Below are updates on our eighteen current high-conviction long and short ideas. We have added Sprouts Farmers Market (SFM) to the long side and Hilton (HLT) to the short side of Investing Ideas. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

TDOC

This past week, our team spoke with the CFO of a major hospital on the west coast. According to him, the recovery for the US Medical Economy will be slow and tenuous. After having canceled 100% of all elective procedures in his network, the hospital was planning to enlist a detailed plan to gradually recover surgery volumes. He expects that patient volumes are unlikely to ever fully recover as habits change.

These comments led to a much deeper conversation concerning the current state of telemedicine, his hospital’s implementation of it, and forecast for its role on “the other side” of COVID-19. He reported that of the 54% of visits being conducted (as a percentage of pre-COVID) at his hospital, nearly half were being conducted utilizing a telehealth platform. He went on to confirm our thesis that telehealth will remain, and COVID-19 has fast tracked adoption.

He went on to give some color on how different areas of the hospital would view telemedicine when we return to normalcy. He expects that primary care will increasingly adopt the platform for routine check- ups and following up after surgical visits. On the other hand, Higher RVU’s will likely revert to in-person care, such as surgical specialties. We remain Long Teladoc (TDOC) on the Hedgeye Health Care Position monitor.

KR

More than half of Americans’ spending on food is outside the home. In 2010 coming out of the last recession, Americans spent more on food away from home for the first time as seen in the chart below. Through the combination of COVID-19 restrictions and the likely consumer spending downturn, we are in the mindset that the share of spending on food at home will reverse years of share loss. The restrictions on eating at restaurants and leaving your home have encouraged more Americans to cook than Julia Child could ever dream. With the supply chains being challenged to catch up with demand many items on the shelves are missing and consumers are probably the least price sensitive in a generation. As one of the largest grocers in the US Kroger (KR) is well positioned to benefit from the structural change in food consumption.

SFM

Hedgeye CEO Keith McCullough added Sprouts Farmers Market (SFM) to the long side of Investing Ideas. Below is a brief note.

Sprouts Farmers Market is a grocer focusing on natural, fresh, and organic food. It is attractive due to its high single digits % store growth opportunity, accelerating SSS, and inflecting margins while trading at a mid-teens P/E multiple.

Grocery stores are benefiting from the sales shift from food away from home for longer than just the one-time pantry stocking ahead of the stay at home restrictions that is currently reflected in estimates.

The daily sales growth of local and independent grocers reported by Womply (a CRM provider) shows the recent re-acceleration in sales after consumers have begun to return to the grocers.

MAR

Click here to read our analyst's original report.

With 16% of hotels closed and some 12% of rooms closed, RevPAR is trending down 70-80% across the board. The strain on the “system” will be challenging for more than just a year as industry cashflows dry up and new development commitments stall out. With this in mind, we have been discussing the potential for incremental deletions in the coming years, but the potential for attrition might be the bigger risk this cycle vs deletion activity that typically arises when the cycle’s downturn starts to clear.

Yes, the SBA / PPP programs will buy owners some time and help them cover fixed costs during this troubled time, but those programs can’t manufacture revenues and cash flow growth for owners. Hotel brands like Marriott (MAR) will do their best to keep as many owners in the system as possible, but it’s quite possible that our deletion / attrition toggle in our NUG matrix, might need to be on the higher side, predominantly due to the likely spike in hotel attrition. This risks are not priced into most hotel brand stocks at present, in our opinion.

CMI

Click here to read our analyst's original report.

Estimates for Cummins (CMI) have moved little since the outbreak of the novel coronavirus in the US and Europe. Freight rates for trucks are broadly the lowest since 2017… who is out ordering trucks? Significant preannouncements are likely in the next few weeks. CMI is likely to have EPS less than $10 in 2020 vs. a $12 consensus, given energy, China, and North America truck exposure. Implied volatility remains very high for airlines, even after pre-announcements. Auto and oil related names have also seen notably increased volatility expectations priced in.

Insofar as the economy is turning more averse for cyclicals – a core part of themes deck that was evident in the data prior to coronavirus – being bearish on a cyclical business that is over-earning and correcting to the downside with long-term value creation challenges seems straightforward. CMI remains a top short idea for us.

