This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

This week in The Institutional Risk Analyst, we ponder the state of the bezzle, that fluffy, frothy portion atop the political economy that feeds the purveyors of fraud and dubious financial schemes.

Six months ago, the bezzle seemed set to expand infinitely thanks to the largess of the Federal Open Market Committee. But now with the COVID19 disaster, all of the air has been let out of the global economy, leaving those who feed on the bezzle scrambling.

The term bezzle, lest we forget, was coined by John Kenneth Galbraith in his classic 1961 book, “The Great Crash of 1929.” Our friend Mark Melcher at Prudential Securities loved to describe the current state of the bezzle in his research. Galbraith himself describes the bezzle as the “inventory of undiscovered embezzlements,” that grow in times of rising markets. He wrote:

|

“At any given time there exists an inventory of undiscovered embezzlement in – or more precisely not in – the country’s business and banks. This inventory – it should perhaps be called the bezzle – amounts at any moment to many millions of dollars. It also varies in size with the business cycle. In good times people are relaxed, trusting, and money is plentiful. But even though money is plentiful, there are always many people who need more. Under these circumstances the rate of embezzlement grows, the rate of discovery falls off, and the bezzle increases rapidly. In depression all this is reversed. Money is watched with a narrow, suspicious eye. The man who handles it is assumed to be dishonest until he proves himself otherwise. Audits are penetrating and meticulous. Commercial morality is enormously improved. The bezzle shrinks.” |

Under the strange regime put in place by the FOMC after 2008, markets are inflated with fiat money to avoid any hint of asset price deflation. We are told that falling interest rates are meant to encourage employment, but the worst examples found in the world of finance are the real winners with quantitative easing.

The generous estate of zero net-cost leverage allows for ever greater acts of fraud and chicanery, all floated upon a cushion of hysterical investor demand and a newly minted pile of fiat paper dollars. Yet such an artificial market bubble is hardly stable, to invoke Nassim Taleb’s “black swans,” particularly when the civil authorities in many countries decided to shut down their economies for three months.

James Glassman stated: capitalism without bankruptcy is like Christianity without Hell. Well, thanks to an understandable overreaction by civil authorities to COVID19, America is seeing a wave of insolvency unlike anything experienced in the past century. Now that the bezzle has basically disappeared, the speculative classes are left to rationalize strategies that, just 90 days ago, made sense. Let’s ponder some of the winners and losers as the proverbial tide goes out, exposing millions of failed companies, denuded business strategies, defaulted securities and busted individuals.

Some of the biggest losers in the wake of the great flushing are investors in commercial real estate. The great pyramid scheme known as WeWork probably jumps to mind first, a debt driven speculative plan hatched by a barefoot visionary whereby temporary workers would support retail pricing for office space and free snacks.

WeWork did not make sense before February of 2020. Now it is just completely ridiculous. Low rates care of the FOMC made WeWork possible.

Another favorite example of the age of QE is Wirecard, Germany’s technology darling which has been under assault by the financial media and investors due to questions about the accuracy of the firm’s accounting. Even after a much anticipated examination by KPMG, questions about Wirecard remain, in part because the firm apparently cannot produce bank records to substantiate claimed revenue to the tune of $1 billion.

The Financial Times notes that KPMG could not confirm “that the sales revenues exist and are correct in terms of their amount, nor can it make any statement that the sales revenues do not exist and are incorrect in terms of their amount.” Certainly, this report fills us with confidence.

And then, of course, there is the iconic speculative fraud of the age of zero interest rates, Softbank, which naturally has put cash into both WeWork and Wirecard. How the FOMC did not get awarded free call options on Softbank for enabling these and other “investments” by guru visionary Masayoshi Son we’ll never know. A century ago, two guys named Morgenthau and Brandeis would be fighting for the honor of putting Masa San in state issued garb.

The Real Deal reports that Softbank is preparing to write down its stake in WeWork to basically zero. “Every writedown takes WeWork’s carrying value closer to reality. Clearly the value is zero,” Kirk Boodry, analyst at Redex Holdings, told Reuters.

The creditors and owners of the select real estate chosen by WeWork are now busted too. In fact, the owners of commercial and residential properties in most major metros around the US have seen a good portion of their tenant base literally disappear in the past 60 days thanks to the Great Lockdown. Rent collections are down sharply and many of these absent tenants may never return.

