As the consumer gets DUPE(d), consumer discretionary categories like casual dining will feel the pinch.

I think it is instructive to link Tuesday’s Early Look with the current picture we face when looking at restaurant stocks. “MEGA” was one of our Q209 macro themes – calling for a MEGA squeeze in consumer stocks with Mortgage Rates going down, the Employment picture turning around, Gas prices declining sharply year-over-year, and Asset prices re-flating. Looking at the data as we emerge from 2Q10, it is clear that the American consumer is now going to get DUPE (d) and is not going to be happy.

Double-Dip: The housing market and the broader economy are on the precipice of a double dip; housing prices have already started to decline and the economy has slowed significantly quarter-to-quarter in 1Q10. The Hedgeye Risk Management Financials team recently presented a very strong case for why the housing market is in trouble. We have high conviction that a double-dip in housing is underway and this will have a serious impact on consumer behavior. Following a decade of out of control spending, the state of the USA’s balance sheet inhibits the country’s ability to navigate the structural issues still present in the economy. Our Double-Dip thesis was supported by data released yesterday concerning mortgage applications; The MBA weekly Purchase Application Index released yesterday fell 3.3%, bringing June-to-date to 86.1 (versus April at 123.2 and May at 101.0). A few additional points to keep in mind include:

- The benefits from the current Obama stimulus peaked in the 1Q10 - Slowing GDP growth.

- In 2011, taxes are going up and that will hamper economic growth - Slowing GDP growth.

- Real estate prices are estimated to decline 20% in the next twelve months - Slowing consumer spending.

Unemployment: Weekly Jobless Claims have not shown any material improvement over the past six months. Private sector job creation remains a concern; private-sector job creation in May decreased sequentially from April. While private sector job creation had been growing for four straight months, it has now come to an impasse as businesses have become nervous about the state of the economy. Unemployment is at an elevated level and indicates a continuing softness in the underlying economy. Some data emerged yesterday is supportive of our view that the unemployment picture is not materially improving. According to ADP, US companies added a mere 13,000 jobs vs consensus 65,000. As census workers are laid off, the rate could jump higher unless other sources of employment pick up hiring drastically. This metric, of course, is of paramount importance to the restaurant industry’s top line.

- The Administration failed to get Congress to pony up an extra $50B for unemployment claims - our leveraged balance sheet inhibits the government’s ability to provide stimulus.

- A strong dollar policy has proven to help job creation – Bill Clinton and Ronald Reagan were the last two presidents to oversee true job creation and both pursued strong dollar policies - to be sure Obama is debauching the US currency.

- As the Double-dip scenario pays out, unemployment will remain elevated and may even go higher.

Prices Paid by the Consumer: While reported inflation by the government looks to be under control, the Hedgeye Inflation Index tells a different story. The Hedgeye Inflation Index focuses on the part of the economy showing inflation that impacts the consumer, specifically the spread between the prices of things they buy and what they earn. Looking out over the next 6-12 months (and even longer), consumers will be paying more to drive their cars, or “bring home the bacon” and to make sure they have health insurance for their family. The issues that arise from the disaster in the Gulf of Mexico will not be solved by the cash flow from BP. The government has been sponsoring cheap gas prices in the US for years and that will, at some point, come to an end. Once again, the government cannot afford to manage through the issues the country faces due to the highly-leveraged balance sheet.

- The Hedgeye Inflation Index turned ugly last week.

- The disaster in the Gulf is inflationary and will be a drag on growth.

- The prices paid by the US consumer for gas is far below the rest of the world and there is a possibility that the gap could close significantly under pending energy legislation – this would be a massive headwind for the consumer. Some commentators are speculating that prices could rise to meet those paid at the pump in Western Europe – some 50% higher than where they are currently.

Equity and Real Estate deflation: We believe that the debasing of any currency (even the Almighty Dollar) ends badly. A lack of austerity in government policies and an aversion to facing facts among our professional politicians is not helping the long-term outlook for equities. The VIX’s 19% up-move week-over-week, along with the move in the equity market, indicates that political summits are doing little to ease fears.

- U.S. equity markets have lost $1.78 trillion since April 23 on concern the European debt crisis will spread.

- China declined 4.2% last night and is now down 26% year-to-date.

- The S&P 500 is down 3.6% year-to-date.

The same metrics that buoyed the consumer over a year ago are depressing spending this year. As long as the data continues to confirm this thesis, we will continue to believe that the consumer is getting DUPE(d). Taking stock of performance in restaurant stocks over the past quarter, it is clear that the space is highly susceptible to the factors I have outlined above.