MDLA

Medallia (MDLA) CEO suggests that Coronavirus won’t affect the implementation or sales process of the Medallia product because most of it can be done remotely

- His suggestion runs counter to our research and field notes indicating that the core Medallia product is high-touch and deeply integrated with back-end systems. If correct, perhaps the CEO’s comment shows MDLA’s shift to selling lower value, un-integrated products to smaller companies, as well as M&A based revenue which does not require core Medallia integration expertise

- Also, MDLA revenue skews heavily to USA (76% of revenue in NA and increasing) which suggests that MDLA has not yet seen the negative impacts of Corona in its results

The CFO finally divulged the diluted share count (171MM)

- Recall, in recent quarters MDLA avoided disclosing the diluted share count by claiming 1:1 ratio of basic and diluted owing to Net Losses at the GAAP level. MDLA still has GAAP net losses but maybe now investors can finally start using the right share count

- Now investors can see MDLA trading ~9x forward recurring revenue and ~7x forward total revenue

SQ

Square's (SQ) subscription business, increasingly based in revenues from the Cash App, is performing well with expanding gross margins of 82%. Note, Cash App revenues have a 77% gross margin; however, Cash App revenues feature a transaction-based component and thus the margin on subscription and service-related revenues is even higher.

Nonetheless, GPV growth sequentially decelerated by -73 bps to +24.75% Y/Y, resuming a broader trend of deceleration after having briefly stabilized last quarter. Transaction-based revenue growth of +24.61% Y/Y, however, was up +1 bp sequentially owing to the effects of the company's November pricing change.

Despite shedding the lower margin Caviar business, adjusted EBITDA margin of 19.1% decreased -271 bps on a linked-quarter basis, in accordance with the company's prior guidance to ramp its sales & marketing spend to drive increased awareness of its seller business and the Cash App.

With growth in the core managed payments business continuing to slow, SQ's future is inextricably linked to the success of the Cash App.

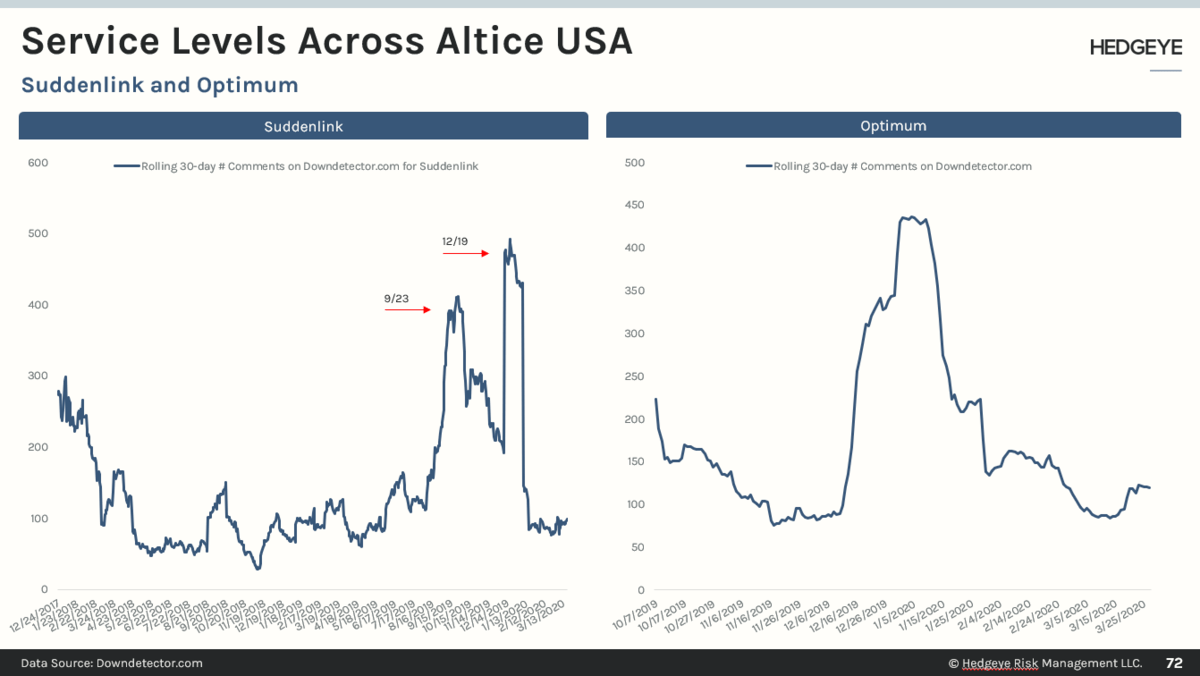

ATUS

Click here to read our analyst's original report.

