In the midst of market jitters, European concerns, and a flurry of retail earnings reports, Foot Locker delivered a solid first quarter. Results were well ahead of the Street, driven by three key factors. First, sales came in slightly better than expected, with same store sales up 4.8%. Domestic results came in ahead of expectations while international was at the upper end of plan. Secondly, gross margins came in better than expected, improving by 140 bps. Recall that the coming out of 4Q, inventories were in the best shape they’ve been in nearly a decade from both a quantity and quality (aged) standpoint. Finally, SG&A expenses were only up slightly on a dollar basis (essentially flat) and leveraged by 100 bps due to the 5.3% increase in total sales. All in, this represents a solid start to the company’s turnaround and it’s encouraging to see early positive results from the company’s strategic efforts.

The biggest criticism here is likely the fact that the entire athletic footwear and apparel space appears to be producing similar, if not better, results. While this is true and well documented, we continue to believe the COMBINATION of Foot Locker specific drivers such as improved apparel assortments, distinct banner segmentation, and inventory management will ultimately lead to a continued string of upside over the next several quarters. Importantly, this is the first quarter to be reported since Ken Hicks unveiled the company’s strategic plan on March 9th. As such, management remains conservative with its forecast on both the top and bottom lines, preferring to use a still “uncertain economic” backdrop as a reason for which to be reserved. While management may be conservative, we are more aggressive both on the opportunity to see meaningful earnings upside over the next couple of years as well as the commensurate opportunity for share price appreciation. Our estimates remain comfortably ahead of the Street for this year at $1.05 vs. $0.87. We’d use the market weakness and any healthy skepticism surrounding management’s conservative outlook to revisit the intermediate term opportunity.

A few highlights from the call on Friday:

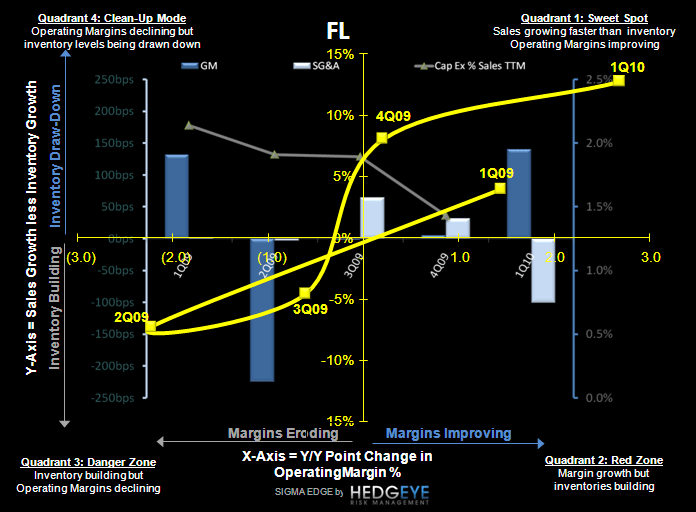

- FL remains in the very early stages of reaping the gross margin benefits from reduced promotional activity. The result should be continued improvement in gross margin rate as well as the opportunity to strategically re-direct markdowns toward clearing slower moving SKU’s. Importantly, 1Q was only the second quarter in almost a decade in which sales grow faster than inventory.

- Lady Foot Locker (LFL) was called out as having the best performance domestically. Recall that LFL has received the most attention so far as it pertains to an upgraded apparel strategy. Yes, excitement from the toning category does help, but the opportunity to convert traffic into additional purchases by the female customer is the holy grail. There are early signs of success here and we believe this is still early in the process of upgrading the brand’s merchandise and image.

- With the Easter shift in the past, early May sales are trending towards a mid single digit increase through two and a half weeks. Recall that comparisons become increasingly easier over the next two quarters, with FL posting its worst quarterly same store sales results in history in 2Q09 and 3Q09, down 12.1% and 8.1% respectively. Putting easy compares aside, even a modest comp store increase with similar gross margin assumptions to 1Q gives us an earnings estimate $0.10 head of the Street. We shake out at $0.15 vs. the Street at $0.05.

- Performance/technical running remains a key category, with management noting that the trend towards this higher price point footwear accelerated in the quarter. This bodes well for future sales growth, as these products are accretive to ASP’s. Furthermore, management confirmed that a new and innovative product pipeline across a variety of suppliers is key to the momentum exhibited in the category.

- Management noted that the company is about 30% through the efforts to reposition the company’s apparel offerings and should be closer to 50-60% complete by the Fall season. Domestic apparel sales, while still down low single digits, showed a huge improvement in trend from 4Q’s double digit decline. We continue to believe the opportunity to improve apparel sales will be meaningful to both the top and bottom lines. Lady Foot Locker is most developed here but we expect to see additional efforts in place for back to school across additional nameplates.

- With 68% of the company’s business tied to Nike, it was encouraging to hear “the relationship [they] have right now is probably the best it’s been in some time”. Importantly, this echoes positive commentary from Nike’s team on recent conference calls and at the company’s analyst day. A healthy NKE/FL relationship goes a long way not just for these two companies, but for the entire competitive set. We continue to believe exclusive content in the form of merchandise, marketing, and actual store formats (i.e. House of Hoops) will further develop in partnership between the two companies.

- Eric Levine, Director