Last week, 6 of the 8 risk measures registered negative readings on a week-over-week basis, while one was neutral and one was positive

Our risk monitor looks at the following metrics weekly:

1. CDS for all available US Financials (30 companies).

2. High Yield

3. Leveraged Loans

4. TED Spread

5. Journal of Commerce Commodity Price Index

6. Greek Bond Spreads

7. Markit Subprime Spreads

8. AAII Bulls/Bears Sentiment Survey

1. Financials CDS Monitor – Moves in swaps were more modest last week than typical over the last few months, but nevertheless worsened week-over-week. Spanish banks saw the greatest improvement. On the domestic side, only MMC came in (by a single basis point) while all other companies increased. Conclusion: Negative.

Contracted the most vs last week: SAN-ES, BBVA-ES, SAB-ES, POP-ES

Widened the most vs last week: CB, TRV, AIG, SLM

Contracted the most vs last month: AXP, COF, ALL, SAN-ES

Widened the most vs last month: MS, LNC, ACE, AGO

2. High Yield (YTM) Monitor – After improving significantly earlier in the month, High Yield rates rose 17 bps last week. Rates closed the week at 9.06% up from 8.89% the week prior. Conclusion: Negative.

3. Leveraged Loan Index Monitor - Leveraged loans fell by 10 bp last week, closing at 1454 versus 1464 the week prior. Conclusion: Negative.

4. TED Spread Monitor - The TED Spread is a great canary. Last week, it diverged from the rest of the risk monitor, making it the only positive reading of our eight indicators. The TED spread fell, closing at 37 bps, down from 41 bps in the week prior. Conclusion: Positive.

5. Journal of Commerce Commodity Price Index – The JOC smoothed commodity price index is a useful leading indicator. A sharp sell-off in this index starting in July ’08 heralded further declines in the stock market. This week, the index fell from 15.21 the prior week to 9.84 on last Friday. Conclusion: Negative.

6. Greek Bond Yields Monitor – Greek bonds yields and CDS continue to show turmoil in the Aegean. Last week yields fell modestly, ending the week at 1021 bps versus 1042 bps the prior week. Conclusion: Neutral.

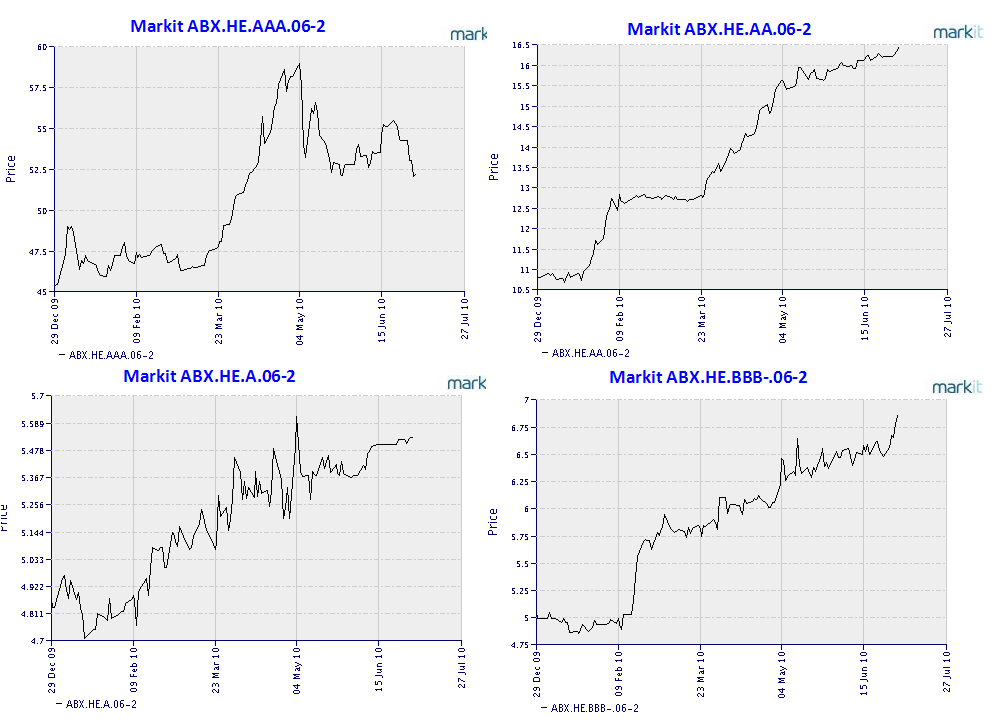

7. Markit ABX Index Monitor - We use the 2006-2 series and look at the AAA, AA, A and BBB- series. We include this measure as a reflection of what is going on in deep subprime distressed paper. The AAA fell sharply versus last week, while the other tranches were flat/slightly up. Conclusion: Negative.

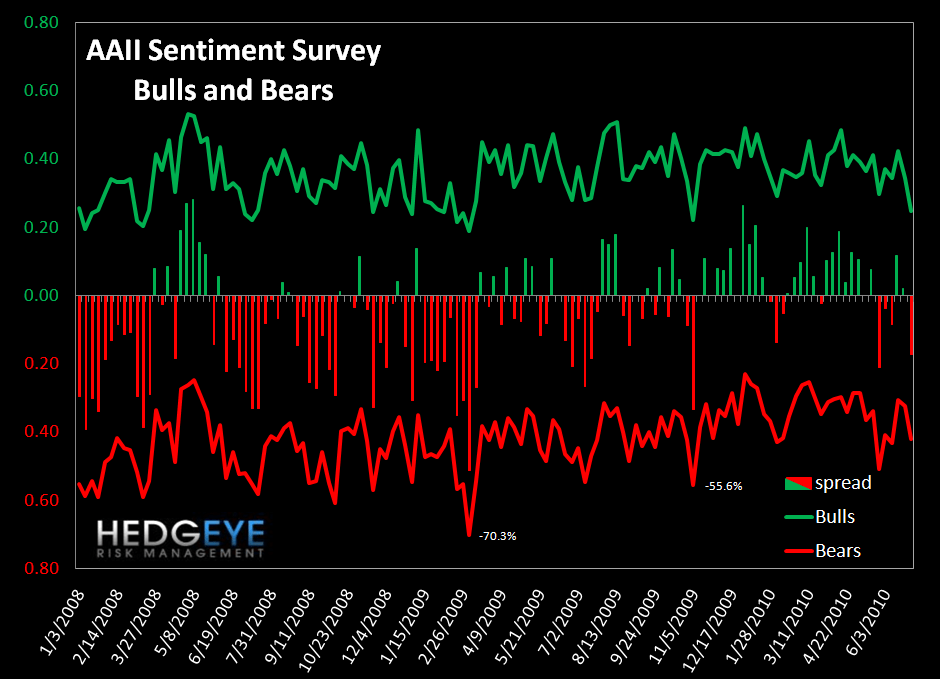

8. AAII Bulls/Bears Monitor - The Bulls/Bears survey grew more bearish on the margin vs last week. Bulls decreased by 9.8% to 24.7% while Bears rose 9.6% to 42%, pushing the spread to 17% bearish, versus 2% bullish the prior week. Conclusion: Negative.

One caveat is that our interpretation of the AAII Bulls/Bears survey is that a more bearish reading is bearish. Most market observers would use this survey as a contrarian indicator, which we wouldn't disagree with from a practitioner standpoint. However, for the purposes of this risk monitor, we treat an increase in bearish sentiment as a negative.

Joshua Steiner, CFA

Allison Kaptur