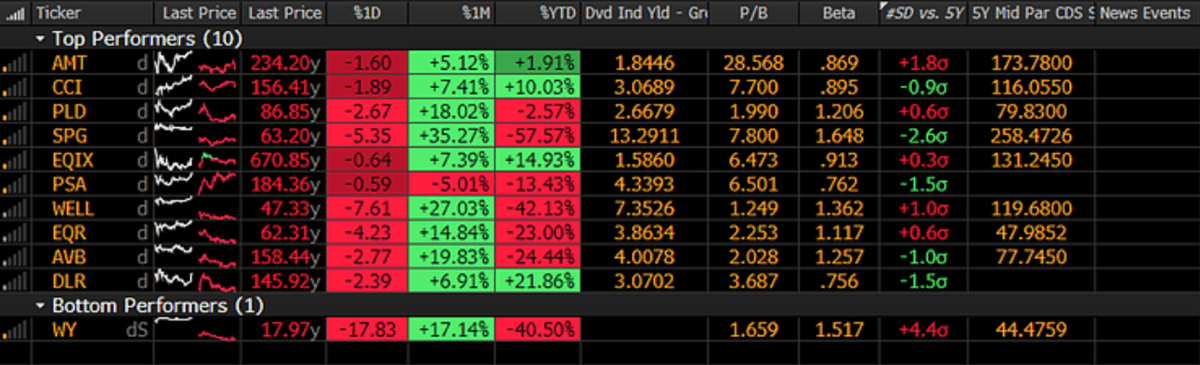

The chart below shows some of the major equity REITs that we follow. Notice in the graphic below that REITs with commercial and retail exposures are faring rather badly, but specialty REITs such as American Tower (NYSE:AMT) are actually up. When we are all living a bad version of “Return to Thunderdome,” with House Speaker Nancy Pelosi in the lead role, at least we’ll have 5G.

Empire State Realty Trust, the owner of the Empire State Building and 13 other commercial properties in the New York region, last week reported in its first-quarter earnings that it collected only 73% of its April office rents and 46% of its retail rents due in April. We expect to see even worse numbers from the equity REITs in May.

We hear reports of residential and commercial tenants fleeing New York or demanding rate reductions from landlords, with obvious downward pressure on pricing for vacant space. Listed rates for rental apartments are in free fall. Landlords will essentially need to eat lost rents on millions of small commercial properties or see the space go vacant. And even if landlords do eat 90 days of lost rent, many small businesses may fail anyway due to the economic dislocation caused by the Great Lockdown.

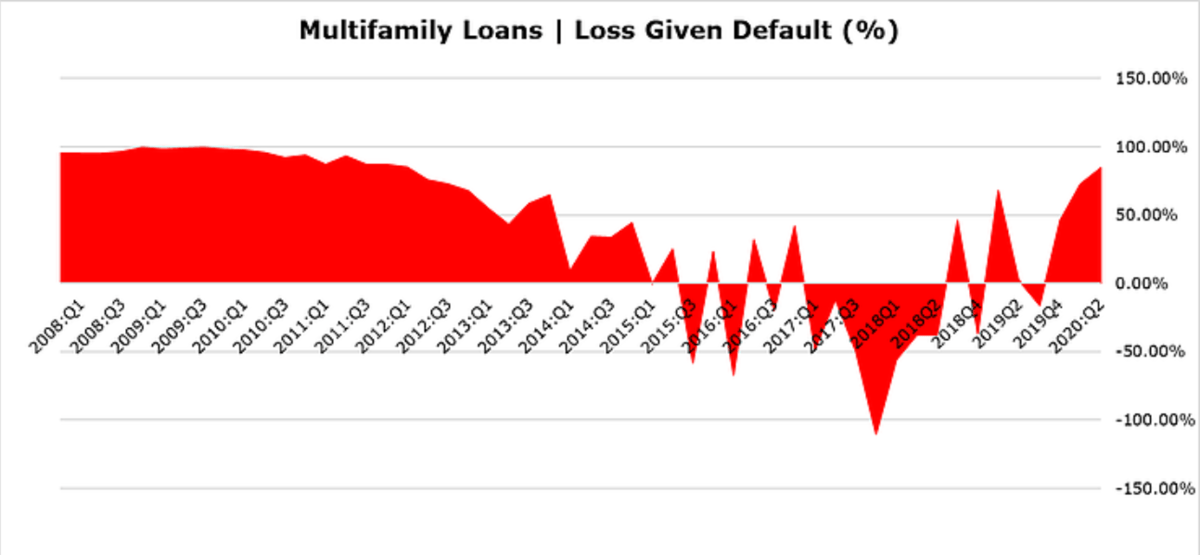

As we’ve noted in past missives, the rate of price appreciation in commercial real estate (CRE) over the past five years drove loss rates post-default negative, just as was the case with residential exposures. Now, however, the dread externality known as COVID19 has evaporated a big chunk of the services sector.

