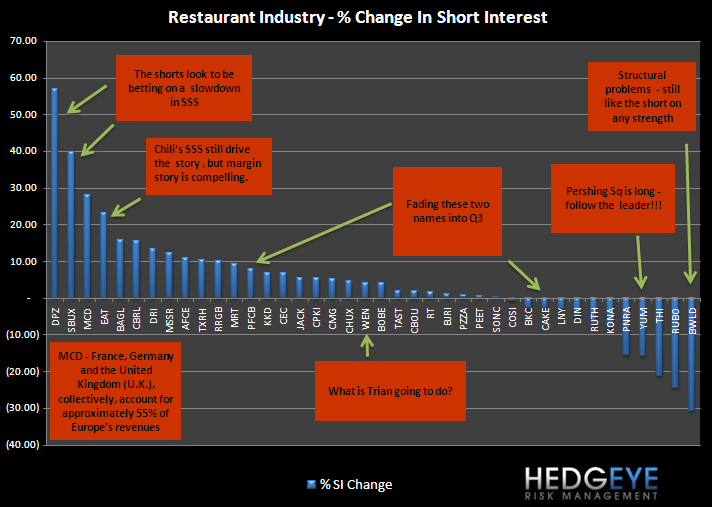

Of the 40 companies we track, 70% of the companies saw an increase in short interest in the past month (43% of the companies were in the QSR sector).

Of the 40 companies we track, 70% of the companies saw an increase in short interest in the past month (43% of the companies were in the QSR sector).

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.