Below are updates on our eighteen current high-conviction long and short ideas. We have added Chewy (CHWY) to the long side of Investing Ideas and Alibaba (BABA) to the short side of Investing Ideas. We have removed Facebook (FB) and Pinterest (PINS) from the short side of Investing Ideas. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

KR

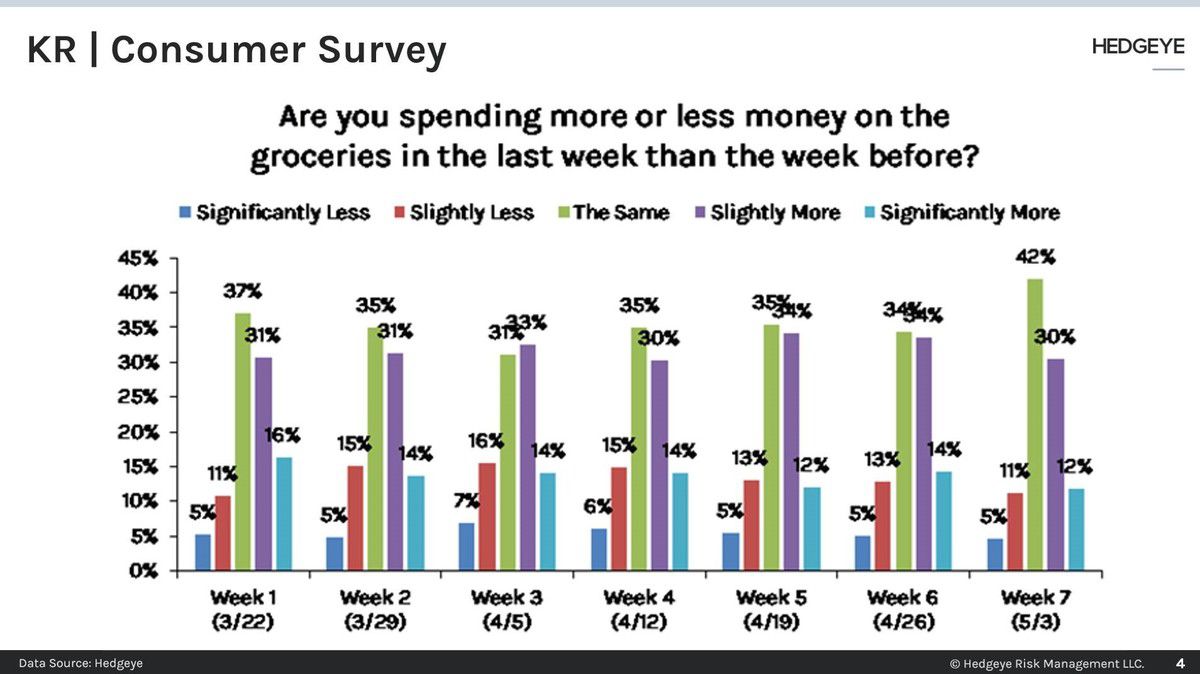

Our weekly consumer survey points to a decline in the number of consumers spending more on groceries – trending towards a new normal. 42% of consumers still say they are spending more on food at home than before, as seen in the chart below.

