THE HEDGEYE EDGE

Acushnet Holdings (GOLF) is a solid golf equipment, accessory and apparel company, however it is an industry that we consider to be in secular decline in the US. US golf participation has been in a down trend since 2004, and there is no sign of that changing anytime soon. In 2018/19 golf industry sales benefited from strong macro tailwinds of tax reform and a boom stock market. Sales significant out paced flattish rounds played and lower participation.

The golf equipment companies capitalized on the consumer spend and took up margins to cycle peaks. That means GOLF has been over earning and now it is facing another industry shock that could have as big an impact as the great recession.

It’s a critical time of the year as it relates to golf equipment sales. Late March to late April is when much of the country has demo days for golfers and club members to try and buy all of the new year's equipment, and by May the season is in full swing. Acushnet’s Titleist T-series irons were likely to be a big hit this spring. The problem is many of the golf facilities in the US that facilitate these sales have been closed.

As are now starting to open there is perhaps hope that golf sales can recover. But the problem is “open” simply means allowing play. There is still very little of the golf “economy” in existence beyond greens fees, which means GOLF's sales remain under significant pressure. The vast majority of club buildings remain closed, and most employees are not supposed to be on site. That means no clubhouse/golf shop selling balls and accessories.

There are no gatherings allowed so there are no demo days, no club tournaments, not golf charity/corporate outings, and no club events. Social distancing makes club fitting very cumbersome (many Titleist buyers would want custom fitting). A significant amount of ball an accessory sales happen around tournaments or outings with custom logos on the balls.

Pretty much all of those events have been cancelled until at least mid-summer if not all year. There is little desire for players to seek out a new set of clubs when part of the season is lost, and the game is not quite “normal” this year. Golf retail stores both big and small are largely deemed unessential and not open for business. Many of golf retail sellers are seeing tough liquidity conditions meaning stocking or ordering the appropriate goods is tough to do with no visibility to demand.

Equipment sales will not recover, and with the days of golf already lost and social distancing restrictions still in place rounds of golf will be down significantly in 2020, which will pressure sales of balls, gloves and other accessories that are tied to the amount of play.

After all of the immediate Covid-19 risks play out, you still have a high priced discretionary industry in the middle of a US recession/depression. The market is clearly missing what plunging markets and recessions do to the golf economy. In the last year or so golf was just starting to stabilize from the impacts of 2008/09.

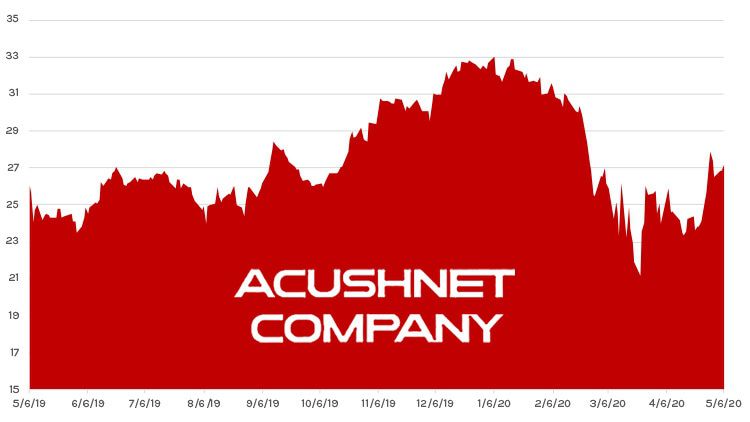

This COVID depression/recession will send another secular shock to the industry meaning lost players, lost businesses, and lost courses, and therefore lost long term equipment demand. EPS numbers have been coming down, but the stock has barely budged, putting GOLF at all time high multiples over 21X PE.

For 2020 the street expects sales to be down 6% and EPS to be down 30%. We see those sales and earnings expectations as being wildly off from what will be reality. As a reference in 2009 ELY sales were down 15%, EBIT was down 125%. For 2020 we think the earnings will be down over 50%, and even as we model 2021 “recovery” earnings, given what we think the state of the consumer will be, we see earnings struggling to get to levels half of what was seen in 2019.

With current peak multiples on EPS expectations that are way too high, we think the stock has 50% downside from current levels. We’d argue a more appropriate valuation is a mid-teens multiple on earnings down at least 50% YY. That’s a $12 stock (or lower) with the current price around $27.