A quick note from Restuarants analysts Howard Penney and Shayne Laidlaw:

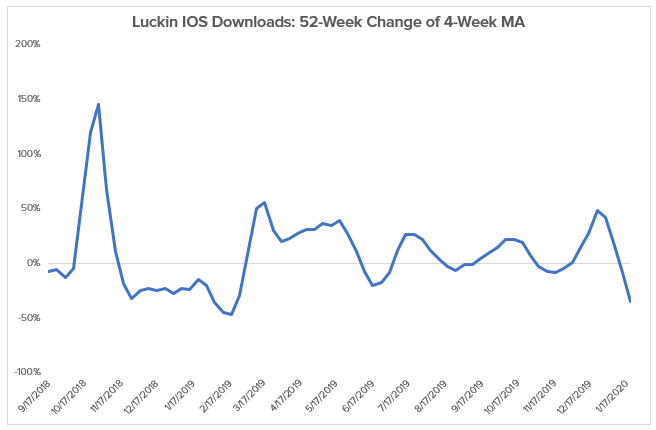

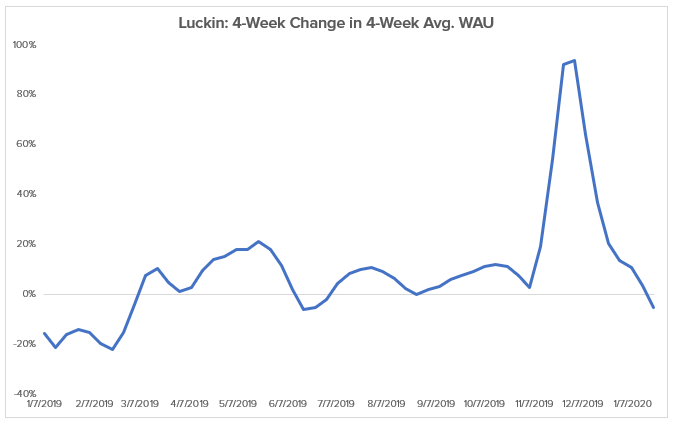

We are removing LK from the Hedgeye Best Ideas List as a LONG and making it a LONG bias until the dust settles. The app data from Sensor Tower is showing a collapse in downloads, and given the turmoil in China, the chance of the company getting to profitability in 3Q20 is slim. As of Friday, add to the list of headwinds, an organization somewhere in the world wanting to bring down the company. We estimate that whoever produced this report spent upwards of $5.0 million to do so.

The extent to which someone put together the resources, time and human capital to produce this report are as extraordinary as the LK store growth story. After going through this report, it is clear to us that a big powerful organization is behind this report and they don't want their name to be associated with it. I'm sure this is not the last we are going to hear from the unnamed author.

The depth the author(s) went in an attempt to prove fraud was so extraordinary, there are parts of the story that seems impossible to accomplish in such a short time. There are some places where I can find some inconsistencies, but it will take more time to look.

Here is what the report is claiming they accomplished in 4Q19:

- Hired 92 full-time employees and 1,400 part-time staff on the ground in China.

- Watched over 11,000 hours of video of recorded store traffic and counted the customers in the stores.

- Has taken over 25,000 pictures of LK Chinese customer cell phone receipts.

- Recorded that data in a spread to conclude management is manipulating the data and committing fraud.

- Did a detailed study of the Chinese coffee and bubble tea markets.

LK came on the coffee scene by taking advantage of the growth in the Chinese coffee culture built by Starbucks over the past twenty years. The long case for LK has been the 100% digital ordering platform is driving incredible customer data over a fast-growing store base and using that customer data strategically to drive higher ASP and more transactions per store. Not surprisingly, the centerpiece of the short thesis accuses management of fraud by claiming they are inflating the number of items per store and average selling prices, among other things. The last 30 pages of the report claim Starbucks has a better business model and that the Chinese don't drink coffee.

Lastly, at the time of the IPO, concerns about the management team and their background were well known. So, by rehashing these stories about management there is sensational nature to this report.

Two people at Hedgeye can't take on a team of thousands in two days, but here are some thoughts around the critical aspects of the report.

