This is a Hedgeye Guest Contributor piece written by Tim Boyd of Delphi Capital.

A funny thing happened on the way to the President's "Bean Deal": the Dollar put in a long-term top. Well, that's what we suspect anyway, begging your pardon for the melodrama.

There are a lot of moving parts here so let's start with an observation that would be regarded as depraved heresy by the U.S.government: inflation is not only back, it's accelerating sharply. This could cause a whole lot of trouble for the Fed (and risk assets) down the road, but for now it's actually put a healthy dose of blush back into the cheeks of commodity prices.

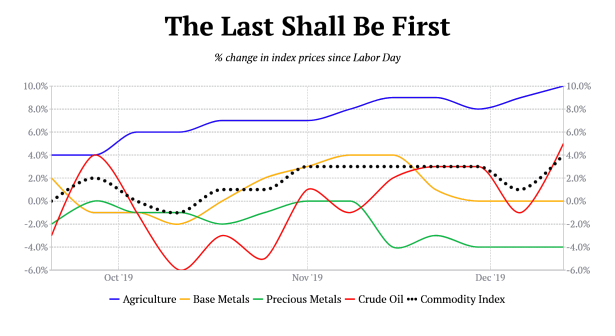

It's worth noting that sad-sack agriculture has led the way up this autumn; when the red-headed stepchild of commodities captains such a charge attention must be paid. We'd also highlight the fact that the rally has taken place relative to all major currencies, including the Loonie and the antipodeans (all of which are considered "commodity currencies").

In other words, this isn't a weak-Dollar story - it's a weak-fiat story.

What's made this upward surge even more impressive is that it's taken place in an environment of global growth deceleration. That being said, should we really be that surprised by such developments in light of the way central banks have been debasing their respective currencies since the financial crisis? No...but also yes.

No: what's happening is highly logical in light of said debasement. Yes: we've been waiting for the better part of a decade for the consequences of ZIRP, NIRP, and QE to show up in PCE - yet they haven't, at least not for any sustained period of time.

It's too soon to proclaim that an inflationary rapture is nigh, but there's every reason to suspect that something is different this time in light of the fact that the Dollar finally seems to be acquiescing to the domestic and international desire for a weaker greenback.

A weaker Dollar has many implications, most of them positive for risk assets in the near term. Emerging market bourses would be "yuge" winners from such a trend change since they'd be able to service and refund their Dollar-denominated debt with less local currency.

Indeed, we find ourselves all but forced to adopt a bullish stance on EEM and VWO and did in fact effect a pair trade featuring the former during Thursday's session (long EEM/short SPY). As the below chart suggests, EEM appears to be on the verge of breaking topside for a retest of its all-time high back in 2018.

We expanded our exposure to the inflation motif by going long three other ETFs vs. SPY, namely EWC (Canada), EWA (Australia), and ENZL (New Zealand), all of which are highly levered to commodity prices.

We cannot stress this next point enough: in our view, U.S. stocks are unlikely to keep pace with either their emerging market counterparts or the aforementioned commodity bourses as long as this nascent uptrend in inflation doesn't decelerate. That's a far cry from current consensus thinking, which remains tethered to the relative strength of the American economy with concomitant overweight positions in S&P 500 stocks.

Real U.S. yields have plummeted since Q4 of last year, which has resulted in steadily building pressure underneath commodity prices. Heading into Q4 of this year only gold and silver had benefited from the drop in real yields, but the rest of the complex now appears to be playing catch up.

While on the topic of real yields we should note that we unequivocally espouse the opinion that they're headed back into negative territory over the next 12-24 months. In our view this will be driven not by falling nominal yields but by a continued ramp in inflation. We realize that many Wall Street gurus are longing for a measure of vindication via a 10-year Treasury yield above 2%, and while that may in fact occur in the wake of "the best bean deal ever" we expect it to be only fleeting.

Simply put, Jay Powell & Co. are not dovish enough and that has set the stage for recessionary conditions in 2020. The fact that the Dollar has been routed since Wednesday's monetary policy decision speaks very loudly and very clearly: staying on hold now only makes it more likely that the Fed will have to ease next year. How will that play out against a backdrop of rising inflation?

Disingenuously at best. We will be told that a PCE over 2% (and let's not kid ourselves: real-world inflation is already well over that threshold) is healthy (which is true to an extent) and that additional rate cuts pose no danger (there's the disingenuous part) and are needed to support employment and GDP growth. Well, that last part is certainly accurate!

If we're right and real yields decline further in 2020 we'd expect to see most if not all commodity prices significantly higher by year-end. Gold and silver - given their special role as fiat pressure valves - strike us as the likely winners in that climate; base metals and energy, being more economically sensitive, should tag along but lag.

In general, the growing revulsion toward NIRP in Europe and the perma-ZIRP environment in Japan yield a situation where the Dollar is really the only G7 fiat with room to run on the downside because it's the only remaining member of that group with meaningfully positive interest rates attached to it! We'd add that technically, the Dollar Index looks like a good bet to visit the uptrend line originating in early 2011.

A break of that line may take some time but strikes us as reasonably likely by the end of 2020.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor piece written by Tim Boyd of Delphi Capital. This piece does not necessarily reflect the opinion of Hedgeye.