|

Below is a complimentary research note from Financials analysts Josh Steiner and Drago Malesevic. If you are an institutional investor interested in accessing our research email sales@hedgeye.com |

With the return of a risk-off environment, we have relaunched our Risk Tracker to track key risk measures across the various banking systems around the world.

Note, we plan to publish the Risk Tracker on a dynamic basis, contingent with evolving conditions in markets, i.e. more frequently during periods of acute stress and less frequently in periods of relative calm.

HEDGEYE FINANCIALS RISK TRACKER

Key Takeaways:

- The US TED Spread decreased -5 bps d/d to 125 bps as of 04/06, up +87 bps (+230%) from four weeks ago

- CDOR-OIS decreased by -21 bps d/d to 66 bps as of 04/06, up +3 bps (+6%) from four weeks ago

- Yesterday's High Yield OAS reading of 9.26% fell -16 bps d/d, up +284 bps (+44%) higher from four weeks ago

- Median CDS spreads for US, Canadian, and European financial institutions all tightened DoD as of 04/06

Our heatmap below is signalling rising risk across most measures on short and medium-term horizons.

Summary

1. TED Spread – The TED spread moved -5 bps (-4%) DoD to 125 bps as of 04/06, registering +87 bps (+230%) higher from four weeks ago.

2. Euribor-OIS Spread – The Euribor-OIS spread held flat DoD at 12 bps as of 04/06, registering +1 bps (+5%) higher from four weeks ago.

The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk.

3. Chinese Interbank Rate (Shifon Index) – The Shifon Index held flat DoD at 1.00% as of 04/06, registering -59 bps (-37%) lower from four weeks ago.

The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

4. CDOR-OIS Spread – The CDOR-OIS spread moved -21 bps (-25%) DoD to 66 bps as of 04/06, registering +3 bps (+6%) higher from four weeks ago.

The CDOR-OIS spread is the Canadian equivalent of the Euribor-OIS spread. It is the difference between the Canadian interbank lending rate and overnight indexed swaps, and it measures bank counterparty risk in Canada.

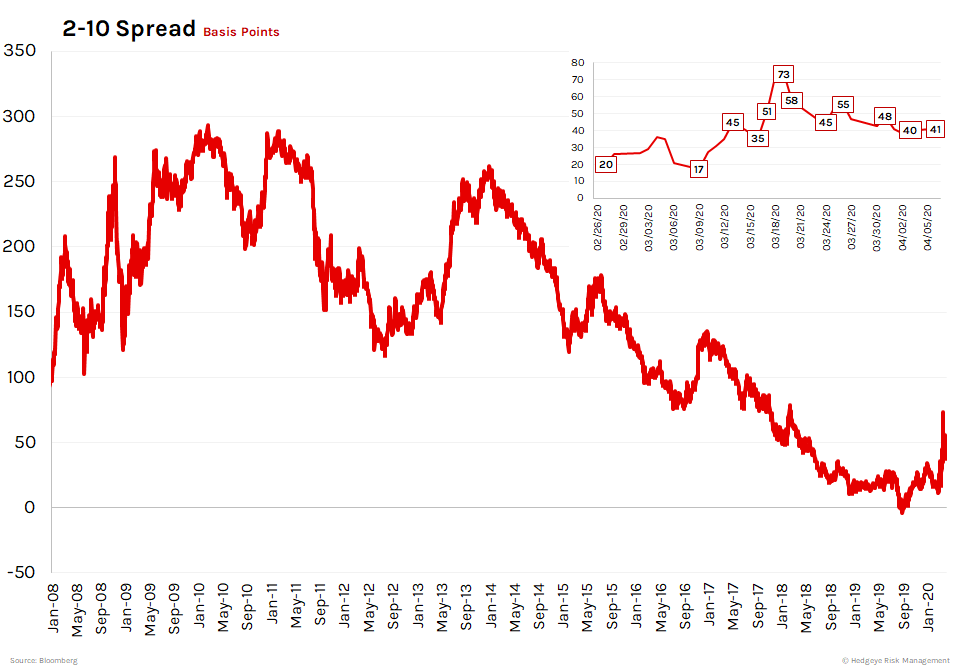

5. 2-10 Spread – The 2-10 spread moved +1 bps (+2%) DoD to 41 bps as of 04/06, registering +24 bps (+139%) higher from four weeks ago.

