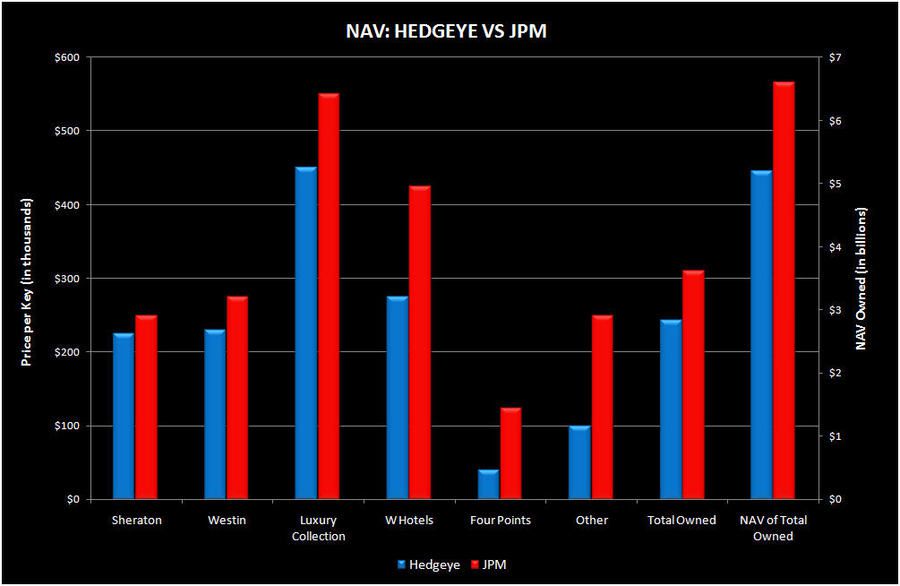

Our NAV analysis is more exhaustive, and we shake out at a lower NAV than “consensus”.

JPM, our consensus proxy, values HOT’s Owned Portfolio at $6.6 billion or approximately $310k per key. Given the firm’s aggressive $64 price target, we’d expect some pretty aggressive NAV assumptions. And boy, did we find some aggressive assumptions. Our NAV analysis values HOT’s Owned Portfolio at "only" $5.1bn or $241.5k per key or almost 18x 2010E owned, leased, and consolidated JV EBITDA. So why are we so "conservative" compared to consensus? For one, our analysis is more comprehensive including a review by our real estate consultant. Second, JPM makes a mistake assuming HOT owns all these assets outright. Some are joint ventures and leased hotels.

Sheraton

- We’re about $25k per key below JPM’s Sheraton valuation.

- The issue is that 7 of the hotels in this portfolio have over 500 rooms and with the exception of Sheraton Manhattan, the sheer size of the assets will cap their per key value. Excluding the Sheraton Manhattan, the other 6 assets make up 57% of the owned Sheraton rooms. For example, there aren’t many buyers for an asset like the Sheraton Centre Toronto Hotel for north of $300MM.

- Airport hotels comprise another 12% of the Sheraton room base. Airport assets typically fetch low per key values since they have no alternative "higher and better" use and attract a price sensitive customer. For example, Sheraton Suites Philadelphia Airport and Sheraton Gateway Hotel in Toronto Int'l Airport are unlikely to fetch more than $125k per key.

- There are only 3 assets in the Sheraton portfolio that we think would fetch north of $300K.

- The Park Lane Hotel, which we estimate, is worth $750k/key (leased)

- Sheraton Manhattan Hotel and Sheraton Diana Majestic Hotel (leased), which we estimate are worth $400k/key

Westin

- We’re about $45k per key below JPM’s Westin valuation.

- The largest HOT owned Westin is the Atlanta Peachtree Plaza. It would be tough fetching significant north of $100k/key for that asset given its size and the massive oversupply in the Atlanta market.

- Similarly, The Westin San Francisco Airport is unlikely to fetch more than $125k/key for the reason we already discussed above.

- We estimate that only 3 Westin assets would fetch north of $300k per key.

- The Westin Excelsior in Florence & Rome – roughly $500k/key

- Westin Dublin Hotel - $350k/ key

St. Regis Luxury Collection

- We’re about $100k per key below JPM’s Luxury collection valuation.

- The Phoenician, which is the largest asset in this collection, making up 26% of the Luxury collection rooms, is in need of material ($100MM) capital improvements and is in a challenged market. Arizona is only second to Vegas in terms of housing issues.

- St Regis NY is the jewel of this portfolio. We estimate that this asset would fetch $1.25MM/key. In addition to the NY asset, we believe that only the Italian assets and the St. Regis Aspen would fetch north of $500k/key. All in, these assets (including NY) represent just 31% of the rooms in the collection.

- Park Towers BA are also unlikely to fetch more than $250k/key, given the economic reality in Argentina.

- We’re pretty confident that St. Regis San Francisco wouldn’t fetch much more than $300k/key.

- While the Spanish assets are nice, they are in secondary cities and the economy is in crisis. We have them valued at $350k/key.

W Hotels

- We’re about $150k per key below JPM’s W Hotels valuation.

- Aside from the Times Square W, we don’t think a single asset in this portfolio is worth anywhere close to $425K/key.

- Several W’s have recently traded at $200k handles.

- 510 Keys or 18% of the W’s in this portfolio are at W’s in New Orleans. Even OEH’s Windsor Court traded for only $137k/key last year. JW Marriott in New Orleans traded for around the same per key price in 2008.

Four Points

- We’re about $75k per key below JPM’s Four Points valuation.

- Second tier markets and limited service – including and airport hotel… find me one asset that’s traded at 125k/key.

- The last Four Points that traded in July 2009 went for $14k/key (in Revere, MA); another traded in May 2009 for $16k/key (Minneapolis, MN).

Other Hotels

- Bottom line – JPMorgan’s estimate on this portfolio looks about $150k/key rich and doesn’t account for the fact that the largest asset is a JV.

- Starwood owns 6 non-proprietary branded assets. Most of these assets have material amounts of deferred CapEx.

- The largest asset in this group - Boston Park Plaza - is not wholly owned by Starwood. We believe that HOT owns 51% of the hotel. Given the size of this asset and the amount of CapEx a new buyer would need to invest in the asset, we think that it would fetch in the neighborhood of $125k/ key

- The Caesars hotels look like they haven’t had a refresh since the 80s; our real estate consultant pegs the value on those at $75k/key.

Since EBITDA is obviously depressed and current stock market valuations are huge, the bulls are using NAV to justify bulging price targets. Fair enough. Our comprehensive NAV analysis produces valuations well below what we consider consensus. The $66k per key differential between JPM and us translates into $1.4bn in equity value or approximately $7.50 per share. At our owned valuation of 18x EBITDA, it's hard to accuse us of being conservative.