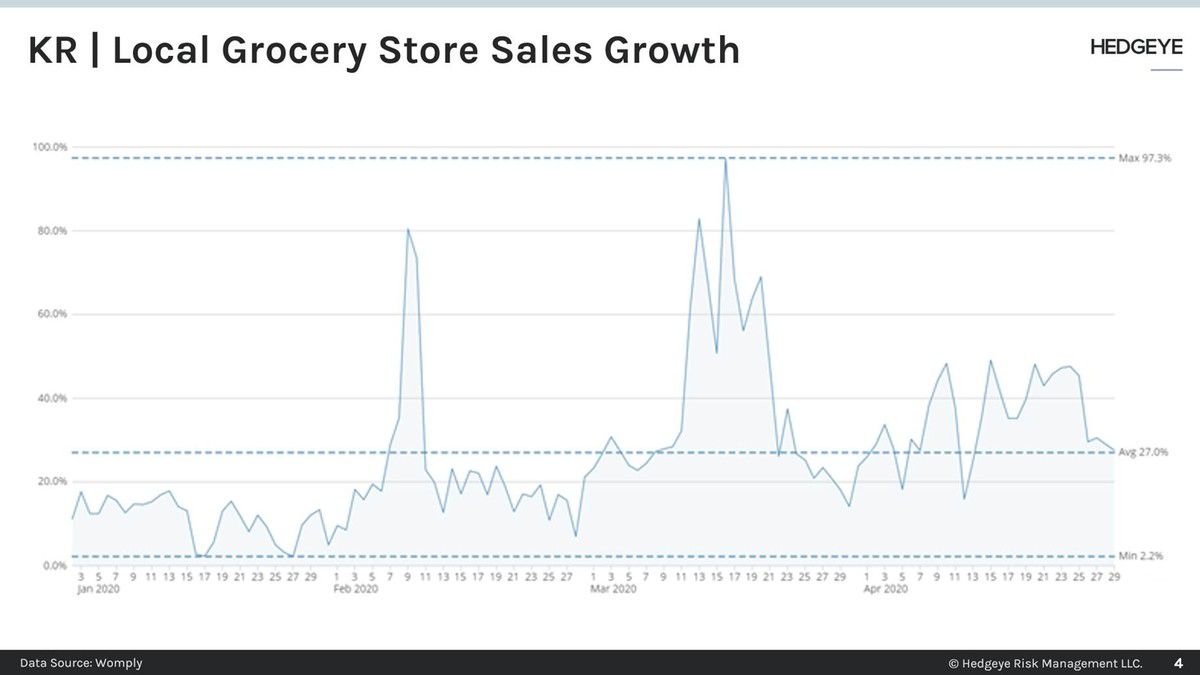

Local grocery stores have also seen a deceleration recently in sales, but to a still robust 27.5% YOY level as reported by Womply (CRM provider) in the following chart.

Ahold Delhaize, one of the largest food retailers in the world and operator of Stop & Shop and Food Lion in the US among other banners, reported SSS ex-gasoline of 13.8% in the US this week. Online sales grew by 37.7%. In the US, Jan. and Feb. comps grew 1.7% while Mar. comps grew 33.8%. US operating margins expanded 170bps to 6.7%. Management said they have been “positively surprised by how strong the sales continue to be [since the end of Q1].” The company expects margins to be lower in the rest of the year due to a more extended period of higher costs combined with less sales leverage than in Q1. Kroger (KO) is likely seeing many of the same industry trends as Ahold Delhaize. Grocery stores are benefiting from a shift to spending more on food at home which will last longer than the market is currently discounting.

