This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

Officials in Washington are looking for ways to quickly put money into the US economy to counteract the recession looming due to COVID19. One immediate way that the Federal Reserve can very directly add liquidity to the domestic scene is to initiate a massive program to purchase agency and government mortgage backed securities (MBS) directly from issuers, bypassing the too-be-announced (TBA) market and the large bank dealers, and focusing exclusively on refinance transactions at lower rates.

Alan Boyce, retired mortgage banker and CA agribusiness executive, argues that the Federal Reserve should begin to immediately purchase pools of Fannie Mae, Freddie Mac and Ginnie Mae refinance mortgages directly from lenders. The former executive of Countrywide argues that given that the Fed’s existing $1.5 trillion portfolio in agency MBS is likely to prepay rapidly in the next few months, the Fed should be an aggressive buyer. He argues that the Federal Open Market Committee is actually adding duration pressure on dealers by allowing the SOMA portfolio to shrink.

“Housing is the ultimate domestic market, argues Boyce in a conversation yesterday with The Institutional Risk Analyst. “Cutting the fed funds rate to zero and expanding QE4 is a very indirect and inefficient way to get liquidity into the US economy. With the 10-year Treasury yielding 75bp, it is outrageous to see Americans originating 3.5% mortgages. The Fed should create a market for agency MBS with 2% coupons at a premium in order to guarantee mortgage bankers a profit if they refinance homeowners into 3% mortgages or lower.”

Boyce continues:

|

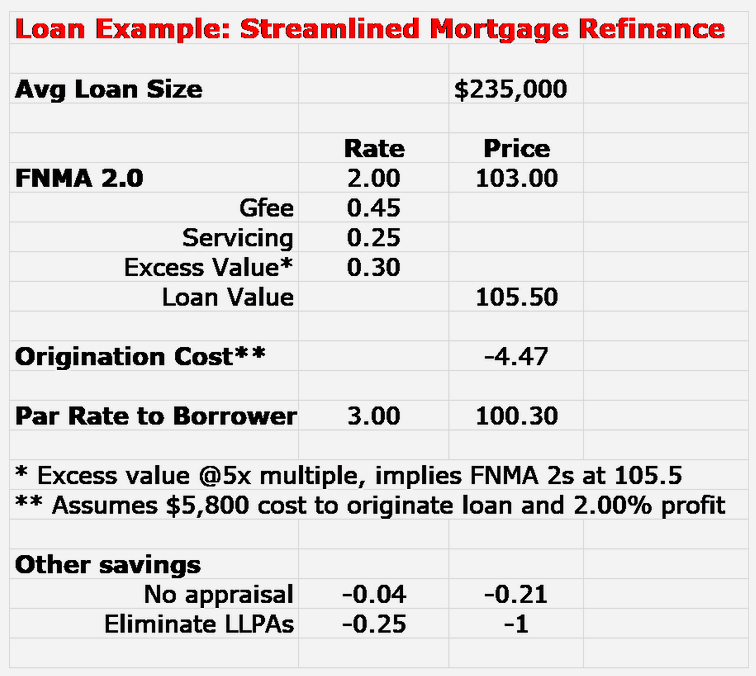

“The Fed should be buying GNMA and UBMS 2 percent coupon (2s) MBS……lots of them and directly from mortgage bankers. Issue an open order to buy $5 trillion of UMBS 2s and GNMA 2s at a price of 103! Let mortgage bankers focus on the paperwork instead of the market volatility. The refi wave is already burning though a huge part of the Fed’s existing MBS portfolio. The runoff of MBS from the Fed’s system open market account (SOMA) is like the Fed selling bonds into the market. Instead, the Fed should start buying back the duration/balance sheet exposure and selling the gamma/vega back to the bond market ASAP. Specifically, Powell should not wait for the actual prepays to hit the SOMA in two months. Buy TBAs now! Drive the prepays and help out homeowners by going directly to the mortgage bankers.” “Below is an example of loan pricing below with better Fannie Mae 2 coupon pricing via the Fed. This approach gets the borrower into a 3% 30yr fixed rate mortgage. We need to direct the GSEs to buy the excess interest only strip at a reasonable price from the lender. More, we can reduce borrower rates by another 29bps with the elimination of the appraisal and loan level pricing adjustments (LLPAs) required from the GSEs. This gets the borrower into a 2.75% mortgage and allows the lender a profit. The FHFA Board of Directors is made up of bank regulators and Fed. They can push Mark Calabria and FHFA to tell GSEs to waive appraisal and LLPAs to make for a more streamlined refinancing process. Remember we were pushing this for HARP 2 back in 2011?” |

Boyce argues that the lenders can simply create conventional agency and government insured pools comprised entirely of mortgage refinance loans to drive the process and could add several hundred billion in liquidity to US households in the next year. And his larger point about the impact of the runoff of the Fed’s MBS portfolio is crucial and alone makes the argument for direct Fed purchases of securities with refinance loans.

Finally, Boyce notes that most of the Street is short duration thanks to the sudden rally in bonds, thus having the Fed act directly may be the only way to get mortgage rates to actually fall without bankrupting a lot of lenders. Boyce argues that mortgage bankers will let their current pipeline of mortgage loans float down to the Fed bid of 103, especially if it comes with no appraisal, no LLPAS and a lower guarantee fee. The resultant MSR will be worth a 5x multiple, that adds to the mortgage banker profits.

“All of the mortgage banker pipelines are short duration due to the rally in Treasuries,” Boyce notes. “If the Fed comes in and simply pumps up the price of GNMA 2's to 103, it will put the vast majority of independent mortgage lenders out of business due to margin calls they cannot meet, not to mention massive pipeline fallout. This is a systemic risk that needs to be addressed. If instead the Fed bids directly for $5 trillion of refis and guarantees a risk free takeout of 103, then the mortgage bankers can originate loans without worrying about market volatility. Mortgage bankers will have a chance to help the economy and make money at the same time. Win-win.”

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington.

This piece does not necessarily reflect the opinion of Hedgeye.