Position: Long Germany (EWG); Short France (EWQ)

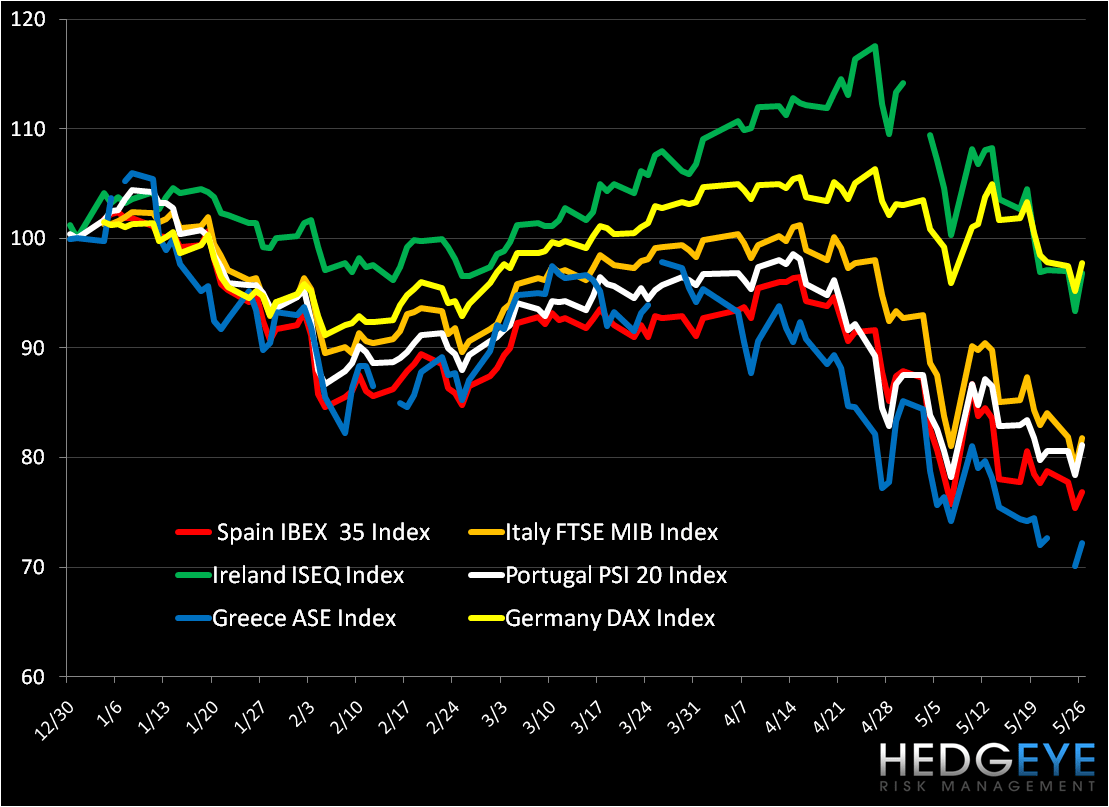

As part of our Q2 theme Sovereign Debt Dichotomy, we advised that one possible play on sovereign debt risk in Europe is to be paired off long Germany and short Spain. Our bullish thesis on Germany included a tighter fiscal balance sheet than many of its European peers, the advantage of a weaker Euro for an export-heavy economy, low inflation, and a stable rate of employment. While we’ve seen significant divergence in the underlying German and Spanish equity markets over the last weeks, including a spread as wide as 2000bps between the DAX and IBEX 35 on May 7th, the increasingly larger share of the ‘bill’ that Germany will bear for the Eurozone’s collective bailout is bearish for German capital markets (see chart 1 below).

Since our initial conference call on the dichotomy on 4/16 we’ve traded around Spain on the short side (we are current short France in our model portfolio) and recently have seen weakness in reported German fundamentals. Further, from a tactical position, our TAIL line of support for the DAX at 5,639 could soon be tested with a close today of 5,758.02, and our TREND line of support at 5,928 is already broken (chart 2).

