This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

|

In this issue of The Institutional Risk Analyst, we take a look at Bank of America Corporation (BAC), at $2.4 trillion in total assets the second largest bank holding company in the US. BAC was a perennial under performer among the large cap financials for almost a decade after the financial crisis, then in October of 2016 it rocketed ahead on falling expenses. |

In 2017, BAC was one of the best performing large cap stocks, but since then has essentially gone sideways as the momentum of expense reductions did not carry over to higher revenue. Today BAC trades at about 1.25x book value or roughly half the valuation premium assigned to the number one US bank, JPMorgan Chase (JPM). The 1.6 beta suggests that BAC is more volatile than the broad market, and yet its credit default swaps (CDS) trade in line with other top bank names. We own the BAC preferred.

The core strength of BAC is its enormous deposit base and relatively low cost of funds. BAC is not quite as efficient as U.S. Bancorp (NYSE:USB), for example, but it has a larger deposit base than any other bank. This includes $1.2 trillion in core deposits and another $800 billion in non-core deposit funding. Like JPM, only about half of BAC’s balance sheet is loans with the remainder invested in securities, a quarter trillion in deposits with other banks and $400 billion in federal funds sold and reverse repurchase agreements. BAC is a vast island of liquidity and has low funding costs as a result.

BAC struggles on the asset side of the ledger, however, where both the pricing and mix of assets has hurt the bank’s performance and peer comparisons. The bank’s yield on earning assets is well-below the average for Peer Group 1, which includes the 125 largest banks in the US.

BAC’s mix of net interest income and non-interest income is roughly 1:1, providing the bank with a solid if less than inspiring source of earnings. Indeed, the bank’s non-interest income has fallen almost 10% over the past five years. More important, however, is the 35% decrease in overhead expenses that has occurred over the same period as legacy expenses from the subprime mortgage crisis have slowly receded. The chart below shows BAC’s gross yield on loans and leases vs JPM and other members of Peer Group 1.

Part of the reason for the relatively poor asset performance by BAC stems from the decision made after the 2008 financial crisis to significantly de-risk the bank. With a return on assets of just 1.14% and ROE of 10.6% at the end of 2019, the bank trails significantly behind its peers. The 60% efficiency ratio is likewise average compared with members of Peer Group 1, but JPM is four points better at 56%. While BAC has significantly lowered its overhead expenses in recent years, it still remains less efficient than its largest peers.

In the fourth quarter, BAC’s yield on $974 billion in total loans and leases was just 4.25,% but the banks larger securities portfolio pulled the yield on total earning assets down a full point to just 3.25%. The biggest loan class on BAC’s balance sheet is residential mortgages. None of its loan categories breaks 5% yield except credit cards, which is just above 10% and only accounts for $97 billion in assets.

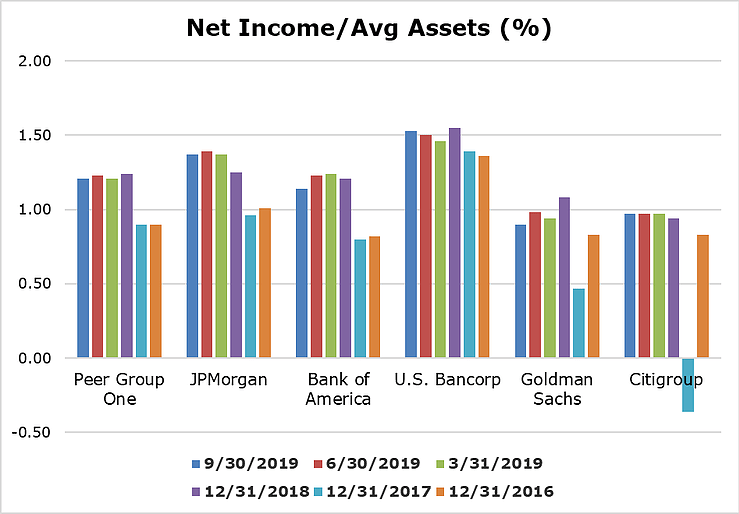

Yields on BAC’s consumer book have fallen 25bp over the past year and the yield on earning assets fell by 30bp compared with Q4 2018. The net interest yield for BAC was just 2.43% in Q4 2019. Overall, interest expenses at BAC rose 20% in 2019 compared with the year earlier, reflecting the considerable volatility in US interest rates last year. When you look at BAC overall, the bank’s net income to average assets was considerably below peer in 2019 as shown in the chart below.

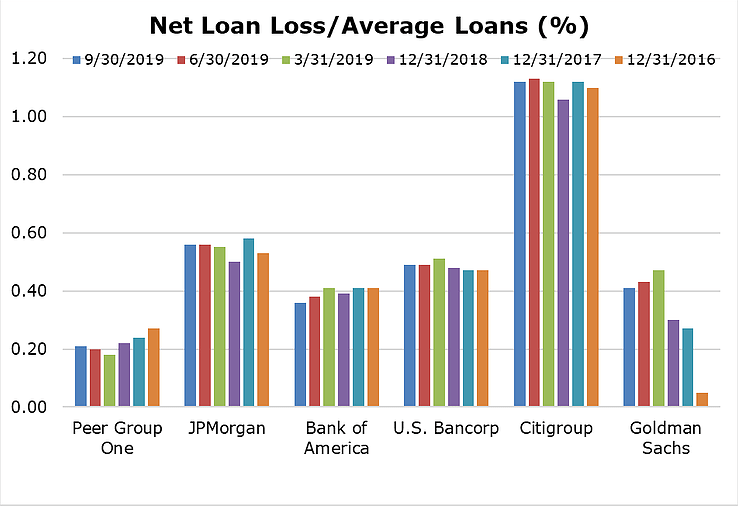

Part of the reason that BAC’s recent financial results don’t compare so badly with its asset peers is that the bank has managed to keep credit losses very low. As part of the campaign by management to de-risk the bank, the CSUITE at BAC has avoided taking any appreciable credit risk, resulting in lower provisions for loan losses and lower asset returns overall. The chart below shows net loan losses as a percentage of average assets.

Despite the significant slippage in the asset returns for BAC, CEO Brian Moynihan remains optimistic. He told investors during the bank’s Q4 2019 earnings call:

|

“How do you run a company, a big bank, and deal with lower rates? Well, we drive what we can control with our sempiternal commitment to responsible growth. We drive more loans, more deposits, more assets under management, and driving growth for the right pricing and at the right risks." |

The bottom line with BAC is that the heady days of double digit equity market returns in 2017 and 2018, which were driven by dramatics decreases in overhead expenses, are behind us. BAC remains less efficient operationally than its large cap peers and it gets horrible pricing for its assets. More, the slippage in the bank’s asset returns over the past year suggests that BAC may be even more negatively impacted by the Fed’s low rate policy than other large banks.

Brian Moynihan needs to boost the bank’s asset returns and the only way to do this is to take more risk. The re-opening of BAC's correspondent lending business is a reaction to this trend, but making more residential mortgage loans is not going to solve the problem. The commitment to responsible growth sounds good, but does not deliver the goods when it comes to earnings.

We have a neutral risk assessment on BAC and will be prepared to downgrade the name to negative should asset returns continue to fall.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington.

This piece does not necessarily reflect the opinion of Hedgeye.