R3: REQUIRED RETAIL READING

May 26, 2010

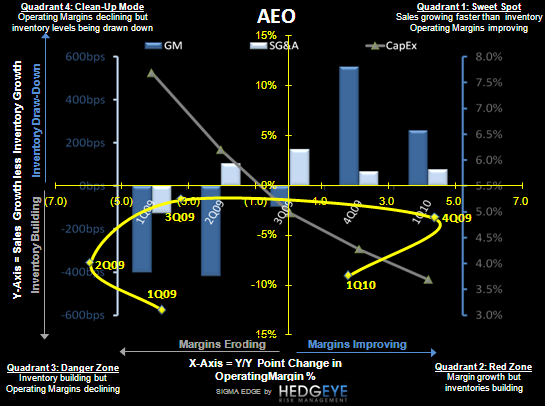

TODAY’S CALL OUT

This morning American Eagle Outfitters reported a largely inline quarter, with EPS of $0.17 coming in at the high end of the company’s guidance and on target with the Street. By now this is old news and hardly surprising given the updates we’ve gotten along the way with each monthly sales report. However, there are two incremental data points that stand out from the release. First, guidance for 2Q is well-below the Street, with the new forecast of $0.12-$0.16 falling below the consensus of $0.21. Secondly, inventories are on the rise. On a sales increase of 8%, inventories were up 16.9%. Management chalks this increase up to a strategic initiative to have a better in-stock position on denim as well as comparisons with last year in which inventory was down 4% per foot.

No matter how we look at it, this stands out as one of the few mall-based retailers actually committing to inventory build in advance of any potential (i.e. hopeful) acceleration in sales. Add in the fact the company has now shed its loss producing division, Martin & Osa, and it’s a bit curious to see inventories on the rise when guidance is on the demise. In fact, AEO is the first company we’ve seen out of earnings season to take a haircut to 2Q earnings based “margin pressure related to weaker trends early in the quarter.” Perhaps this is a company specific issue, as much of the past year AEO has lagged its peers in the area of inventory management, but this is a data point worth keeping an eye on. This could be a lull or the beginning of a trend. Either way, there’s 6-8 weeks before the key back to school season kicks in and it’s fair to say some doubt should begin to enter the minds of both investors and retailers.

Eric Levine

Director

LEVINE’S LOW DOWN

- Despite some chatter suggesting post-Easter business has seen a slowdown across the mall, PVH is not seeing this from their wholesale perspective. Management noted that the company’s customers across all tiers of distribution are still pulling orders forward to meet demand.

- DSW noted that the company’s loyalty program continues to grow and now totals 14 million members. Clearly the program includes DSW’s most loyal customers as indicated by the fact that 86% of revenues are derived from those carrying loyalty cards. Efforts to mine the loyalty database and segment promotional offers are still underway.

-Fashion accessory consumption, a key consumer discretionary barometer, is on the rise as indicated by NPD data with sales up 17% in Q1 compared to a 10% decline in the same period last year. Notably, larger ticket items like women’s handbags drove the outperformance of women’s accessories up 20% during the quarter.

HEDGEYE CALENDAR

MORNING NEWS

ICSC Lowers May Monthly Sales Target - The International Council of Shopping Centers said U.S. retail sales in May are so far coming in worse than originally expected. It now expects sales during the month to be up 2% to 2.5% vs. previous estimate of 3.5%. The reason for lower the estimate was inconsistent traffic trends and softer consumer spending. Some chains said that a later Memorial Day holiday will shift some sales from May into June. <sportsonesource.com/news>

Kevin Garnett Switches From Adidas to ANTA - Despite signing a "lifetime endorsement deal" with adidas in 2003, Boston Celtics star Kevin Garnett has reportedly signed an endorsement deal with the Chinese-brand ANTA for the coming season. <sportsonesource.com>

Obama Signs Haiti Trade Bill - President Obama has signed into law a bill that almost triples the amount of apparel made in Haiti that can be shipped into the U.S. duty free. The bill is intended to help Haiti, the poorest country in the Western Hemisphere, rebuild after the devastating earthquake in January that disrupted the mainstay of its economy — the apparel and textile industry. The sector accounted for two-thirds of Haiti’s exports and almost 10% of GDP. Apparel and textile imports were $513.3 million in 2009. <wwd.com/business-news>

Perry Ellis Brings Business In House - Perry Ellis International is bringing its dress shirt business in-house, ending its license with Smart Apparel (U.S.) Inc. at the end of this year. On Jan. 1, 2011 Miami-based PEI will assume all aspects of the business under the Perry Ellis and Perry Ellis Portfolio brands. Smart Apparel, which made Perry Ellis dress shirts for two years, will continue to produce Perry Ellis branded suits, suit separates and sport jackets. <wwd.com/menswear-news>

Wal-Mart Cuts Apple's iPhone Price - Wal-Mart Stores Inc., the world’s largest retailer, cut the price of Apple Inc.’s iPhone 3GS by $100 to $97 before the possible introduction of an upgraded version of the device. The deal is available in stores and not online, Wal-Mart said on its website. It requires a two-year service contract, Melissa O’Brien, a spokeswoman for the Bentonville, Arkansas- based retailer, said in an e-mailed statement. The reduction may also be aimed at clearing unsold iPhones before Apple unveils the next iteration. <bloomberg.com/news>

84% of Women Plan to Increase Spending as the Economy Improves - Among the top items they plan to purchase are electronics, clothing and accessories, according to a new survey. <internetretailer.com>

Burberry Group Profits for Year Fuelled by a 6.5% Sales Growth and Cost Efficiencies, Boost 2011 Capital Spending - The fastest growing category was non-apparel, which accounted for 36% of revenue. Burberry plans to build on its strong financial position by accelerating investment in growth initiatives in retail, digital, and new markets, while continuing to enhance the brand. The company added that in the current year, capital expenditures would nearly double and be spent in part on new stores and refurbishment as well as expanding key product areas including kidswear and moving into emerging markets. <wwd.com/business-news>

Steve Madden to Find New Designer through MTV - Steve Madden has enlisted the help of MTV to find the newest member of his design team. On the cable network’s new show, “Hired,” tonight at 6:30 p.m., Madden chooses between five recent graduate contestants, each vying for a position at Steven Madden Ltd. The candidates each meet with a recruiter, who provides suggestions and tips, before they meet with Madden himself for an interview. The final round includes an additional interview and hands-on activities at the Long Island City, N.Y.-based headquarters. One lucky winner will be offered the job during tonight’s episode. <wwd.com/footwear-news>

Sneaker Con in New York - The lines were out the door for last Saturday’s Sneaker Con in New York, the third edition of the celebration of all things sneaker. According to organizer Yu-Ming Wu, more than 1,000 sneaker fans flocked to Manhattan’s Sullivan Street to buy, trade and ogle some of the most sought-after kicks around. Sponsored by New York retailer Dr. Jay’s and by Adidas Originals, the meetup featured 40 vendors hawking their wares, as well as an exclusive look at rare Kaws toys from the private collection of Lev Levarek from Toy Tokyo. <wwd.com/footwear-news>