GO

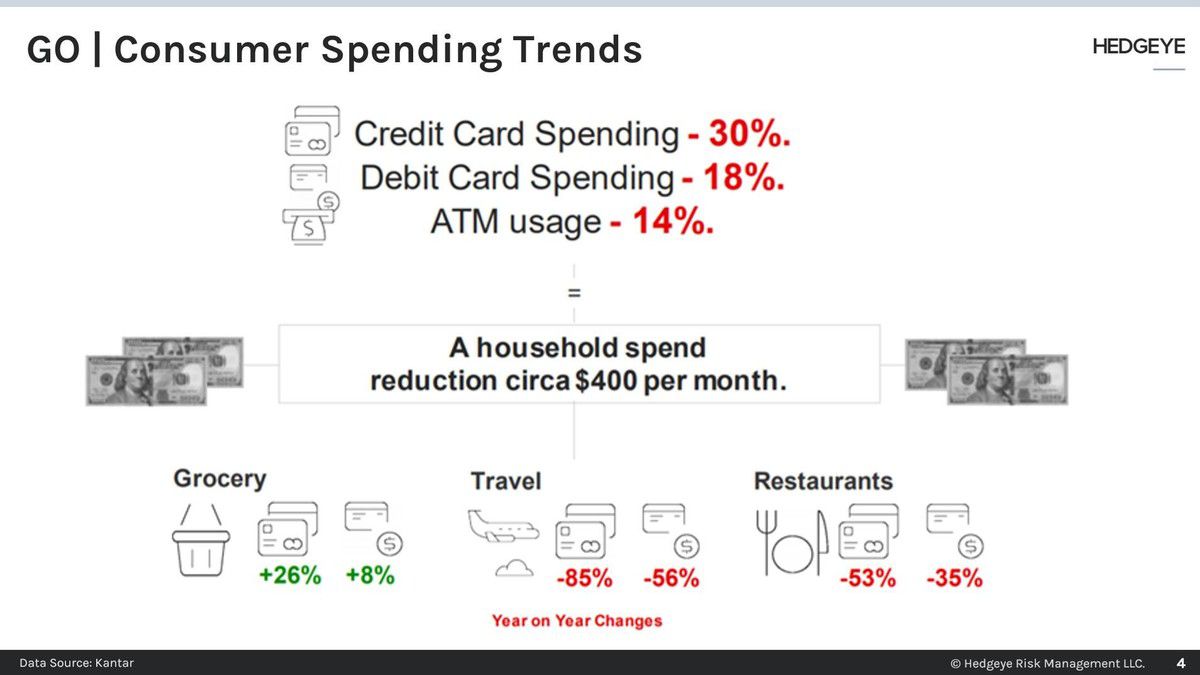

According to Kantar, during the pandemic, there has been a reduction in spending of roughly $400 per household per month in the U.S., as seen in the illustration below. The reduction has been across credit card (-30%) and debits card spending (-18%), but surprisingly despite contactless spending, ATM withdrawals (-14%) have declined less. This is likely due to which spending categories are seeing the largest declines.

Spending on travel and restaurants are down significantly while grocery spending is up 26% on credit cards and 8% on debit cards. Everywhere in the world people are spending less money than normal despite the rising grocery food bill. Grocery Outlet (GO) is well positioned with its discount food offering for the current spending environment with consumers spending less, but more on groceries.

SFM

Sprouts Farmers Market (SFM) reported Q1 EPS this week of $.79 beating consensus expectations of $.54 and $.46 a year ago. Same store sales increased 10.6% vs. consensus expectations of 6.6%, driven by March which was up 26% from the initial pantry loading. Management estimates COVID shopping provided a 9.6% boost. Grocery, frozen, and vitamins were the strongest categories – areas of competitive strength for SFM. Gross margins expanded 180bps and were well above low expectations. COVID-19's sales boost had an 80bps benefit from sales leverage and consumers being less price sensitive. The company recently began changing its new store promotional strategy which also contributed to the margins gains. The timing of pulling back on new store promotions will benefit from the current environment. SG&A as a percentage of sales was flat YOY.

Management noted that many consumer trends have continued into April with SSS up 7.2% (with an Easter penalty of 3-4%). The additional costs of cleaning and compensating employees will have a more significant impact on Q2 because the initiatives only began to ramp up at the end of Q1, so there will be less SG&A leverage going forward. The pandemic has only impacted one planned new store opening, and the company remains on track to open 20 this year. The company is also reinvesting in new customer acquisition while seeing the COVID-19 impact drive new customers that are forming new shopping behaviors. We have been modeling EPS upside this year and expect the earnings multiple to expand. Q1 results provided more visibility on both.

TDOC

There is likely a thesis to sell the stocks that have benefitted from the COVID-19 such as Teladoc (TDOC) as the economy re-opens. With Telemedicine generally, and TDOC specifically at least, we do not think this is the right call as behavior changes are likely sticky, and estimates have room to move higher. App downloads are backing off the COVID-19 surge highs, but the new run rate is settling into a higher level than pre-COVID and utilization continues to ramp. With the guidance for 2020 went to $800-$825M from the previous $695-$710M and consensus of $726M, but the real focus will turn to 2021 where we think the step up in estimates could be similar to 2020. As of 1Q20, penetration into convertible patient volume is 5.6% leaving substantial upside, even in the face of competition.

Without a vaccine we do not expect consumer behavior to change and telemedicine to embed into the delivery system. Importantly guidance does not include a resurgence in COVID-19. As the economy re-opens it is as likely for employers to want a telehealth option as a risk mitigation strategy as it will be for consumers.