We updated our data trackers from the Better Business Bureau, Glassdoor.com and Downdetector.com. We spoke with the BBB and they expect a delay in processing consumer complaints. Meanwhile, the Net Promoter Score (NPS) for Altice (ATUS) compensation and benefits, and view of senior management continues to trend well below peers. In terms of network stability, the number of comments on downdetector.com suggests that the Suddenlink and Optimum networks are holding up well so far since the national emergency was declared on 3/13.

DFS

Consistent with our original short thesis, we are seeing delinquencies continuing to tick upwards despite a still remarkably favorable labor backdrop, signifying the escalating risk profile of the underlying book, namely greater late-cycle subprime exposure - a stark contrast to the last downturn when Discover Financial (DFS) was shedding risk steadily in the years leading up to the crisis.

Discover, CFO John Green previewed the company's forthcoming 10-K disclosure on troubled debt restructurings, with credit card TDRs up +$1.1B or +48% y/y to $3.4B as of December 31, 2019. Combining the 2019 and 2018 ending balances, average TDRs for the year were $2.85B - a near tripling of the $1.0B figure in 2016.

Accordingly, Discover Financial remains a Hedgeye Financials Best Ideas Short.

SYF

While contract extensions with major store parents are in place, we draw on the experienced insights of the Hedgeye Retail Team to cast serious shadow on the outlook for some of Synchrony Financial's (SYF) major brick and mortar partners like JCPenney and GAP; A reminder of late-cycle realities: elevated loan loss rates, increased defaults, higher credit costs, slower loan growth, and highly sensitized investor sentiment to the consumer finance space amid deteriorating economic conditions.

SYF has high sell side ratings combined with low levels of short interest which historically have translated to underperformance according to our proprietary scoring system. With the Hedgeye Macro Team firmly positioned in Quad 4, we highlight SYF's abysmal record under an economic regime characterized by decelerating growth and inflation.

We stay firm with our short thesis.

PYPL

While PayPal's (PYPL) total take rate increased sequentially by +4 bps to +2.49%, it remains -9 bps lower y/y. The transaction expense rate, however, increased sequentially by +1 bp to 0.96%, +0.5 bps higher y/y as well.

Net transaction expenses, transaction & loan losses, and customer support & operations expense from the gross total take rate, we see a +3 bp sequential increase to 1.12%; however, on a y/y basis, we see a -8 bp decrease and the continuation of the downward trend in adjusted total transaction margin.

BABA

We aggregate on a daily basis the total number of mobile Taobao/Tmall search keyword shows, clicks, click-through rate & conversion rate for the top 50 stores in terms of sales volume (RMB). This has implications for Alibaba's (BABA) customer management revenues within its China commerce retail business.

It was a good March for Tmall's CTR and conversion rate. Undoubtedly, a greater number of online shoppers (helped by Goddess Day promotions) and the continued waiving of certain Tmall/Taobao merchant fees stimulated March's rebound. However, we believe it is within consensus expectations as a February disappointment was offset by a better March.

SMAR

The question is: how far can Smartsheet (SMAR) take upsell if the Land in unit terms is fixed? Management is savvy. They see the end of the upsell road, and will push for more M&A as well as pivot to positive FCF. SMAR will exit FY21 with positive FCF on the way to ~$150MM FCF by FY25.

And that is assuming no change in the ability to add 150k new paid seats per year and to continue to increase past $1k incremental billings/seat. But if that is the ‘no interruption’ model (not from saturation or from COVID or from cycle or from competition) and that stock price is already something we have seen if you factor slower organic growth rates and share count dilution…then what is the ‘interruption’ model?

Point is: the upside potential from rinse and repeat has already been registered in this Smartsheet (SMAR) stock, and even if perhaps there is a no-COVID rebound, the downside case is more compelling to us for a landlocked company that is good at upselling existing customers but isn't widening out adoption metrics in one of the largest potential markets out there in productivity software and at the best time ever (last few years) for selling into it.

