This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

|

“The very numbers you use in counting are more than you take them for. They are at the same time mythological entities (for the Pythagoreans they were even divine), but you are certainly unaware of this when you use numbers for a practical purpose.” - C. G. Jung (1961) |

Financials swooned this week as Federal Reserve Board Chairman Jay Powell rejected the idea of negative rates as a matter of monetary policy, that is to say, interest rate targets. Since the Federal Open Market Committee decided decades ago to turn the federal funds rate into a policy tool, the setting of interest rate targets and related signals has become the stuff of national fascination.

But like any benchmark, the significance of fed funds for financials has changed over time. Most important, Chairman Powell rejected the idea of negative interest rates, something we think is obvious but some economists cannot seem to appreciate.

The deflation that negative penalty rates imply clearly is antithetical to economic growth. Negative interest rates mandated by government are a tax, plain and simple, not a means to encourage growth. Negative rates shrink private capital leverage and growth possibilities to benefit the indebted state. Only heavily indebted nations could possibly find utility in a negative interest rate regime.

In mathematics and in the real world of people and commerce, natural numbers are those used for counting and ordering, the common means of accounting for global economic activity. In common mathematical terminology, those words used for counting are called "cardinal numbers" and words connected to ordering represent "ordinal numbers.” In the world of natural numbers, negative values do not exist independently and are, at best, derivatives of natural values.

Zero is a natural number and so too are the positive values that follow, but negative values have no place at all in the world of natural numbers or economics. Mathematician Leopold Kronecker (1823–1891) is reported to have said, “The dear God has made the whole numbers; all the rest is man’s work.”

Negative values do not exist in the natural world. You can possess nothing, or something more than zero, but in the real world you cannot have a negative quantity of something.

Why don’t many economists seem to understand these basic human distinctions when it comes to numbers? Beyond mere values, numbers impart qualitative aspects to social interactions that we call “markets.”

Numbers define value, enable commerce and compensate for work. Negative numbers retard these basic human functions. If an asset does not generate a positive return, no matter how small, then the asset has no value relative to the cash used to purchase it. Will the worker pay for the right to work? No. But fortunately, so long as the United States still has a private bond market, economists who have not been confirmed by the Senate will not be allowed to make such decisions.

Meanwhile, the process of value destruction and creation in the global capital markets proceeds apace, but there are also some opportunities. This is not nearly 2008 in terms of capital markets dysfunction and resulting litigation and nastiness. Instead, we are entering a process of plain old commercial defaults that will clog the arteries of finance and the bankruptcy courts for years to come.

This work will employ some members of the bar, but perhaps not in the custom they might expect.

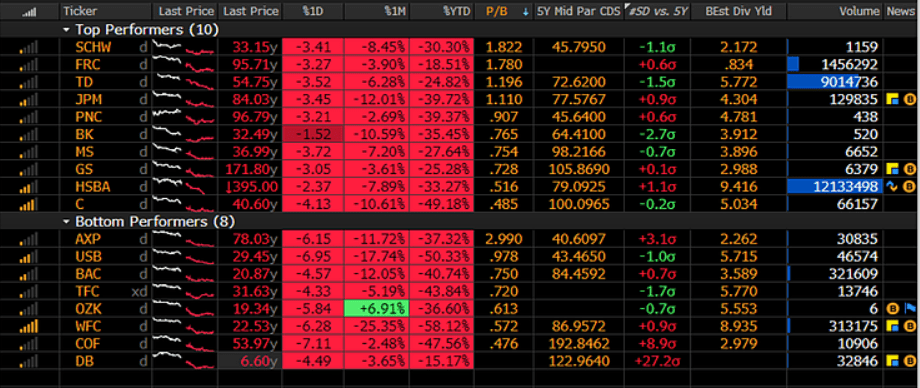

The spectacle of most major law firms cutting headcount and compensation is a leading indicator of tough days ahead. In the center ring, we have the large cap financials defending the post-selloff rally, but with little in the way of hope for the immediate future.

