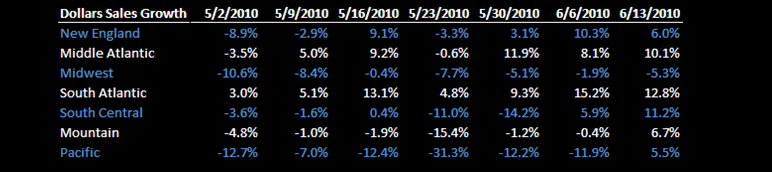

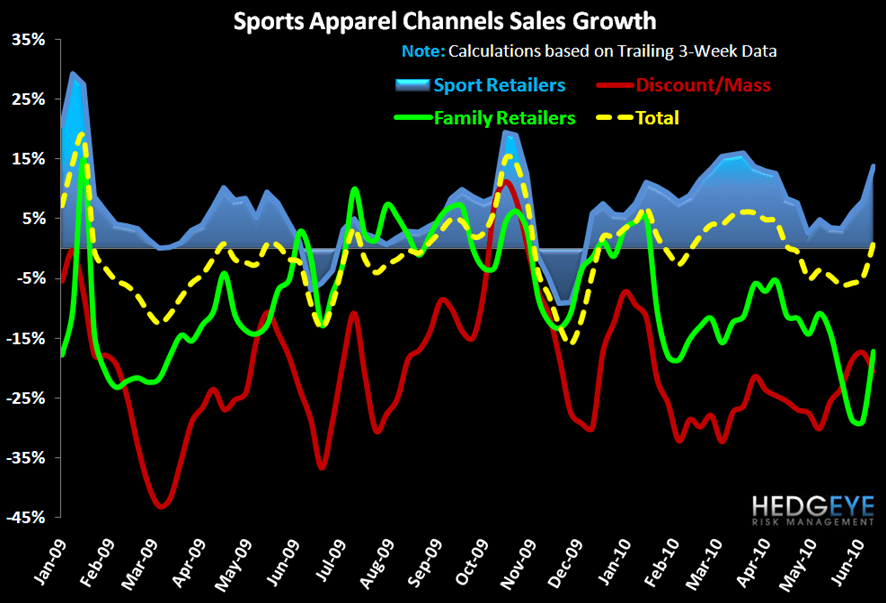

The athletic industry is still looking good. Regional performance is shaping up out West. Nike and UnderArmour are looking solid, while Columbia is simply crushing it.

Conclusions:

- Both footwear and apparel sales maintain a healthy underlying trend.

- Apparel is stronger on the margin, as it continues to gain traction week on week. Footwear decelerated last week, but the more-important 3-week trend is still holding.

- The week showed a sharp rebound in Pacific, South Central, and Mountain states. Note that some retailers – including Payless – highlighted these regions as a source of comp weakness in the recent quarter.

- Reebok footwear continuing to trend +160-170%yy. This is ALL toning. We’ve gotta give credit where it’s due.

- Nike and UnderArmour remain strong…Though a clear standout is Columbia Sportswear, which is posting solid numbers across the board in footwear and apparel alike.

LEVINE’S LOW DOWN

- According to Nielsen, SKU counts in the supermarket channel shrank by 1% in 2009. While this is hardly a noticeable amount to even the trained eye, 60% of retailers indicated that the reductions were driven by the desire to eliminate shopper confusion. Categories that were reduced the most included water, cookies, and shampoo. Shower gel, yogurt, and carbonated soft drinks actually showed SKU count increases.

- Rumors persist that Kohl’s has been investigating real estate in Canada. While no formal plans have been announced, the move to the north makes sense and is the most “obvious” international expansion opportunity for any domestic retailer. Recall that Target has already announced it will make a move into Canada over the next five years.

- Converse tops the list of growth in Facebook followers for the month of June. The brand currently has north of 3 million fans, up an impressive 30% since May. Interestingly, the next closet brands in terms of sequential growth were Levi’s and Christian Leboutin, up 10% and 9% respectively.