This, in turn, is leading to defaults and requests seeking forbearance that only find parallels in the early 1900s.

We suspect that the downward skew in loss given default (LGD) seen in all real estate exposures will normalize and start to climb above 100% in some cases. The chart below shows LGD for bank-owned multifamily properties and our guess as to what Q1 and Q2 are likely to show once some significant adjustments and restatements of Q1 losses are eventually tabulated. Notice that we expect to be above 80% LGD for bank multifamily exposures by Q2 2020.

We know of a number of businesses in the NYC area that have received PPP loans from their banks. Many will only use a portion of the funds and will return the balance, but with the big positive of keeping their staff employed and health insurance intact. But the sad fact is that many smaller businesses will not be saved and their employees and owners are now busted flat.

We observed in an earlier comment that the world of jumbo loans for banks and investors has pretty much stopped. We know a couple of lenders, each owned by Buy Side sponsors, who’d forsaken the world of agency lending for making non-QM mortgage loans.

Through February 2020, these firms were doing growing volumes in non-QM loans, which were being purchased by banks, REITs and hard money investors. Today, however, these lenders have pivoted, disavowed non-QM and returned 100% to government lending in the FHA and Ginnie Mae market.

Government lending, as it was a decade ago, is the only stable market in residential housing finance today. And remember, non-QM lenders never lose the risk of claims based upon the ability to repay (ATR) rule that was put in place in 2010 by the Dodd-Frank legislation. Remember those three letters: ATR.

As the true extent of the pull-back in many real estate markets becomes apparent, look for groups of trial lawyers to start testing the ATR rule as the basis for tort claims against some of the larger non-QM lenders -- and the Buy Side players who financed these activities, firms like PIMCO and Blackstone (BX).

Meanwhile, the earnings from Fannie Mae and Freddie Mac last week suggest dreadful days lie ahead for the GSEs. As we noted in National Mortgages News (“Why the FHFA's latest move undermines the MBS market”), Washington is now the problem in conventional loans.

The Federal Housing Finance Agency has effectively been taken over by the Cato Institute, which wants to implement free market principles just as the housing sector faces its worst challenge since the Great Depression. For years conservatives wanted to shrink or even kill the GSEs. Now the opportunity arrives.

At precisely when we need the mutualized risk sharing power of the GSEs to support 1-4s, the FHFA is trying to shrink the GSE’s role in housing. Dick Bove of Odeon writes that FHFA Director Mark Calabria believes that “the government should not be in the housing industry; The government sponsored enterprises (GSE) should be taken out of government. No bank is too big to fail.”

What the COVID19 event proves in housing is that in times of stress, no amount of private capital can support $11 trillion in single family housing assets or another $1.5 trillion in multifamily properties.

Banks own a quarter of the 1-4 family housing market, the FHA/VA/USDA about 18% and the rest – about $6 trillion in loans -- is supported by the GSEs. Without financing support, we expect residential home prices will start to fall in many markets around the US before the end of 2020.

Meanwhile, the REITs and funds are the chief victims in this cycle. Think L Shaped recovery in services, and related CRE and multi-family assets. The hard money investors we work with in the market for CRE, small commercial and non-QM residential loans see lots of opportunities, but also a lot of risk. The current judgement seems to be that we need to be thinking about 40-50% discounts off peak valuations to make the risk/reward equation start to make sense.

As we consider the wreckage in the credit markets caused by the Great Lockdown, a couple of things to ponder. First, the response to COVID19 is doing more damage than the disease itself. The dislocation to the economy, especially the real estate and services sectors, will set back global economic growth by decades.

Second, the unwillingness of politicians to admit that the universal lockdown was a mistake is now a major obstacle to moving forward. We need to protect the vulnerable and send everybody else back to work, without masks and social distancing. Otherwise the global economy is headed for depression like conditions for decades to come.

And finally, the damage inflicted on the speculative classes in the past 90 days is just the appetizer. The unwind of leverage in real estate and many parts of the world of secured finance is just starting. Aircraft leases? Hotels? Casinos? Yet the agency loan sector, including government guaranteed residential and multifamily loans, will be an island of stability in a sea of woe.

The deflation of the bezzle may be very painful indeed.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington.

This piece does not necessarily reflect the opinion of Hedgeye.