprising member of the press decided that Goldman Sachs Group (GS) was considering a merger with the likes of U.S. Bancorp (USB) and PNC Financial (PNC).

Not going to happen in our lifetime. Let us count the reasons. First, none of the largest depositories have any interest in acquiring the GS franchise, even at a significant discount to current market value. While many businesses go at a premium to book value in acquisitions, in this case GS would go at a discount to partially compensate for the numerous known unknowns.

Like DB, GS is a vile risk sandwich of indeterminate size and condimentation. The idea of the board members of USB or PNC approving the acquisition of GS is fanciful. Second and more important, the situation at GS with respect to what is perhaps the largest fraud scandal in modern history remains unresolved. Andrew Cockburn writes in Harpers in “The Malaysian Job: How Wall Street enabled a global financial scandal”:

“Beginning in 2009, billions of dollars were diverted from a Malaysian sovereign-wealth fund called 1Malaysia Development Berhad (1MDB) into covert campaign-finance accounts, U.S. political campaigns, Hollywood movies, and the pockets of innumerable other recipients.” Third and perhaps more important, we doubt that the Federal Reserve Board would allow the principals of GS to play a significant role in the management of a larger depository.

As we tweeted to Charles Gasparino at Fox News last week, GS has barely $100 billion in core deposits underneath $1 trillion in miscellaneous assets and the largest derivative book on the Street in relative terms.

The GS business has uneven profitability, poor core funding and outsized risk factors, making it problematic from the perspective of federal regulators. We see a combination between Deutsche Bank and JPMorgan Chase (JPM) as more likely than a voluntary combination between GS and any other bank. One exception might be a white knight rescue of GS by Morgan Stanley (MS), but that is about the only possibility we see.

Of course we could merge GS and DB together and move the officers and directors to a Caribbean island with no electronic access, plenty of fresh water and gear for surf fishing. Instantaneously, the financial world would become a safer if less interesting place.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington.

This piece does not necessarily reflect the opinion of Hedgeye.