This guest commentary was written by David Stevens, CEO of Mountain Lake Consulting. It was originally posted on The Institutional Risk Analyst.

When America realized that it had to shelter itself and implement safety and distancing measures to respond to COVID19, most public policy makers jumped into high gear.

Addressing housing was part of this enormous series of response measures in an effort to cushion the US economy and its people. Almost all sectors of the federal government's apparatus dove in, from the Federal Reserve, to Congress and the White House, HUD, and more rallied to do their parts. But notably absent was was Federal Housing Finance Agency (FHFA)?

With an excess supply of mortgage backed securities (MBS) in the market as investors repositioned their balance sheets, the Fed began aggressively buying agency MBS removing the excess, creating a short, plunging yields lower and prices higher eliminating the risk of failure to companies holding these bonds.

When the Fed realized it had pushed rates down too hard, risking a severe blow to nonbank lenders with short hedge positions on their production pipelines, they quickly slowed the purchases. Rates stayed low but margin calls slowed and the mortgage markets stabilized. But the Fed did not stop its commitment to support liquidity in the agency markets.

Beyond simply purchasing Treasuries and MBS at an unprecedented level, Fed Chairman Jerome Powell took to the airwaves to spread a message of their commitment to cushion the economy. To his credit, Powell appeared in multiple interviews including the Today Show, something rare for a Fed Chairman. He understood that supporting the markets, financially and rhetorically, was important.

ABC reported last week, Federal Reserve Chairman Jerome Powell pledged Friday that the Fed will “use our tools" to support the economy, an effort to ease fears over the viral outbreak” one of many stories in early March that were followed by rate cuts and more.

In came Congress to help pass a sweeping bi-partisan piece of legislation, signed into law by President Donald Trump that provided $1.8 trillion in aid to spread across small business, consumers, housing, and more. It was this piece of Legislation that created a new form of forbearance. Rather than follow the blueprint from the last recession, where one had to prove something called “hardship,” in order to insure that taxpayer dollars only went to those who needed it, this was quite different.

First, CARES Act forbearance was made available to all homeowners with a government backed mortgage. That removed any friction in allowing people to get relief from mortgage payment. Yet it also introduced moral hazard by allowing people who were still employed and able to make their payments to skip them anyway. Unlike 2008, consumers need only ask for assistance with no proof of hardship.

Second, The CARES Act offered 6 months of forbearance with an option to extend for another 6 months, a term far longer then the four month terms used previously.

Third, the legislation stated that loans in forbearance were to be considered “current” and the consumers credit would be reported as such; Forbearance loans would not be considered delinquent mortgages.

There were gasps heard across the mortgage industry simply due to the magnitude of the CARES Act forbearance. Estimates of impact showed massive dollars of outlays depending on who would take forbearance. This is also where the FHFA and Director Mark Calabria began to ignore the facts and depart from basic commercial market practice in the world of secured mortgage finance.

The Mortgage Bankers Association as well as top economists began looking at potential impact in ranges of $40 billion to $100 billion in skipped payments. Calabria, an economist, made his prediction in public comments that total forbearances would be under 1 million borrowers by May, but the actual number was already more than three times that and rising by the 3rd week of April.

The risks were clear to almost all in housing. From mortgage bankers to consumer groups, realtors, and members of Congress, all took aim at Calabria warning of the impact to bank and nonbank servicers, calling for a liquidity facility to be established to help make advances. As noted in an article by Mike Calhoun, Jim Parrott, and Mark Zandi:

“Congress hasn't made the repayment obligation disappear, but simply moved it from the borrower to the mortgage servicer.”

The Cares Act offered this to all borrowers with a government backed mortgage. Because forbearance lasts 6 months or more, and because these "performing" loans would remain in the securities rather than being repurchased out of pools, there was an open ended funding requirement for all servicers, banks or nonbanks. The amount of advances required looked to wipe out some smaller servicers. This unprecedented liquidity requirement thrust on industry by Congress was in excess of any available source of funds.

But Director Calabria not only turned a deaf ear to such real world concerns, he made things worse by making public statements about his willingness to let nonbank mortgage servicers fail. In shocking remarks as reported: Calabria suggested, incredibly, that Fannie Mae and Freddie Mae "could just transfer servicing in a way that's not too disruptive" and give those mortgage servicing rights owned by independent mortgage banks to other entities – either larger nonbank servicers or the banks themselves. He even suggested that some homeowners might be better off dealing with larger banks, a dangerous fiction everyone in the mortgage industry knows to be untrue.

His comments set off a chain of events that tightened credit. Rather than calm markets like other Federal regulators and use the tools of government under his authority to step in and support this legislation, Calabria's public comments sent a message to warehouse lenders, MBS investors, broker dealers, and more that they might get caught holding the bag should one of these companies fail.

Investors might lose their back stop for reps and warrants made, warehouse lenders might get stuck with a pipeline of forbearance loans, etc. So credit overlays started rolling out and the result is significant tightening in credit terms for 1-4s. Minimum credit scores rose, debt to income ratios dropped, certain programs like bond loans, high balance GSE loans, and more simply began to vanish.

What’s most outrageous perhaps is FHFA's view about transferring servicing and consumer experience when the opposite is true.

First, no servicer wants to take on a new volume of in-forbearance loans, particularly not in the midst of a rising credit loss cycle.

The FHFA's position shifts the advance burden for forbearance and actual loan defaults to the servicers, who must fund and manage the workout process to be done post forbearance. The costs would be significant and the GSE’s would have to essentially pay handsomely for any servicer to take that on. Second, as the FHFA Director knows first hand, the transfer itself is disruptive to the consumer and simply shifting to a “larger” servicer adds no benefit to the experience.

