The balance of the year could prove difficult from a cost perspective. The consumer comeback that casual dining management teams have touted may also be running on fumes.

Casual dining sales slowed in April and we are hearing that May’s numbers are not showing stronger trends. Officially in April, the Malcolm Knapp data showed that two-year trends slowed sequentially from March.

The trends in April and May suggest that the rate of change in improvement in sales trends is slowing just when the industry needs it most. As you will see in the following charts, the industry benefited from declining food prices in 2009. Labor costs were also somewhat benign as turnover rates slowed in the recession.

As we get closer to the outlook for 2011 (Q2/Q3 conference calls), higher food costs will dominate the headlines. In addition, if the jobs picture really improves it’s only a matter of time before we hear about higher labor costs. In an economy that is creating jobs, there is an increased incentive to quit and walk away from a lower-paying job (think restaurant server/cooks) increases and the restaurant industry will pay the price.

There is also a case to be made that the improvement we have seen in sales trends is somewhat artificial, or said another way, it’s the SQUATTERS’ INCOME impact. A New York Times article entitled “Owners Stop Paying Mortgages, and Stop Fretting” details just one example of unsustainable consumer spending patterns. The article describes how for some homeowners that chose to halt mortgage payments, foreclosure has allowed them to “stabilize the family business. Go to Outback occasionally for a steak. Take their gas-guzzling airboat out for the weekend. Visit the Hard Rock Casino.” One individual stated, “instead of the house dragging us down, it’s become a life raft. It’s really been a blessing.”

Additionally, as our Hedgeye Risk Management BLACKBOOK on the consumer (released yesterday) illustrates, the consumer is facing a myriad of other headwinds. For a copy of this BLACKBOOK, please email sales@hedgeye.com.

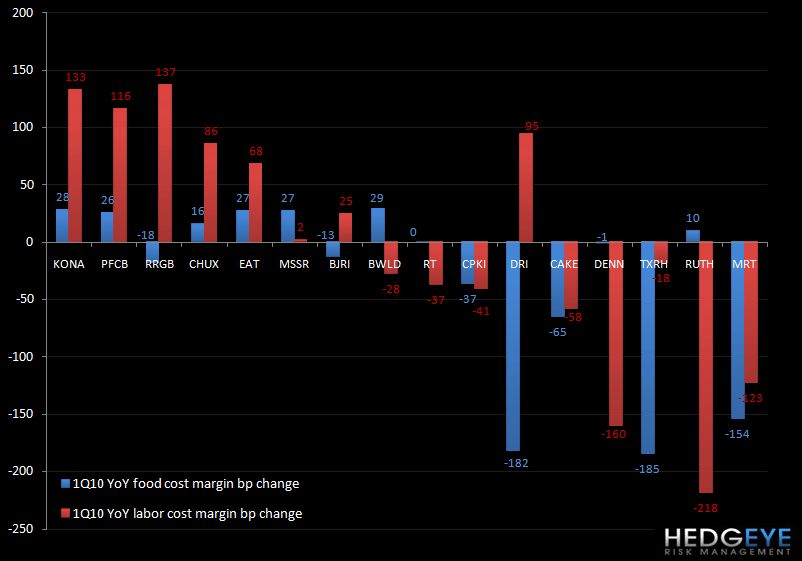

From a cost perspective, restaurant companies face difficult comparisons over the next few quarters. As the first chart below shows, average food costs as a percentage of sales for casual dining decreased significantly through the first three quarters of 2009. While the first quarter saw further year-over-decline in food cost margin, the compares become increasingly difficult through the third quarter. Some restaurant companies have indicated that costs have been trending higher than was expected at the outset of the year. Two components that were cited specifically by management teams during the recent earnings calls were alcohol (MSSR) and chicken (RT).

While most companies are under long-term contracts for beef, as new contracts are negotiated, nearly every company will be paying higher prices in 2011.

Some companies that are looking vulnerable coming into the 2Q earnings season are CAKE, RT, TXRH and to a lesser extent DRI.

In terms of labor costs, 2Q will likely bring significant labor cost year-over-year growth to the casual dining space. Many companies saw year-over-year labor cost inflation in 1Q10. DRI, PFCB, KONA, and RRGB had labor costs jump 95 bps, 116 bps, 133 bps, and 137 bps, respectively. MRT saw deflation of 123 bps in labor costs.

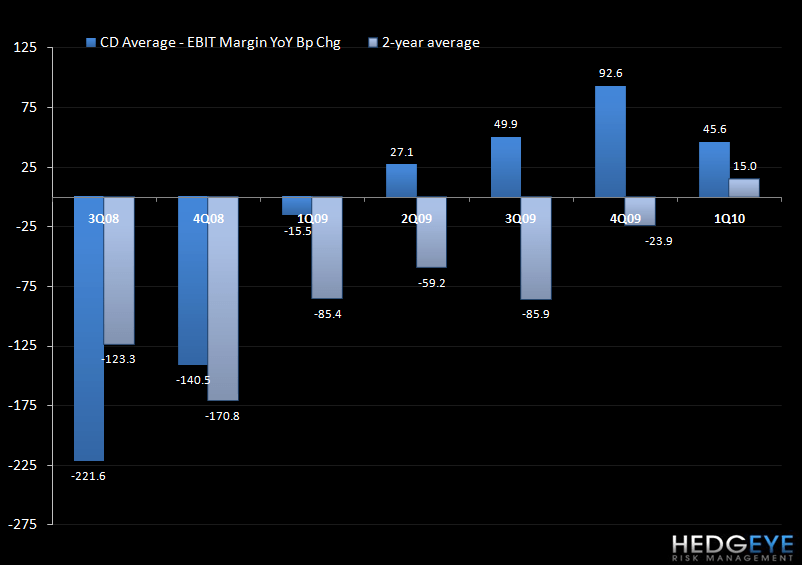

Examining the EBIT margin trends in casual dining paints a vivid picture; the category is facing increasingly difficult margin compares for the rest of the year. 1Q10 was the last easy comp and many companies operating at peak margins will find it difficult to sustain those levels. Those that jump out for me include CAKE, MRT, and TXRH.

Howard Penney

Managing Director