CHWY

Hedgeye CEO Keith McCullough added Chewy (CHWY) to the long side of Investing Ideas this week. Below is a brief note.

Gold and groceries worked out nicely for us last week. Now we have to feed our pets!

I've been waiting for Chewy (CHWY) to correct since Retail analyst Brian McGough went bullish on it... and it's for sale, down over -3% here on the open today.

Here's a summary excerpt from Brian's recent Institutional Research note:

|

We're also adding Chewy to our Long Bias list. We’ve been positively predisposed to the name since the June IPO, but the current environment is about as good as it can get for CHWY. People won’t stop feeding their pets, but are extremely averse to trudging out the pet store to buy food and supplies. Enter Chewy. It sells a better basket of brands than Amazon, and service is arguably better. |

MAR

Click here to read our analyst's original report.

“Is it the frank or the beans?” The epic question (and recurring line) toward the beginning of the comedy movie classic “There’s Something About Mary” was answered with, “…both I guess”. Well, we’d answer the big question circulating amongst some GLL investors of whether NUG or RevPAR is the driver of hotel brand stock performance the same way. It’s both.

The math and a historical look back certainly suggests that both drivers are critical and will matter for the stock performance at different stages of the downturn and the inevitable upcycle. Unfortunately, both will trend lower with RevPAR moves dominating near term stock performance with NUG providing significant tail risk. We remain bearish on RevPAR, the hotel development cycle, and Marriott (MAR).

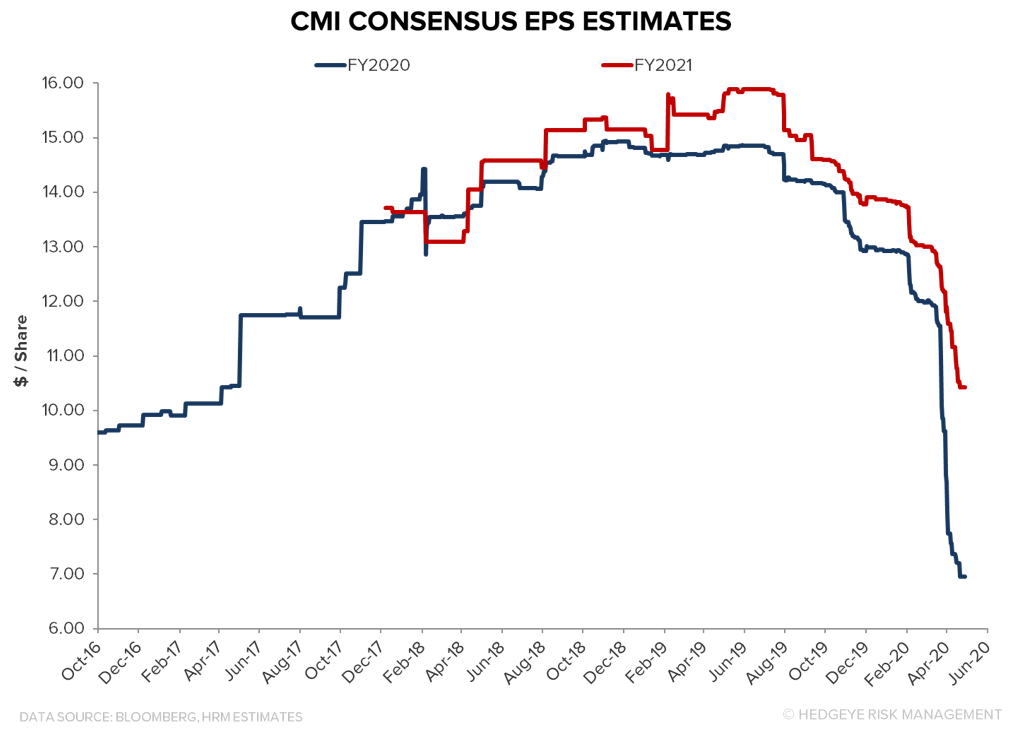

CMI

Click here to read our analyst's original report.