We track the 2-10 spread as an indicator of bank margin pressure.

6. High Yield (OAS) – Option adjusted spreads on high yield moved -16 bps (-2%) DoD to 9.26% as of 04/06, registering +284 bps (+44%) higher from four weeks ago.

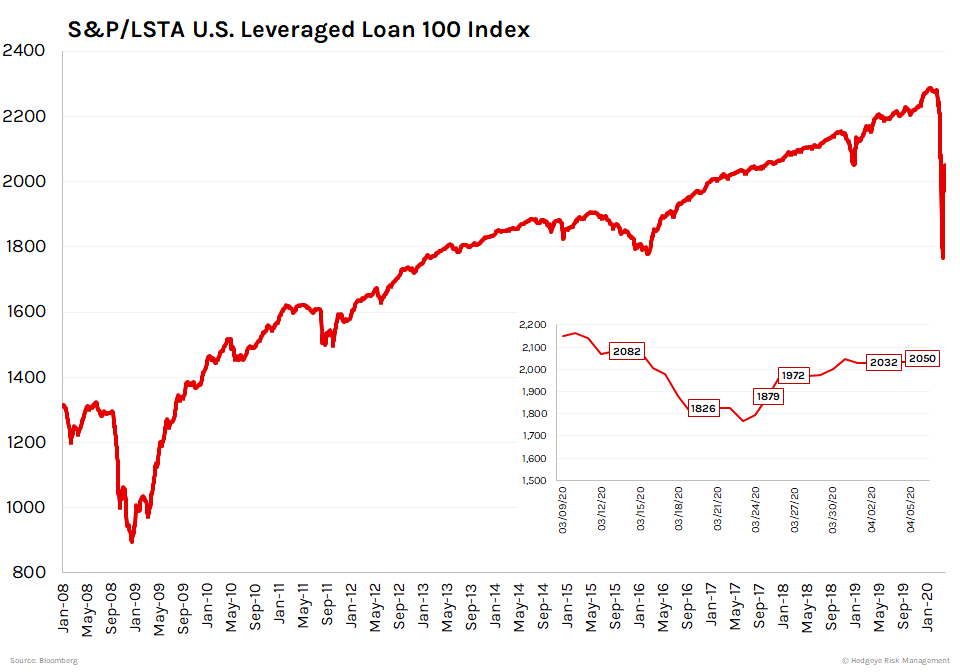

7. Leveraged Loan Index – The Leveraged Loan Index moved +18 bps (+1%) DoD to 2050 as of 04/06, registering -98 points (-5%) lower from four weeks ago.

8. North American Financial CDS – The median North Americans financials swap moved -6 bps (-6%) DoD at 98 bps as of 04/06, up +3 bps (+3%) from four weeks ago.

9. European Financial CDS – The median swap moved -9 bps (-8%) DoD to 101 bps as of 04/06, up +20 bps (+24%) from four weeks ago.

10. Asian Financial CDS – The median swap moved +2 bps (+3%) DoD to 76 bps as of 04/06, up +21 bps (+37%) from four weeks ago.

11. Sovereign CDS – U.S. swaps moved most DoD, compressing -3 bps (-11%) to 22 bps as of 04/06. German swaps widened most MoM, rising by +7 bps (+38%) to 24 bps as of 04/06.

12. Emerging Market Sovereign CDS – Indian swaps moved most DoD and MoM, rising +4 bps (+2%) and +138 bps (+151%) to 229 bps as of 04/06.