Most troubling this past week is that high yield and leveraged loans broke to new lows (price), while the CDS for Financial companies (US) was generally wider week over week even though equities were slightly higher. The TED Spread continues to widen, even as LIBOR marks time. Overall, six of our eight risk metrics registered negative week over week changes, while two were positive.

Our risk monitor looks at the following metrics weekly:

1. CDS for all available US Financials (30 companies).

2. High Yield

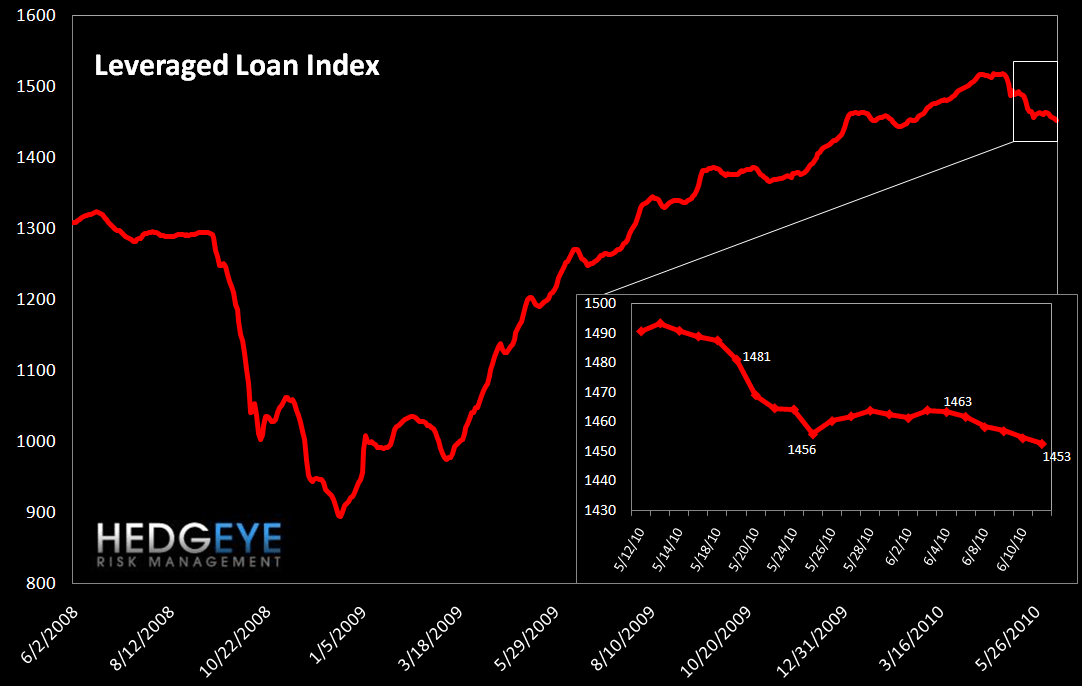

3. Leveraged Loans

4. TED Spread

5. Journal of Commerce Commodity Price Index

6. Greek Bond Spreads

7. Markit Subprime Spreads

8. AAII Bulls/Bears Sentiment Survey

1. Financials CDS Monitor - Spanish banks were the best performers in CDS last week, with three of the four improving. In the US, the environment was less sanguine, as Moneycenters and Brokers CDS rose an average of 11%, Consumer Finance companies rose an average of 7%, and Insurance companies rose an average of 15% (median 9%). Conclusion: Negative.

Tightened the most versus last week: Spanish banks (SAN-ES, BBVA-ES, SAB-ES, POP-ES)

Widened the most versus last week: ACE, XL, ABK, AGO

Widened the least versus last month: BAC, COF, MMC, SAN-ES

Widened the most versus last month: ACE, XL, ABK, AGO

2. High Yield (YTM) Monitor - High Yield rates rose 20 bps, continuing their recent march upward. Rates closed the week at 9.29% versus 9.09% the prior week This is a new high on yield post-February (new low on price). Conclusion: Negative.

3. Leveraged Loan Index - Leveraged loans fell last week to close at 1453, down 11 bps from the prior week. This is also a new low on price post-February. Conclusion: Negative.

4. TED Spread Monitor - A great canary, the TED spread continued to close higher on almost a daily basis, finishing the week at 46 bps, 6 bps higher than the previous week. Even though the Libor component was flat, we still regard this as a meaningful negative. Remember, a persistently high TED Spread was one of the ways markets knew for sure that the fundamental backdrop was not improving in the 2007/2008 credit crisis. Conclusion: Negative.

5. Journal of Commerce Commodity Price Index - A sharp sell-off in this index served as a harbinger of the 2008 crash. This week the JOC Commodity Index closed at 16.11 on Thursday, down 4.3 from the previous week. Conclusion: Negative.

6. Greek Bond Yields Monitor - Greek Bond yields fell 11 bps last week to 811 bps. Conclusion: Positive.

7. Markit ABX Index Monitor - We include this measure as a reflection of what is going on in deep subprime distressed paper. We use the 2006-2 series and look at the AAA, AA, A and BBB- series. The Markit ABX Index was generally flat last week, except the A series, which made a strong move to the upside. Conclusion: Positive.

8. AAII Bulls/Bears Monitor - The Bulls/Bears survey grew more bearish on the margin, with bulls falling 2.6% to 34.5% and bears gaining 2.3% to climb to 43.1%. This leaves the spread at 9% to the bearish side, up from 4% bearish last week. We consider extreme readings in this series to be notable (particularly to the bearish side) as a contraindicator, but moderate readings are less indicative of short-term movements. Conclusion: Negative.

Joshua Steiner, CFA

Allison Kaptur