We cannot wait to see the Q1 2020 financials from the FDIC and FFIEC on the US banking industry. Suffice to say that the markets cannot discount what we cannot quantify. As we noted in our Q1 bank earnings report, the magnitude of loss facing US banks is larger in terms of the dollar of credit loss and broader in terms of the sector of the economy affected than in 2008. We expect to see early and frequent guidance from the major banks ahead of Q2 2020 earnings.

When the likes of Corelogic (CLGX) and Black Knight Inc. (BKI), data monopolies with a privileged view of the backend pipes in the world of asset backed securities, are competing for the most gruesome headline on forward residential loan defaults, it makes maintaining a positive outlook difficult but not impossible.

For you see, there are opportunities scattered amidst those steaming cow pies in the world of mortgage finance. Consider the world of mortgage servicing rights (MSRs). Our friend Joe Garrett at Garrett, McCauley & Co. in San Francisco put together this handy table of the Q1 marks for bank MSRs as reported by these leading residential mortgage issuer/servicers. In the past year, MSRs have lost about 1/3rd of their value due to interest rate volatility and related changes in assumptions about the maturity or option-adjusted duration of mortgage backed securities.

Notice that Mr. Cooper (COOP), which has excellent performance in terms of the recapture of loan refinance opportunities that come off its servicing book, has a relatively high multiple for the MSR. And by no coincidence, COOP is one of the better performers in the nonbank mortgage sector. Other nonbank lenders like Quicken, Freedom, Amerihome and PennyMac (PMT) are also very efficient at recapture.

The big banks don’t really make loans and therefore have little or no benefit from recapture, thus we see lower valuations for the large bank-owned MSR. But Flagstar (FBC) and U.S. Bancorp (USB) which we own, are in the middle in terms of recapture and thus market value of the MSR. It all comes down to this: Can you defend the value of your MSR by capturing mortgage loan refinance opportunities?

Now there is a school of thought that says that MSRs have no or even negative value due to the cost of forbearance as a result of COVID19 and the absurd mortgage payment holiday thrown into the CARES Act by Congress.

Yet even as investors focus on the temporary drop in servicing income due to loan forbearance, loan prepayments are also falling. Hmmm.... As and when loan prepayments eventually rise again due to accelerating mortgage refinance transactions, the new MSRs created in 2020 and beyond should have multiples that are higher than current vintages, especially for government insured loans in the FHA/VA/USDA markets.

Default rates on FHA loans will be high based upon the latest delinquency data, but each defaulted loan is also an opportunity for another gain-on-sale. Always look on the sunny side.... Just as negative interest rates are not a valid policy option for the FOMC, so too you cannot have negative rates on mortgage loans or mortgage servicing assets in a democratic, free market system.

The fascist states of Europe and Asia may be able to impose negative rates via government supported banks, but the US bond market is still a bit too large for the Fed to manipulate.

If the Fed tried to impose negative rates on private mortgage investors or loan servicers, the investors and lenders that populate the world of nonbank finance would simply go home. That is why we will not see negative interest rates in the US and why too there is a lot of value being created today in mortgage servicing assets.

Note in the FRED chart below, for example, that even as Treasury bond yields have dropped a point since February, 30-year mortgage rates have not followed.

Suffice to say that the compression in terms of valuation multiples for MSRs begins to approximate the similar crushing compression seen in both MBS coupons and Treasuries thanks to the Fed’s purchases since mid-March.

And yes, we did invoke the gods by asking the FOMC to buy GNMA 2s until the markets bled. And yes, they did. Thank you, oh Great Jay. Most operators in the mortgage sector fully expect to see GNMA 2s trading in TBAs by June. We can only say to the desk at the Federal Reserve Bank of New York: Be gentle with us.

Indeed, the system open market account (SOMA) will own about 40% percent of all agency mortgage securities by the end of 2020.

This is not a bad thing, but we’d only offer to the folks on Liberty Street that if the markets starts to strain in terms of collateral, sell the MBS back into the market demand. As in 2008 and 2018, lest we forget, the ability and willingness of the Street to support leverage is the key indicator of the true state of things.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington.

This piece does not necessarily reflect the opinion of Hedgeye.