We shorted Ruby Tuesday on Friday for two main reasons.

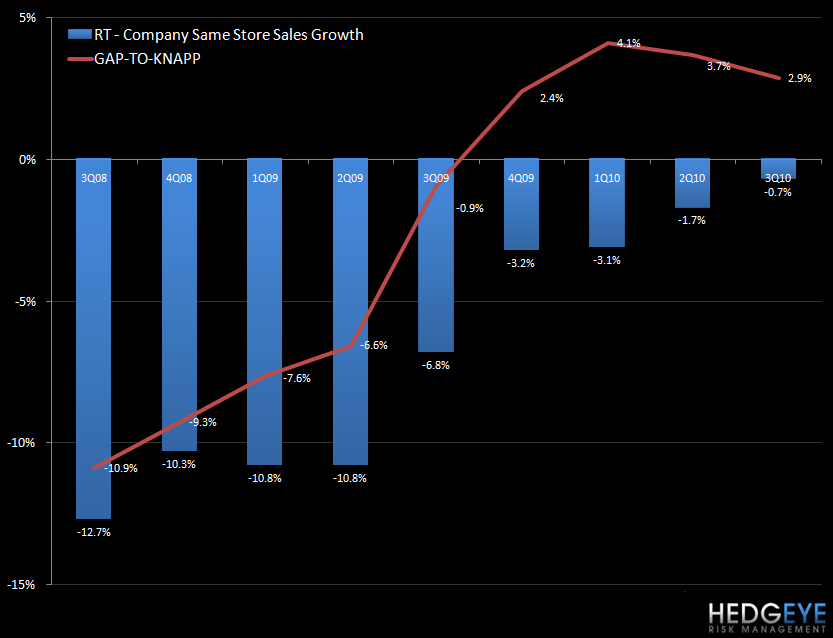

Firstly, casual dining trends are not showing much strength. This has been implied by various management companies as well as the whisper number for June’s Knapp same-store sales number which we wrote about last week (CASUAL DINING - KNAPP RUMOR MILL). News emerging of CPKI slashing Q2 guidance further confirms the softness in casual dining restaurant sales recently, particularly in May when CPKI posted a -7.9% same-store sales number according to their press release. Specific to RT, we can see in the chart below that compares get increasingly difficult going forward. The company will need to drive incremental sales year-over-year to maintain or improve trends.

Secondly, driving incremental sales without compromising margins is going to be difficult. In their third fiscal quarter of 2009 (roughly 1QCY09), according to Chairman and CEO Sandy Beall, “[our] performance started to stabilize in the third quarter as a result of improved sales from our marketing initiatives that better communicated our compelling value proposition to our guests, as well as the implementation of $45 million to $50 million in annualized cost savings.” As RT laps these marketing initiatives, it will become increasingly difficult to drive traffic without further discounting. Additionally, while casual dining trends are showing weakness, Knapp Track sales have easier compares over the next few quarters while RT’s compares are growing more difficult. This should compress their “Gap-to-Knapp” (shown below).

Howard Penney

Managing Director