Far from providing liquidity, the FHFA aided and abetted a credit tightening event at a time when liquidity is needed most. HUD, in contrast, approached this in a different and far more responsible way. Rather than shake the markets, HUD moved quickly and quietly to calm them. GNMA took a liquidity facility once only used for servicers in technical default and facing collapse and expanded it to all of their issuers thus easing the concern about finding the money to make these advances.

In addition, the FHA's tools were already in place to handle the borrower and the servicer once the forbearance period ended. The servicer submits a partial claim to FHA and the balance to be repaid by the borrower is tacked onto the back of the loan in the form of a “secretary’s lien.” The forbearance is to be paid back at minimum when the home is sold or refinanced. In effect, HUD is financing the CARES Act forbearance.

After weeks of pressure on Director Calabria, he came back with partial help by capping the forbearance payments to four months. But much of the damage had already been done. Credit had already tightened in the correspondent lending and other channels. And, as of this writing, because these loans will remain in the security there is no reasonable timeline for the servicer to get the advances returned.

Keep in mind, all of the $5.5 trillion of conventional servicing is owned by the GSE’s. It’s their legal asset as the owner of the mortgage notes and issuer of the UMBS securities. In the conventional market, the servicer owns the loan level servicing and acts as essentially an agent for the note holder, servicing the loan for the GSEs and, indirectly, the investors in the UMBS securities.

The FHFA did not protect these crucial assets owned by the GSE’s It should have authorized a liquidity facility to be established by the GSE’s to make advances and thereby protect the value of this servicing asset. A GSE-led liquidity facility would not impose any risks on the GSEs and, indeed, would have made Director Calabria the hero of this story. Sadly, his lack of understanding of the rules of secured mortgage finance blinded him to this obvious political win.

A GSE-led liquidity facility would have alleviated the risk to the massive non bank market that dominates the US mortgage finance system, accounting for over 60% of all mortgages made. The risk, fully secured by 1-4 family mortgages, would be placed it where it should be - in the hands of two companies controlled by the federal government and under the control of this federal regulator.

The sort of extremis that is the COVID19 crisis was the reason Congress created Fannie Mae almost a century ago, to provide liquidity to the mortgage market in times of crisis and, more than anything, to buy time. When Congress created Fannie Mae in 1938 it was about buying time. The wave of defaults that are right behind the CARES Act forbearance issue should be the focus of our attention.

The complex web of inaction, obfuscation, and belligerence in the midst of a national crisis when all other federal agencies, Congress, and the President dove in is remarkable. Calabria’s ignorance about how the GSEs and the mortgage industry function as well as consumer behavior only adds to the danger.

When the FHFA and GSE’s announced a new policy of charging 700 basis points for acquiring first payment forbearance loans and refusing to buy those that were legitimate, agency eligible cash out refinances, this just added to the absurdity of the responsibility that the GSE’s were shirking.

And here we sit today with the outcome.

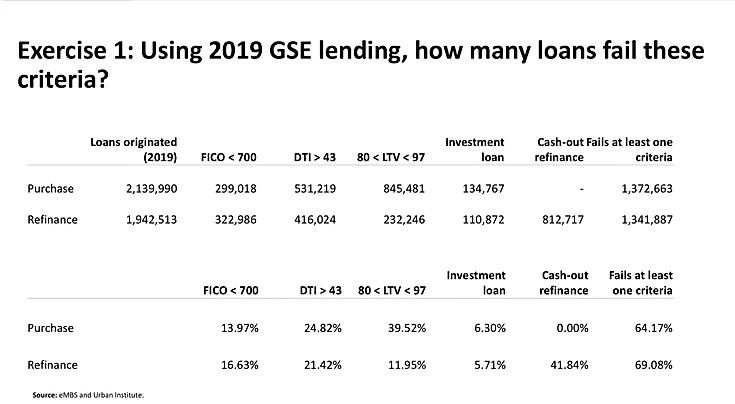

Announcements from lenders include things like stopping all cash out refinances, having a 700 minimum FICO score and maximum 80% LTV. The loss of product availability is incredible. According to the Urban Institute these overlays produce an outcome where approximately 64% of all purchase loans fail at least one of these overlays.

History will look back at this incredible time that took over the world. The response from the US government will certainly undergo scrutiny about preparedness, response, and subsequent efforts to return to work and the post effects of these moves. For housing the response from the Federal Reserve, Congress, the White House, and HUD was swift and effective.

The inept actions taken by the leadership team at FHFA to date are inexcusable. To not use two government controlled and backed companies whose primary mission is to provide liquidity especially in a counter cyclical period is unforgivable.

With billions of dollars at stake on assets owned and guaranteed by Fannie and Freddie, this FHFA Director has shirked his responsibility as the Conservator of the GSEs to protect the value of the servicing assets owned by the GSEs and the conventional market that gives the enterprises economic life.

The behavior of FHFA these past weeks has been incredible. They are putting confusion and uncertainty into the market. Instead, FHFA should join other federal agencies and leverage these tools of government to help the economy and provide a cushion as they are able to. There is still time to get this right.

ABOUT David Stevens

David Stevens is the CEO of Mountain Lake Consulting and former President and CEO of the Mortgage Bankers Association (MBA). Prior to assuming this position, Dave served as the Assistant Secretary for Housing and Federal Housing Commissioner at the U.S. Department of Housing and Urban Development (HUD).

This piece does not necessarily reflect the opinion of Hedgeye.