Not a terrible quarter but estimates for Cummins' (CMI) have fallen so far that it allowed the company to stumble over consensus. Cummins also engaged in restructuring at the end of last year, helping 1Q20 reported results. EV delays in the medium-duty space, not long-haul, are the real CMI risk. ESG holders must love that conflicted section of the earnings call – diesel is cheap right now…but because transportation demand has fallen off a cliff, and that is somehow a positive? That is a tortured bull story.

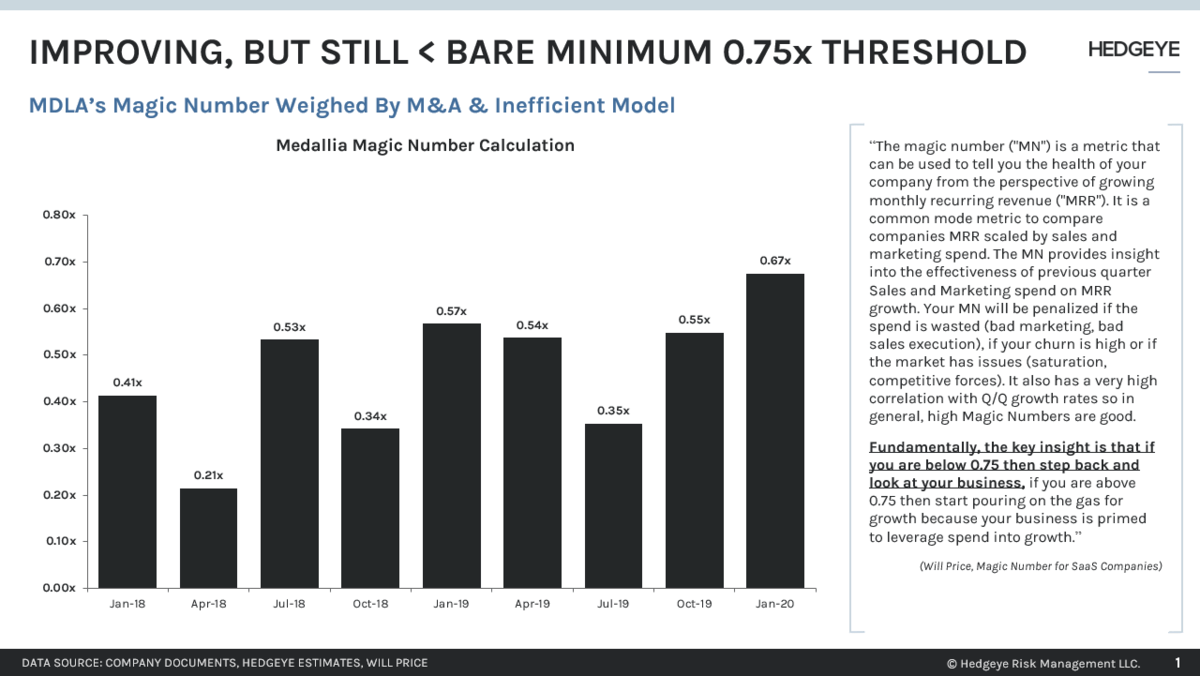

MDLA

Medallia (MDLA) was once a pioneer in the voice-of-customer software industry but MDLA’s high professional services touch, complete enterprise back-end integration, and long time to value / long sales cycle, caused the company to fall behind as the market moved to pure software approaches, easy to use, low dollar, fast time to value, with consequently wider adoption. MDLA has not lost its perch serving large F100 enterprises but those organizations are also using a multitude of other solutions, and incremental customer capture at that level is an uneven phenomenon. We see ongoing organic deceleration for MDLA on dollars and % terms, partly offset by the new CEO spending ~$110MM on M&A in the last 12 months to purchase ~$15-20MM of incremental subscription revenue with acquired solutions unintegrated and delivered from companies that have never scaled.

MDLA Remains a Hedgeye Technology Best Idea Short.

ATUS

Click here to read our analyst's original report.

