Take it as a data point or it may just be speculation, but the Starbucks bloggers are talking about insufficient staffing levels. I would not even highlight this if so much of the margin recovery story at SBUX was not built on cost cutting. To that end, the company continues to surprise to the upside with its cost cutting initiatives.

From a Starbucks blog; “apparently there is such a staffing crisis at the SM (Store Manager) level in the DC area that several SMs in the Mid-Atlantic are being recruited to travel down to DC, all expenses paid, for a period of two months to help run the stores until ASMs and RMTs are ready to assume those positions. One of the SMs I know is going.”

More important for the Restaurant industry as a whole is the trend in turnover rates if the economy and the job picture gains momentum. In an economy that is creating jobs there is an increased willingness to quit and walk away from a lousy job, and the restaurant industry will pay the price.

For now, however, we don’t have much to worry about. As our Financials Analyst, Josh Steiner, wrote today “Consistent with the trend year to date, claims remain in their ~450k range, too high for unemployment to improve meaningfully. This morning the reported number fell 14k to 460k, down from last week's revised print of 474k, and higher than consensus of 458k. Rolling claims climbed 2k to 457k week over week. Remember, we need to see initial claims fall to a sustained level of 375-400k in order for unemployment to fall meaningfully and, by extension, lenders' net charge-offs to return to normalized levels. We remain well above that level.”

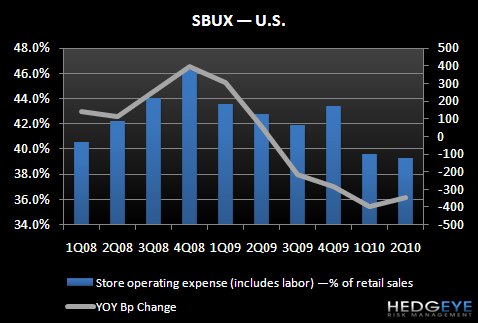

Cutting costs too deeply is a whole different issue. Based on SBUX’s improving same-store sales trends, I had not been under the impression that the company was cutting costs to the extent that it was detrimental to the customer’s experience. In the most recently reported fiscal 2Q10, store operating expenses (including labor costs) as a percentage of retail sales decreased 350 bps YOY in the U.S. Management attributed the YOY decline to “sales leverage, the closure of underperforming stores and the continued application of lean principles in our store labor deployment. Lower benefits expenses related to health and welfare programs, which tend to vary from quarter to quarter also contributed to the improvement. As a result of the lean work to-date, productivity and customer satisfaction have both improved dramatically compared to last year. We continue to refine these important activities as many of them are customer facing. In addition we have other initiatives under way such as a new labor scheduling tool and a new point-of-sales system that we expect will further increase productivity once fully implemented.”

It will be important to monitor whether customer satisfaction scores continue to improve to ensure that the company’s cost cuts are sustainable and not a result of management “pulling the goalie” to improve margins. I don’t think this is the case, however, as management seems focused on improving the customer experience and sequentially better same-store sales and traffic trends seem to reflect that renewed focus, but insufficient staffing levels would be concerning.

Howard Penney

Managing Director