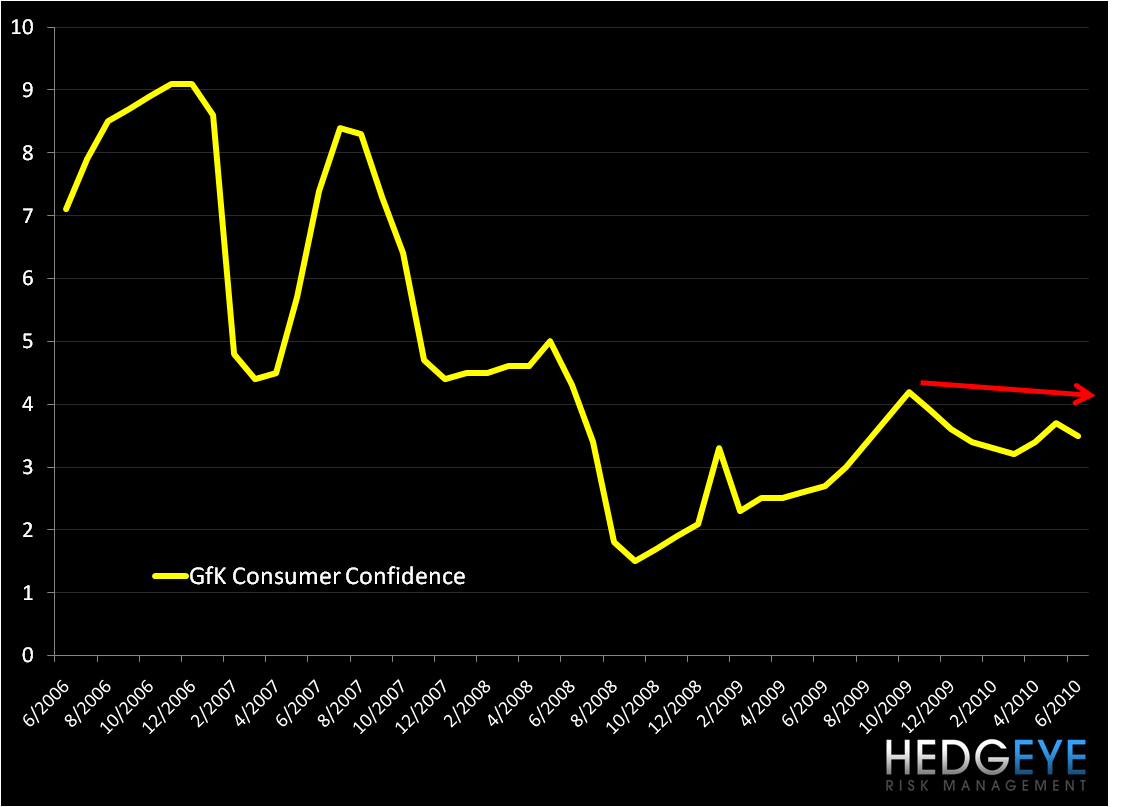

Today, the GfK German Consumer Confidence survey for June fell to 3.5 from 3.7 in May (chart 3). Last week German PMI contracted; services fell to 53.7 in May from 55.2 in April and manufacturing dropped to 58.3 versus 61.5 in the previous month. Also, earlier last week, the ZEW economic sentiment survey, which forecasts for 6 months ahead, fell to 45.8 in May versus 53.0 in April.

While the German unemployment rate remains positive, declining in the latest reading to 7.8% (versus the Eurozone average of 10% and 20% in Spain) and is underpinned by the government’s successful part-time labor programs, contagion from European sovereign debt risk persist despite the $1Trillion European loan/debt buy-up facility issued on 5/9. Additionally, Germany’s unilateral ban on naked short selling on 5/25 is adding fuel to the fire and enhancing market volatility.

On the margin, the fundaments we’re following in Germany and the broader stock market suggest a downward reversion to the mean, especially as risk in Europe (and globally) is pushed further out. One area to look to for confirmation of this is the bond market (chart 4), where we’re starting to see German yields rise.

Matthew Hedrick

Analyst