The report claims to have over 11,000 hours of video recorded of store traffic and over 25,000 customer receipts. Given that LK is 100% digital, they are claiming to have amassed pictures of over 25,000 cell phones and the associated LK transaction in just three months. Then input all that data into spreadsheets and analyzed the data, again all in only three months.

FROM THE REPORT: "We mobilized 92 full-time and 1,418 part-time staff on the ground to run surveillance and successfully recorded store traffic for 981 store-days covering 100% of the operating hours of 620 stores."

Hiring this many people is an extraordinary claim and something I have never witnessed. The data collection they claim to have gathered and analyzed would require this firepower.

FROM THE REPORT: "Below is the full result of our 981 store-days. We have 11,260 hours of recorded store traffic data to back this up."

The store observations (customer counting) leads them to claim that:

FROM THE REPORT: "the calculation of the national average number of orders per store per day using the results of our 981 store-days' tracking, arriving at 230. Multiply it by Items per order 1.14, and we get the number of items per store per day of 263. The 263 number is well below management's claim of 444 per day in 3Q19."

I agree that the number of items sold per day is a critical measure in determining LK success. With SBUX selling close to 900 per day, a coffee shop can do that without having the digital engineering that LK has built. The data source cited for the above claim is "offline footage tracking," which I'm assuming is someone they hired to stand in front of the store with a video camera for twelve hours. So the authors are claiming that the workforce they mobilized:

FROM THE REPORT: "for each of the 981 store-days we tracked, our staff usually sits in the store with a direct line of sight to the collection counter and counts the number of customers picking up Luckin products while recording the video."

It is important to note here that the authors gave management an out to prove the report wrong since there are "eight internal surveillance cameras in each of Luckin's stores covering it with no blind angle." To take this one step further, if management is a fraud, they can fraudulently produce videos of stores doing 500-600 items per day.

FROM THE REPORT: "As all orders are placed and paid online and picked up offline when an order is placed, a three-digit pick-up number and a QR code will be generated to facilitate the in store pick up. This method cannot be used if Luckin intentionally jumps and skips numbers during the day to purposely distort the tracking."

The claim here is that management is inflating orders by intentionally skipping numbers during the day. They further go on to say:

FROM THE REPORT: "we also have more than 10 video evidences recording real-time order jumping processes in-store. Though we can't publish the videos due to privacy reasons."

Who's privacy are they protecting or are they protecting a very large organization out to bring down LK. They are also claiming that they tracked 151 stores "offline" presumably using the same workforce from above and was the first customer to place an order and the last customer to place an order during that day to get the "online" order numbers. The ability to pull this off is extraordinary.

FROM THE REPORT: "From 2019 4Q, we gathered 25,843 customer receipts from 10,119 customers in 2,213 stores in 45 cities."

How did they physically do this? Ask people for there phones and take a picture of their LK order? The chart on page 26 shows the time frame from December 2017 to April 2019, but the data collected was from 4Q19. The report shows pictures of phones they supposedly collected. It almost seems physically impossible to do this in just three months and analyze the data. From these receipts, they are attacking the ASP and the number of items sold in the stores.

On page 26 of the report, the report says, "from 4Q19, we gathered 25,843 customer receipts." I'm assuming that means in 4Q19 the collected the receipts, yet a chart on page 26 citing the receipts has dates from December 2017 to April 2019. The dates on the chart don't coincide with the times they said they collected the data.

Keep in mind that LK was not found until October 2017. Did they think LK was a fraud before the company got off the ground?

In sum, the evidence they presented to support a smoking gun that the company inflated the number of items sold per store, the items per order and ASP, appear to be gathered in such a manner that it's hard to believe that the numbers are believable. Unless your goal is to bring down the management team.

The report takes ten pages (pages 55-65) to attack the credibility of the management team and its previous experiences and companies they have worked for previously. None of the information presented in those ten pages revealed anything new to the market, and most was well known at the time of the IPO. It’s sensationalism and trying to tie back to the beginning of the report, accusing the management team of fraud.

In the second part of the report (pages 66-89), the author opines on the coffee and tea market in China and compares Luckin to Starbucks about the coffee market in China. The author also offers up some thoughts about the differences in the SBUX business models and that of LK. None of these thoughts are smoking guns, and it’s just one person's opinion about the viability of the business model. Everybody is entitled to a conclusion, but that is all it is, an opinion.