This guest commentary was written last night by Mike O'Rourke of JonesTrading.

It was often said during the 20th century that the Chairman of the Federal Reserve was the most powerful person in the world outside of the President of the United States. Almost no one would deny that the Fed Chairman was the most powerful unelected official in the world.

The post crisis era of the past decade has been the Golden Era for central bankers. The Global Financial Crisis and the Great Recession prompted both politicians and the global populace to cede extraordinary powers to the major central banks that would been unthinkable just 12-13 years ago.

Central bankers have effectuated trillions of dollars of asset purchases and years of negative interest rates, and pursued any policy necessary under the guise of “whatever it takes.”

These tools were sold to the public as temporary measures intended to get the global economy through trying times. Now that the major economies are more than 7 years removed from the last wave of the crisis, the policies are still in place for the sole purpose of achieving 2% inflation.

The Fed’s official Congressional mandate remains threefold. It is:

“The Board of Governors of the Federal Reserve System and the Federal Open Market Committee shall maintain long run growth of the monetary and credit aggregates commensurate with the economy's long run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.”

Note that over the past decade, Core PCE Inflation (the Fed’s preferred measure) has been above 2% a total of 11 times or 9% of the time. The reading has been below 1% a total of 3 times or 2.5% of the time.

That is price stability.

During the crisis, Chairman Bernanke unofficially broadened the Fed’s mandate through an activist interpretation to say that the Federal Reserve can respond to anything that risks diverting the economy from full employment or price stability. That unsanctioned interpretation (which lacks Congressional approval) has become embedded in today’s Federal Reserve.

In short, it is a case of mandate drift where the Fed Chairman can arguably pursue any policy he wishes if something is deemed a risk to the economy. The political powers in both the Executive and Legislative branch have fallen in love with easy money policies that facilitate re-election, thus oversight is absent. Any audit the Fed initiatives in Congress were drowned by excess liquidity.

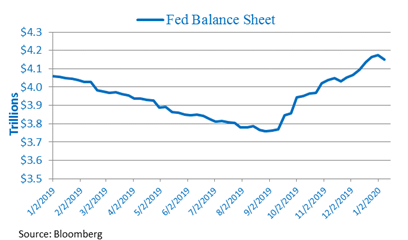

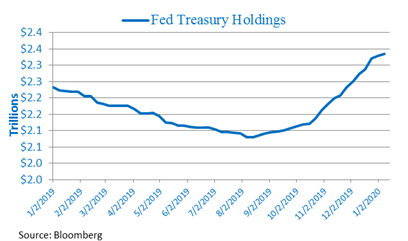

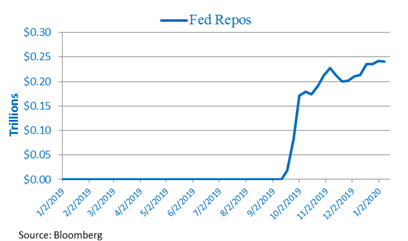

The WSJ published two stories today about the ongoing dislocation in the repo market. One is titled “The Fed (Mostly) Didn’t Cause the Latest Stock Market Melt-Up.” The line that illustrates the context of the article is “The answer is that the Fed probably isn’t the cause of the stunning rally in Tesla or stocks more broadly, at least in the usual way of thinking about causes. On the other hand, if the Fed hadn’t acted, the market would almost certainly be lower, possibly disastrously so.”

Thus, the Fed liquidity provided to the repo market is a real world manifestation of the “Fed Put.” Even more alarming was the article reporting that the Federal Reserve is considering lending cash directly to counterparties, including hedge funds through the repo market clearing house, the Fixed Income Clearing Corp. The heightened cash liquidity needs of these institutions whether they be hedge funds or smaller banks are the result of regulatory guidelines for the daily leverage they are incurring.

Furthermore, the lending capacity of the larger banks has been hampered by the post-crisis Liquidity Coverage Ratio rules. Thus, here we have banks attempting to adhere to post crisis solvency measures and the Federal Reserve stepping in to facilitate leveraged risk takers.

The September quarter end and year end were expected be the levels where the squeeze would be tightest, but the market continues to seek the Fed’s cash liquidity as it continues to provide it. If the Fed stepped back from providing the liquidity, leveraged positions would need to be sold. Someone needs to remind the Fed that that is called a “market.”

Obviously, considering the Fed’s penchant to throw ever growing mounds of money at problems, it would need to plan some type of gradual taper to allow for the unwind of the leverage (whose growth it has facilitated). Regardless, it is time the Federal Reserve is again accountable to oversight.

If it continues to view every free market function in the financial system as a threat to the economy, before long there won’t be a financial system left.

* * *

EDITOR'S NOTE

This is a Hedgeye Guest Contributor research note written by Michael O'Rourke, Chief Market Strategist of Jones Trading, where he advises institutional investors on market developments. He publishes "The Closing Print" on a daily basis in which his primary focus is identifying short term catalysts that drive daily trading activity while addressing how they fit into the “big picture.” This piece does not necessarily reflect the opinion of Hedgeye.