Altice (ATUS) has underperformed the broader market since reporting weaker than expected results last week. Pay-TV subscriber trends continue to deteriorate, weighing on overall revenue per residential customer which only grew 0.2% YoY despite a 5% price increase across their base in February. Meanwhile, the company continues to plow all free cash flow into buying back the company’s stock while underinvesting in the core business.

The company repurchased $1B of stock in 1Q20, leaving $700M left under their authorization. Also weighing on shares, was news that top 10 shareholder CPPIB completely sold their position in ATUS in the last week. We continue to view ATUS as a melting ice cube/financial engineering story that will limit the companies future growth prospects (cutting back on fiber deployment). We continue to favor Charter Communications (CHTR) as a better pure-play on cable as the stronger operator over ATUS.

DFS

Discover's (DFS) card loan book ended Q1 at $73.8 billion. Applying 18% to $73.8 billion we get losses of $13.4 billion. After-tax, (tax rate is 22-23%) this works out to around $10.4 billion. Divided across the firm's sharecount of 306 million, this is around $34 per share.

Now, the company is coming off a 2019 level of earnings of around $9 per share, so this would equate to a net loss of around $25 ($9 less $34), but that is on a book value of $31.55 and a share price around $35.

To be clear and to be fair, this is an extremely aggressive level of loss assumption. It makes no mitigating assumptions for enhanced unemployment assistance, the potential for a V-shaped recovery, further government stimulus/bailouts, TDR usage, and, perhaps most importantly, it assumes a constant "caliber" of layoff embedded in these numbers as in the Financial Crisis.

SYF

Synchrony Financial's (SYF) management indicated that its reserving levels this quarter assumed a peak rate of unemployment of 10% in the second quarter, followed by an average level of unemployment of 7% in the back half of 2020 followed by a return to 4.5% unemployment in 2021. We find it interesting that the company built its reserves (ex-CECL) by just $451mn this quarter ($1,667mn provision less $1,125mn NCO less $101mn CECL) to help it weather the downturn. On a loan book of $82.5bn that works out to just 55 bps of additional reserving for an assumed jump in unemployment from 3.5% to 10%. For comparison, JPMorgan reported last week it was built its US Card reserves (ex-CECL) by +$3.8bn on a loan book of $162bn, which equates to 235 bps. In other words, it appears that SYF has baked in ~1/4 of the hit that JPMorgan has assumed.

We think Synchrony remains behind the curve in terms of its provisioning and expect further catch-ups will be necessary in Q2 and likely beyond.

MCD

Click here to read the short McDonald's stock report that Restaurants analyst Howard Penney and Daniel Biolsi sent Investing Ideas subscribers this week.

ITW

While China may have bottomed for Illinois Tool Works (ITW) in April, the auto market and foodservice equipment remain problematic. ITW estimates for 2Q2020 should *run rate* about $4 per share, and that is assuming they can hit the sort of decremental margins discussed on the call. The shares may have bounced on flat YoY China comments, or maybe that the company plans to emerge stronger or whatever, but we doubt the street is ready to see the 2Q20 revenue declines that impact higher margin segments.

We remain firm on the short thesis.

HLT

Hilton (HLT) kicked off what should be one of the busiest days of GLL earnings in a long time. Though consensus #’s appeared stale, results were generally in line with our lowered expectations and the preliminary numbers that HLT provided in mid-April in conjunction with their AMEX credit card point sale. Details and forward looking color were a little more sparse in this release relative to other releases making the conference call more important to us. With that in mind, we’ll focus on the basics of the release – development and RevPAR.

On development, HLT posted its slowest net unit growth (NUG) since Q3’15 as the posted NUG of +5.8% YoY, slightly below our expectations. New deliveries for the Q were likely impacted by the threat of Covid-19 where in some markets construction had grounded to a halt, but we had also heard from WH that owners are opting to wait before officially opening given the dearth of industry demand. We expect this to be a problem for HLT in the coming quarters and year.

Continue the short.