MORNING NEWS

New York & Co.’s Top Two Design Executives Have Abruptly Quit - Marie Holman-Rao, chief design officer, and Anne-Charlotte Windal, senior vice president and general manager of design, both resigned this week. A search for their successors is expected to begin immediately. In the meantime, Greg Scott, president, will lead the design and visual teams. Windal is expected to stay at N.Y. & Co. for awhile until the company rebuilds the design team. The departures compound the challenges of inventory buildups and some fashion misses that have caused the company to expect Q2 losses. The retailer needs to sharpen its image selling sexy, modern and moderate price apparel and accessories targeting women 25 to 45. <wwd.com/retail-news>

Hedgeye Retail’s Take: This won't be the straw that breaks the camel’s back, but when you're one of the only retailers discounting on top of discounts last year due to fashion misses you've gotta be worried...

Adidas Again Defends Soccer Ball - Adidas again defended itself against complaints against its new Jabulani soccer ball and its performance at the World Cup. Adidas' Global PR Manager Erik Van Leeuwen noted that FIFA has said that the new ball is tested and proven and there have been no complaints. <sportsonesource.com>

Hedgeye Retail’s Take: Negative PR is still PR. And, this is probably not going to prevent the local kid from wanting an “official” World Cup ball to kick around at the park.

Hopkins Sporting Goods Buys Stake in Wrestler's World - Iowa-based Hopkins Sporting Goods has acquired a minority stake in Suplay Products, Inc. dba Wrestler's World. Terms were not disclosed. <sportsonesource.com>

Hedgeye Retail’s Take: This is the real type of wrestling gear, not the WWE kind. Aside from the M&A worthiness of this, there are no signs that wrestling has become a growth area for the sporting goods industry.

Early Sales Indicate Father's Days Sales Upside - Early sales indications are decent — if not spectacular — for most retailers, and they’re expecting a surge in the final days before the holiday on Sunday. So far, traditional seasonal items such as T-shirts, shorts and short-sleeve knits have been most popular. Stores have been aggressive in their promotions this year — whether it’s gift-with-purchase coupons, one-day specials or celebrity in-store appearances. With overall business still a little shaky, stores believe they need incentives such as these to drive sales. According to the 2010 Father’s Day Consumer Intentions and Actions Survey, conducted by BIGresearch for the National Retail Federation, consumers will spend an average of $94.32 on Father’s Day gifts this year, up nearly 4%. Total Father’s Day spending is expected to reach $9.8 bn. Special outings, gift certificates and apparel are expected to be the most popular gift choices this year, according to the survey. <wwd.com/business-news>

Hedgeye Retail’s Take: While this commentary on sales trends is not terribly different from that which characterized Mother’s Day, the reality is the spend on Mom is 50% higher than it is for Dad. Either way, this bodes well for June- which was already off to a solid start.

Tiffany Engages in M-Commerce - The jeweler has introduced an iPhone and iPod Touch app that offers a virtual display case of its diamond rings. The app, dubbed the Tiffany & Co. Engagement Ring Finder, was created in response to growing customer desire for mobile and interactive shopping, the merchant says. The app includes Ring Sizer, a tool that lets shoppers determine their size by placing a ring directly on the screen of the mobile device and aligning it with the correct circle in a guide. Shoppers can browse the collection according to shape, setting, metal or design. The rings are shown in actual size. Each style may be viewed with diamonds of six different carat sizes. And shoppers can zoom in on a ring’s details, pair the rings with wedding bands, and save or share their favorites via e-mail, Facebook and Twitter. <internetretailer.com>

Hedgeye Retail’s Take: Clever way to get males excited about one of the biggest purchases in their lives, especially if they’re shopping at Tiffany. Or better yet an even more clever way for someone to drop a hint that they want to get engaged! Also an interesting juxtaposition between and old-school, heritage brand and forward-thinking technology. It won’t be long before almost every retailer has some sort of mobile presence.

