MGM Macau is likely to see continued improvement under Grant Bowie but net IPO proceeds to MGM are still unlikely to reach the suggested $500m.

THE TURNAROUND PATH

While MGM Macau is unlikely to ever produce the type of numbers we see at WYNN, we do believe that they can continue to fix the sins of the past and materially improve results at the property. So what went wrong?

When MGM entered Macau, there was no shortage of hubris. They embraced the build it and they will come approach. With MGM’s gaming expertise and brand name, and Pansy’s knowledge of the market, it was a slam dunk, right? Well, Pansy is not a casino operator and has no experience as a property manager, and MGM did not have a track record of operating successfully outside the US. MGM brand recognition was indeed high, in the mid 90% range. Unfortunately, it was the movie studio that was well recognized. Not many people in Asia knew MGM as a great casino brand. Oops.

Here are/were some of the problems:

- Bad layout that appealed to a US player but not an Asian player

- Fixed

- No marketing or sales function at the property

- Now they have a marketing team in place

- Surrounded by construction

- Ceased, now that Encore and One Central are open

- Confusing logo

- Recently rebranded to MGM Macau instead of MGM GRAND MACAU

- Had no business plan and strategy

- We’ll see whether improved performance is a result of market strength and/or Grant Bowie’s strategy

- Too many FTE’s

- Cut 1,000 FTE’s from August 2009-March 2010

- Too much bureaucracy with the 50/50 structure

- Still an issue

- Investors will penalize the IPO multiple

- Too conservative with whom they dealt and lent money

- Becoming more aggressive in the way they manage their business but only extend credit to players with assets outside of China

- Increasingly extending credit to junkets

There is no question MGM is benefiting from the incredible strength of the market. Unfortunately, market share continues to languish after a push forward late last year. However, margins are expanding and the increasing use of junket and direct play credit should boost share going forward.

THE IPO

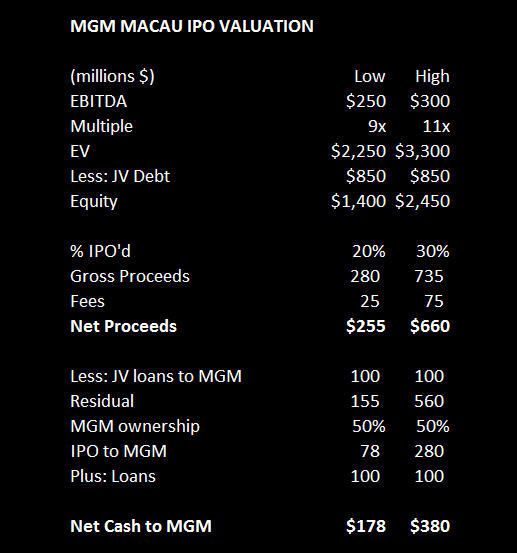

MGM Macau generated only $150 million in EBITDA in 2009. However, with Grant Bowie’s changes and the strength of the market, we are projecting $240 million for 2010 and $279 million for 2011. We think it is fair to base the IPO valuation on a range of $250-300 million. Based on that level of EBITDA, we calculate the net cash proceeds to MGM of only $178-380 million after factoring in expected joint venture debt and the repayment of MGM’s intercompany receivable (~$100MM), which will get repaid before divvying up the IPO proceeds. We assume 20-30% of joint venture is sold through the IPO.

Some may argue for a higher multiple range but we think investors will severely punish the IPO valuation for the joint venture structure and a lack of control. The valuation may be enhanced somewhat by a credible and well-articulated Cotai strategy but investors are unlikely to ascribe significant value to that part of the story given the huge amount of Cotai supply coming online and MGM’s dismal development track record.

Based on our research and analysis we believe it is unlikely MGM generates the $500 million in net cash proceeds it is expecting.