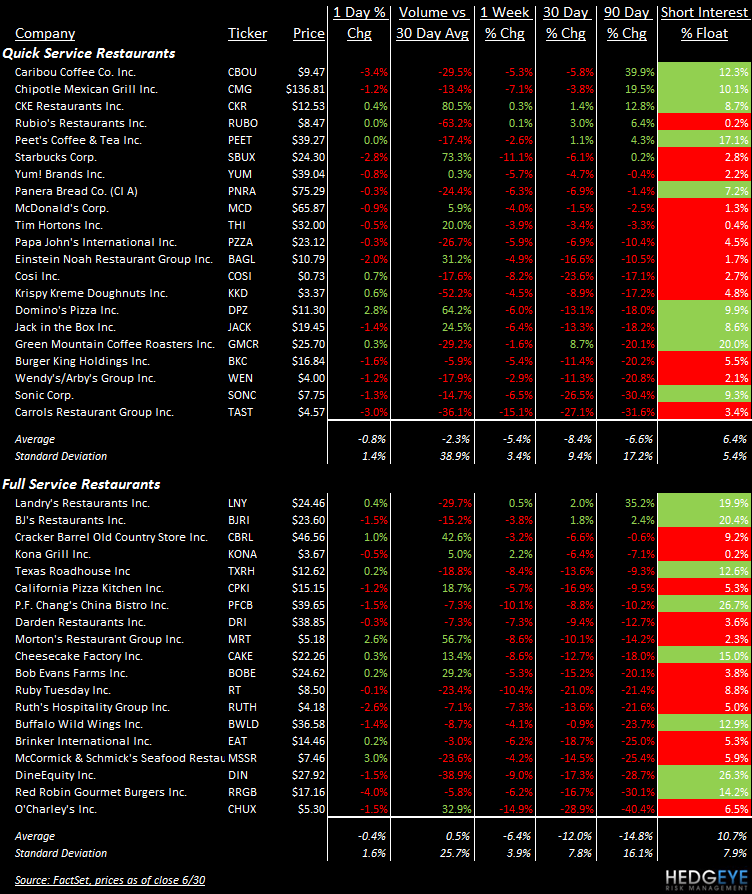

From the table below, one can see right away that it has been an ugly quarter for casual dining. Almost every stock in the category with the exception of Cracker Barrel, BJ’s Restaurants, and Landry’s (private) got hammered over the last quarter. Notably, in the table, from Bob Evans down to the bottom of the list (BOBE, RT, RUTH, BWLD, EAT, MSSR, DIN, RRGB, and CHUX) there are nine stocks that have declined by more than 20% over the last 90 days. Despite the precipituous declines, some of these companies are still facing serious issues (RRGB’s heavy dependence on promotions, BWLD’s terrible ROIIC due to unsustainable growth). With regard to EAT, we are maintaining our view that the company can take meaninful share from DIN and use their improved balance sheet (new revolver and proceeds of On the Border sales) to buy back ~25% of their market cap.

In terms of QSR, too, the poor outlook is certainly being confirmed by the price action. Chipotle has been unstoppable, up nearly 20% over the last 90 days, but has declined 4% over the past month. The QSR group on average is down nearly 6.6% over the past quarter. The “U” in DUPE(d) is highly relevant for the quick service category and, as I discussed above, the unemployment picture is not improving materially. QSR management teams have reiterated ad nauseum (Sonic Corp and Starbucks recently) the need for the unemployment picture to meaningfully improve if the topline is to grow.

Some recent news items include:

- CKE restaurants announced that its stockholders approved the proposal to adopt a merger agreement providing for its acquisition by “entities created by certain affiliates of Apollo Management VII, L.P.”.

- Brinker International and OTB Acquisition LLC, an affilliate of Golden Gate Capital, closed the sale of On The Border Mexican Grill & Cantina. Gross proceeds for the transaction total $180 million.

- Jack in the Box announced a five-year, $600M refinancing plan, comprised of a $400 million revolving credit facility and $200 million term loan.

- Starbucks is rolling out free WIFI in all US and Canada stores today.

- UBS raised its YUM price target to $49.

- CAKE upgraded to market perform from underperform.

- PFCB upgraded to market perform from underperform.

- CPKI mentioned in NY Post article detailing how, despite the capital gains tax increasing from 15% to 20% next year, private equity is not overly eager to spend. The CPKI auction, according to a source cited in the article, is near collapse and the restaurant company is an example of the lack of growth potential out there for PE to acquire.

- An interesting article in the Wall Street Journal titled, “USING STARBUCKS, DUNKIN’ DONUTS TO TRACK ECONOMY”, discusses the relationship between the state of the economy and where consumers buy their coffee and how much they are willing to spend. By breaking out the average dollar transactions at Starbuck’s and Dunkin’ Donuts, a research economist was able to identify a trend whereby consumers spent less at the outlets during the worst of the recession, but the spending on coffee ticked up as the unemployment picture improved. In April, the trend reversed but as the article notes, much of that change is likely to be seasonal.

- McDonald’s is changing its menu. The “Big N’ Tasty”, “Mac Snack Wrap”, and the fruit and walnut salad, among other items, are being crossed off the menu while an oatmeal breakfast will be rolled out nationally in January.

- Cosi, Inc., has announced that it has named Kimberly Letizia as its director of Culinary Innovation and Menu Strategy. Letizia most recently acted as Corporate Chef Consultant to Kraft Foods.

Howard Penney

Managing Director