SYY

This week Sysco (SYY) reported FQ3 EPS of $.45 missing the consensus estimate of $.58 and down from $.89 last year. Overall organic case volumes declined 5.8% while gross margins contracted 7bps. The U.S. foodservice case volumes fell 5.2% (breaking a 23 consecutive quarter streak of growth) down sequentially from +1.3% while gross margins contracted 11bps. International foodservice revenues declined 7.8% in constant currencies while gross margins contracted 50bps. FQ3 itself is very backward-looking as most of the quarter was pre-COVID. Total sales fell 60% in the last two weeks of the quarter as the impact of the pandemic had its most significant impact. The U.S. foodservice division was down 60%, SYGMA was down 50%, and International was down 70% in those two weeks. Since the end of the quarter, sales trends have improved by about 15% points with more recovery in the U.S. than in Europe. Sequential improvement from -60% will continue as restaurants re-open, but the shares never discounted a scenario with sales continuing to be down 60%.

Sysco's accounts receivable balance fell by a whopping $791M sequentially. The allowance for doubtful accounts increased by $174M at the end of the quarter. Adjusted earnings excluded $153M of excess bad debt expense in the quarter. An allowance of less than 5% of the receivables balance when so many restaurants are at risk of closing may seem low, but restaurants won't be able to have food unless they pay distributors. Payment terms will matter when Sysco only has a 30% share of its customer's spend. The generally stable inventory balance ballooned by $190M at the end of the quarter as the company froze some items to reduce spoilage. Sysco had a sufficient $6B of cash and available borrowing capacity as of the earnings report, but it is negotiating its EBITDA to interest expense covenant in its credit facility.

Management said two-thirds of costs are variable, but a higher amount of costs will have to be added back when restaurants start to open their dining rooms again. When Sysco's restaurant customers operate their dining rooms at 25% and 50% of their capacity in the coming weeks, the strain on restaurants’ cash flow will grow, and the shakeout will accelerate.

GOLF

Click here to read the short Acushnet Holdings (GOLF) stock report that Retail analyst Brian McGough sent Investing Ideas subscribers this week.

BYD

If we apply the state by state reopening cadence + assume that casinos will only be included in either Phase 3 or later, it might not be until the end of Q2’20 before Boyd Gaming's (BYD) properties are fully open. Important to also note that these reopening forecasts assume that there are no setbacks during the phases (i.e. case count accelerations or spikes in positive Covid-19 test rates).

But what about the actual process of reopening once BYD is allowed to open? Herein lies the can of worms. Likely capacity constraints (less seats on tables, plastic partitions, fewer slots due to spacing restrictions, etc.), re-staffing hurdles (luring service workers back), and incremental cleaning costs (one time and ongoing) are just some of the operational hurdles waiting for BYD and others when states do start to give the green light.

Moreover, the demand picture is just so uncertain with an elderly demographic that should be very cautious about crowded venues and potentially damaged by the Covid economic carnage.

baba

Hedgeye CEO Keith McCullough added Alibaba (BABA) to the short side of Investing Ideas this week. Below is a brief note.

I've been waiting on a bounce in BABA to lower-highs... and we got that in the last few days...

Here's an excerpt from an awesome proprietary tool China analyst Felix Wang built for our Institutional Research clients tracking Chinese demand in real-time (he’s long PDD vs. BABA short):

|

WHY IT MATTERS The Wechat Index is one of the tools we use to gauge user engagement and interest in China. It's a keyword popularity index. While the time series is volatile, trends in the index can be helpful in identifying changes in user activity and preferences. We collect index data daily for each of the keywords, and for smoothing purposes, we exclude any outliers/special events. CONCLUSIONS In the e-commerce space, JD, Fresh Hippo (BABA), and Kaola (BABA) were the notable laggards. While some of the traffic for JD are likely redirected to Jingxi which is not captured by the Wechat index, this was surprising given JD was the relative winner in Q1 among the Big 3 in Wechat engagement. With logistics infrastructure back to normal and less COVID-19 concerns in China, Wechat shoppers may be less focused on getting the best logistics i.e. JD and more focused on low prices. Fresh Hippo's decline isn't surprising as the surge in fresh e-commerce was short-lived as we expected. Consumers are returning to supermarkets and wet markets, albeit cautiously. Kaola may be lagging given the international trade disruption from COVID-19 worldwide. |