Men's Wearhouse Looks to E-commerce and M-commerce for Sales Growth - The addition of mobile-phone shopping applications that store customer sizes, preferences and offer a phone answering message from the Men’s Wearhouse founder and chairman is part of a plan to increase the e-commerce business. Currently, e-commerce accounts for less than 5% of the company’s $1.9 billion in annual sales. “That’s our main focus now in all our divisions — to make e-commerce an integral part of our business,” Zimmer said at the annual shareholder meeting, describing a strategy in which Internet and sales among the company’s 1,142 U.S. and 117 Canadian stores work in tandem to bolster business. <wwd.com/business-news>

Hedgeye Retail’s Take: With fit and alterations being such an important aspect of a suit purchase, this is one business that may hit some limit on how far it’s direct business can go. However, once fit is established (provided the waistline stays put), we can see some interesting replenishment opportunities via e-com and m-com.

Macy's Private Label I.N.C. to Sell Men's Footwear - Macy’s private-label collection I.N.C. International Concepts, a line of moderately priced apparel and outerwear for men and women, is adding men’s footwear to the offering for fall. A women’s collection is already at retail. The collection will include a wardrobe of looks, from motorcycle boots to high-top sneakers. Set to retail for $60 for sneakers to $100 for boots, the line will hit 150 Macy’s doors in July. <wwd.com/footwear-news>

Hedgeye Retail’s Take: Seems like a natural extension for Macy’s powerhouse private brand, but not one that is likely to move the needle.

Kohl's Inks Deal with Aldo Shoes - Kohl’s is looking to take its burgeoning footwear business to the next level. The department store chain said Wednesday it has inked a deal with Aldo International to produce private-label offerings for the chain. Aldo will design a range of products for women and men, and the styles will be available at Kohl’s stores and on Kohl’s.com beginning next spring. The move, Kohl’s said, will bolster its private-label and exclusive brand segment, which accounted for 47% of sales in the first quarter. <wwd.com/footwear-news>

Hedgeye Retail’s Take: Good move here by KSS to boost its fashion footwear offering while maintaining differentiation from JCP and others. Also, an interesting opportunity to take Aldo distribution out of the mall to new distribution points.

Seven For All Mankind Return to Print Advertising - 7 is aiming to spur growth with an ambitious, multimillion-dollar advertising campaign for fall that will be its first print campaign for the VF Corp.-owned premium denim brand since fall 2008. The campaign, which was shot by Mert Alas and Marcus Piggott and features models Masha and Julian Schratter, will break in September books, in addition to an outdoor and online component. The media buy comprises 15 titles, including Vogue, W, Vanity Fair, InStyle, Elle, GQ, Details, V and Nylon. The ads also will run in Europe and Asia. The brand is celebrating its 10th anniversary this fall and the company hopes the campaign will help drive traffic to stores. For the first time, the brand tapped an outside agency to create the ads, New York-based Chandelier Creative. <wwd.com/markets-news>

Hedgeye Retail’s Take: We're finally seeing VFC put its money where its mouth is. VFC claimed over the last 2 quarterly calls that they would increase spending primarily on Vans and TNF. Now it looks like Seven is getting some marketing dollars as they look to revitalize the once-hyped denim brand. Next up, accelerating store growth?

Overstock.com Most Consistent Online Retail Site in May - Overstock.com had the best consistency rating among large retailers for May, says Gomez, the web performance division of Compuware Corp. Last month the mass merchant had the best aggregate site loading time at 17.60 seconds. Rounding out the top five retailers after Overstock.com, Gomez listed CDW.com (17.85 seconds), Staples.com (18.75), LLBean.com (18.93), and BlueNile.com (18.99). <internetretailer.com>

Hedgeye Retail’s Take: Clearly the benefit of operating in an online world, companies can measure with complete accuracy how fast it takes to load their sites. We just wonder if the consumer really notices a 1-2 second difference in load time across different brands. No matter how long it takes, waiting even a minute is sure faster than getting into the car and heading to the local strip-mall. Clearly there’s a double standard here in terms of expectations in an online vs. offline retail experience.

China's Quanzhou City Produces 20% of World's Sport Shoes - Sports shoes manufactured in China's Quanzhou city currently accounts for 40% of national production in 2010, and 20% of the world's total output, according to China Leather Industry Association. The city has 925 shoe businesses with production capacity of RMB100 million and achieved total output value of RMB208.315 billion in the first five months, up 29.4% from early year. <fashionnetasia.com>

Hedgeye Retail’s Take: Its not like Quanzhou was off the radar, but add the city name to your google global alerts… we will.