FB

We see downside to Facebook (FB) 1H20 consensus growth estimates as the spread of COVID-19 weighs on global growth and pushes the U.S. deeper into #Quad4 in Q2.

We believe investors don't fully appreciate the cyclical nature of the business, with advertising budgets often the first to get cut in periods of weak demand.We went short FB on 3/5 with the view that advertising spend would be negatively impacted by COVID-19. Three weeks later, and we can confidently say that we were not bearish enough. We see a 30% downside from here. For 2020, our base case advertising revenue growth estimates for FB is -13% YoY.

PINS

1Q20 revenue of $269-$272M represents growth of 33-35% YoY (compared to 46% YoY in Q4) and was in-line with consensus estimates (which have come down from $280.5M since February). Global ARPU growth in Q1 grinded to halt as incremental user growth continues to come from countries where Pinterest (PINS) doesn’t monetize and due to “weakness across nearly the entire advertising market”.

While management noted “record levels of engagement” in user activity in the last two weeks of March, PINS didn’t see a noticeable positive inflection in user growth in Q1 compared to more communication driven platforms like FB/TWTR. In fact, global user growth slowed modestly in Q1 on a YoY basis, and U.S. MAUs saw the slowest QoQ increase in Q1/Q4 in 3-years… which suggests that PINS continues to struggle to appeal to the male demo and scale even in a period of quarantine.

MCD

For decades the investment case for McDonald's (MCD) that it was the largest landlord in the U.S. It leases the land, the buildings, or both on a significant markup to over 13,000 restaurants in the U.S. and a good portion of the 36,000 restaurants internationally. Today the investment case for MCD is that it's the largest landlord in the world, and nobody can pay the rent!

Not to mention that 15% of the company's units are closed globally, with the rest of the system operating on limited hours. McDonalds is allowing franchisees to defer rent and service fees for a few months. Given the ongoing stress from stay at home restrictions, the greater McDonalds community is under significant pressure, and the National Operator Association (NOA) is pushing back on how the company is dealing with franchisee support. What MCD is not doing, is helping to support the additional payroll costs (hazard pay) that others in the industry are doing to support front line employees. By not providing additional support, the CEO is only hurting the franchisee's cash position further, which will ultimately tarnish the McDonald’s brand!

ITW

Estimates for Illinois Tool Works (ITW) have yet to reset lower despite increasingly clear headwinds to the conglomerate's core exposures, including automotive, foodservice equipment, and manufacturing capital investment. ITW’s ~84 business tend to have high operating leverage; in the post GFC period, ITW has also run with more financial leverage than the decade prior. Conglomerates tend to look as though diversification reduces cyclicality, but the current COVID-19 driven downturn is likely to prove unusually challenging for the majority of ITW’s end-markets. Foodservice equipment looks likely to endure an exceptionally severe and prolonged downswing, with collapsing restaurant traffic and a used equipment overhang likely to severely impact revenues.

Global automotive sales – and China had been a content story for ITW – are likely to drop meaningfully as employment and consumer confidence slide and used car prices decline. Capital spending on measurement and test equipment should suffer on lower demand. While some construction activity may hold-up comparatively better, it not a source of offsetting strength in our current data sets. Divestitures to focus the ‘strategy’ are in jeopardy given market disruptions.

HLT

Hedgeye CEO Keith McCullough added Hilton (HLT) to the short side of Investing Ideas this week. Below is a brief note.

This isn't the first day when Hilton (HLT) has drifted to lower-highs intraday on #decelerating volume. But that’s a similar set a short seller should be looking for...

Here's an excerpt from Gaming, Lodging, and Leisure (GLL) analyst Todd Jordan's recent Institutional Research notes on why owning branded hotel stocks is not a very bright idea right now:

|

"Long considered bullet proof with recent valuations commensurate with that view, the hotel brand asset light models of HLT, MAR, WH, CHH and H (to a lesser extent) are being put to the ultimate test. A bullet proof vest is useless against a head shot and the COVID-19 pandemic might be that gun pointed right at the face of unit growth. Certainly, the asset light vest partially deflects the RevPAR bullet vis a vis a hotel owner, but will unit growth provide the offset to RevPAR degradation? This has been the asset light thesis. We’re not so confident and expressed precisely why on in this deck and call." |