This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

As the US financial markets get ready for another volatile week, leaders in the mortgage finance sector spent the weekend in meetings with regulators trying to fashion a way forward. In the $12 trillion marketplace for mortgage finance, liquidity is rapidly disappearing. Banks and even the GSEs are said to be backing away from the mortgage markets with potentially disastrous results.

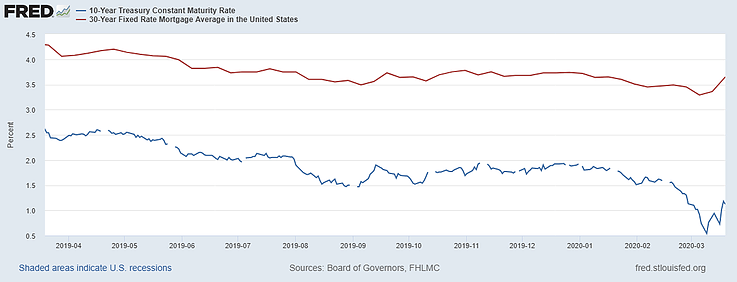

As one dealer noted on Friday: “The specified pool market is dead... there is no spec anymore, it is all TBA. The Fed action this morning did nothing. There are no buyers in the market. The refi rate is between 4.75-5.00%. There has been a massive widening of the Primary rate to swaps & Treasuries.”

Another veteran mortgage manager tells The Institutional Risk Analyst:

|

"You need to get them to buy $1 trillion of agency now. They need to suspend the Volcker rule. Banks are our only chance to not go into a depression. They have to fix the system to let banks add liquidity. We also need a PPIP. Get the mortgage market working. ABS is totally shut down. DoubleLines of the world are panicking. This is worse than 2008 for the system. If they don’t act soon we are in real trouble." |

Despite the efforts so far from the Federal Reserve, the mortgage finance markets are increasingly dysfunctional and the risk of a significant financial failure is growing.

For example:

* Liquidity is drying up in the short-term mortgage financing market for loans, mortgage backed securities (MBS) and servicing advances. There are no bids for specified pools in either the government or conventional markets. Primary dealers reportedly are forcing REITs and other levered investors to liquidate MBS positions, adding further pressure to the markets. Prior to the crisis, 20% of the government FHA/VA/USDA loan market was financed in specified pools. Also, the lack of a specified pool market in conventional and government loans hurts the low-income borrowers that pay the highest fees and need help the most.

* The large banks and GSEs are stepping back from the MBS market and are withdrawing financing for warehouse and advance lines, putting further pressure on independent mortgage banks (IMBs). Fannie Mae and Freddie Mac reportedly are stepping away from bidding on specified pools in the conventional market, claiming that they have “balance sheet issues.” The Trump Administration is wasting what could be a valuable liquidity tool by not using the GSEs, including the FHLBs, to provide liquidity to the markets in tandem with the Federal Reserve.

What must be done to avert a liquidity crisis in the housing market?

* Liquidity: First, the Federal Reserve and other agencies must increase their support for the housing market. Specifically, the Fed needs to increase its purchases of MBS to alleviate strong selling pressure across the market. Add a zero to last week’s daily allocations by the New York Fed.

The single biggest thing the Fed can do to help the market is to announce BIG MBS purchase numbers on Monday and keep buying until yields start to fall. The street is extremely fragile; with commercial banks and IMBs hoarding cash. The Fed in the government market and GSEs in conventional loan market should bid directly for specified pools, again until MBS yields start to fall and especially for discount coupons.

The Fed’s explicit public policy goal should be to push consumer mortgage rates down to 3% or below. The Fed should use continuous MBS purchases to drive down yields on MBS until it is economic for the industry to originate government and conventional mortgages with 3% coupons. By putting a 103 bid for Ginnie Mae 2s in market and allowing issuers to deliver the pools directly to the FRBNY, the Fed could finance trillions in streamline mortgage refinance transactions and add balance sheet assets to the system open market account (SOMA).

* Financing: Second, the Federal Reserve and other agencies, including Fannie Mae and Freddie Mac, should aggressively provide financing for loans, MBS and servicing advances on market terms. The Fed in particular should set up a standing repo facility (SRF) to provide financing directly to all market participants, including banks, nonbanks, dealers, REITs and the GSEs themselves, which will need financing support. As MBS spreads over government yields grow, so too do the funding costs to the GSEs increase.

The government should give the GSEs balance sheet support, perhaps including exercise of the Treasury warrant to convert the government’s preferred equity position in the GSEs into common equity, and increase the GSE portfolio limits to allow them to create market liquidity in loans, MBs and servicing assets as well.

* Third and also needing immediate attention, the Federal Reserve, Treasury/GSEs and other agencies must provide a liquidity backstop to help finance forbearance on mortgage payments for millions of consumers.

Specifically, Congress needs to pass the “Section 13(3) Directive,” which is legislation prepared at the request of Chairman Mike Crapo (R-ID) to provide legal support for using the Federal Reserve’s 13(3) authority and Ginnie Mae’s Chapter 34 emergency authority to provide the needed liquidity to the housing sector.

Importantly, this language would fix an impediment in the National Housing Act that effectively precludes financing servicer advances in the Ginnie Mae segment. Markets need this fixed to have collateral for any national liquidity program involving Ginnie Mae loans. Legislative action would greatly speed the administrative efforts on this long-debated topic.

Bottom line is that the mortgage finance market, the second largest securities market in the world after the Treasury market, is dysfunctional and in need of government support. The Federal Reserve and the three GSEs, supported by the Treasury, need to provide strong support to the markets on Monday morning, including the provision of liquidity to prevent a disorderly liquidation in the MBS markets and potential contagion among banks, dealers, IMBs and REITs.

Just as civil authorities are trying to get ahead of the threat from COVID19, financial authorities in the US need to act decisively to protect the housing sector and then support the growth of refinance volumes to help drive economic recovery. By protecting the housing finance sector from liquidity-related disruptions, the Federal Reserve, GSEs and Treasury can ensure that this key part of the US economy is functional and able to support economic growth in the months and years ahead.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington.

This piece does not necessarily reflect the opinion of Hedgeye.