Over the near term, the prospects for a recovery in replacement demand are likely to drive IGT’s stock. The sustainability of IGT’s still high participation share remains a longer term risk.

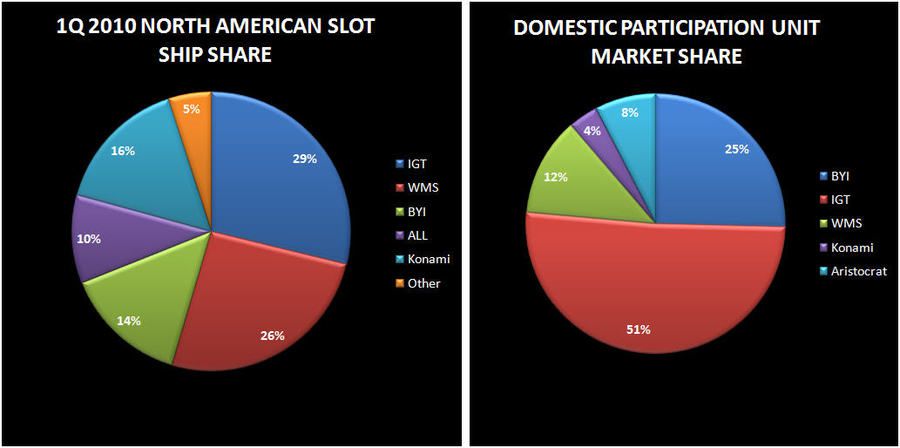

Take a look at the charts below. IGT’s slot ship share has been around the historically low (at least since the 80s) 30% for the last few quarters including 29% in the March quarter. IGT’s market share of high margin participation units was almost twice its ship share at 51%.

As we showed in our WMS Black Book (released in April), IGT’s market share of gaming operations revenue has been on a steady decline but can still fall significantly further. If participation share declines to ship share levels tomorrow, it would mean $350-400 million in lost revenues. Of course, we are not projecting this in short fashion, but over time, IGT is unlikely to participate in this segment's growth and will likely see declining revenues over the long-term.

The other overlooked aspect of its gaming operations segment remains the over-reliance on the Wheel of Fortune line of products. As we wrote about in our 11/27/09 post, “HOW LONG WILL THE WHEEL KEEP TURNING”, the “Wheel” generates almost 50% of the company’s profits. Last year’s patent invalidation opened the playing field and created one more hurdle for IGT in this segment.