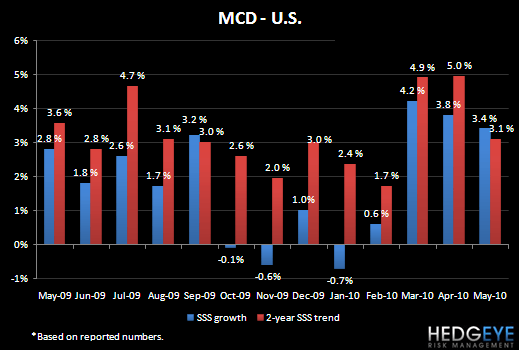

MCD reported May sales today and as I stated yesterday although trends remain positive on an absolute basis, expectations, particularly in the U.S., are ahead of current trends. U.S. same-store sales came in +3.4%, below the street’s +4.3% estimate. Relative to the ranges I outlined in my sales preview note, which look at reported trends versus recent two-year trends, the U.S. segment posted a BAD result and both Europe and APMEA came in NEUTRAL.

Adjusting for calendar shifts, two-year average trends in the U.S. slowed again in May to February levels of below 4% after accelerating in the prior two months to closer to +5% while Europe and APMEA were in line to slightly better. For reference, MCD lapped the initial national launch of its McCafe advertising campaign in mid-May so it will be important to watch how McCafe fares in its second year. MCD reported that the recent addition of Frappes to the McCafe line-up helped drive same-store sales growth in May, but I continue to believe that the beverage initiative will complicate operations longer-term.

FX Headwind…MCD also reported today that for the full year foreign currency translation is expected to have a negative impact on EPS, which reflects a change from the company’s prior expectation of a slight benefit.

Howard Penney

Managing Director