Below are analyst updates on our fifteen current high-conviction long and short ideas. Please note we have added Guardant Health (GH) to the long side of Investing Ideas. We have also removed Netflix (NFLX) from the short side of Investing Ideas and removed Booking Holdings Inc (BNKG) from the long side of Investing Ideas. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

IDEAS UPDATES

AMN

Click here to read our analyst's original report.

The Hedgeye Health Care Team’s LONG Position in AMN Healthcare Services (AMN) can be broken down into the following three levels. At the macro level, health care stocks thrive in the current Hedgeye Macro #Quad3 outlook. At the sector level, the policy and health care labor demand drivers we projected for health care services, the sources of our utilization forecast for much of 2019, are finally being priced in. At the stock level, AMN is experiencing the growth and acceleration necessary to be successful in the current market environment.

AMN correlates tightest to forward consensus EPS. As consensus catches up to our internal estimates, we expect strong fundamentals, such as growth and acceleration, to push the stock price higher. This initial move will be followed by the machines which will continue to push the crowd into the stock, again boosting the price with a secondary wave. All of these assertions are backed by a significant number of data sets that we are constantly monitoring.

CNQ

We continue see Canadian Natural Resources (CNQ) as one of the most compelling opportunities on the long side in energy today. The business is on the back-end of a 10 year CapEx cycle, retains high FCF margins due to low operational costs and bitumen upgrading operations, has a repeatable, low decline asset base, and is shareholder focused. All in all, a rarity in North American E&P. Additionally, we see it as an interesting way to play our Macro Team’s call that Quad 3 and Long Energy will be a persistent theme over the coming quarters.

GH

Hedgeye CEO Keith McCullough added Guardant Health (GH) to the long side of Investing Ideas this week. Below is a brief note.

On down days (yes the US stock market still has those from the trumped up highs), we'll do what our risk management #process always has us doing, buying/covering on red.

Today we're registering a buy signal on a name Healthcare Analyst Tom Tobin's team likes on the long side. Remember, both Organic Growth #Accelerating (in a top-down GDP #slowing quad) and Healthcare (as a Sector Style) are longs in #Quad3.

Here's Tom's latest Institutional Research summary on Guardant Health (GH):

|

Our claims data pointed to revenue upside heading into 3Q19. Guardant stock had fallen from a peak of $110 to a low of $60 alongside the collapse in other Softbank names such as UBER. From our perspective, the key driver for GH shares was slowing revenue. Our analysis shows that the correlation between revenue and enterprise value, and more specifically the expected change between these metrics, is the key fundamental driver of the GH share price. For a TAM story, a tight correlation to revenue should not be surprising. If consensus isn't wrong, forward estimate trends will resume an upward expansion, taking the shares with it. |

MAR

Click here to read our analyst's original report.

We’d love to give you a few nuggets of optimism for the upcoming lodging earnings season regarding Marriott (MAR), particularly for the beaten down hotel REITs desperately in need of a catalyst. Sorry to disappoint but we got nothing. Our forward looking rate tracker and survey based, forward looking models suggest only one thing: further deceleration. We remain steady with our short.

GOOS

Click here to read our analyst's original report.

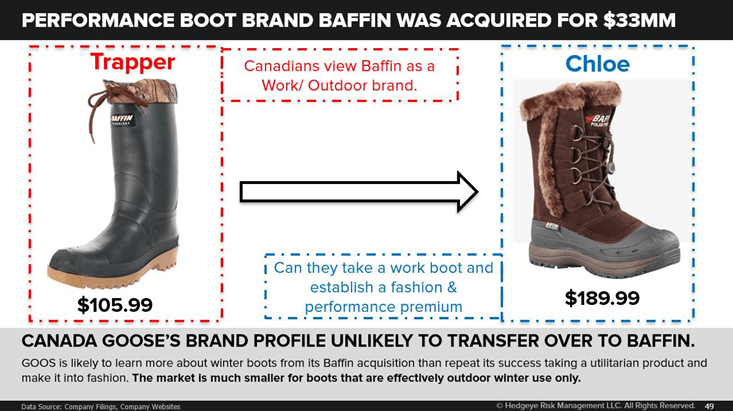

A year ago Canada Goose (GOOS) acquired Baffin, a winter boot brand. Management recently said that they were in no rush to launch their own footwear line. In a recent interview the CEO said, “It’s definitely not next year, but probably before five years from now. Somewhere between the two.” Canada Goose has expanded its offering to knitwear, lighter wear jackets, and most recently a high end jacket line. Footwear is an obvious extension, but it will bring lower margins and greater markdown risks as the other extensions have done.

There’s 500bps of margin risk as it pursues its growth initiatives. That leaves us with an earnings annuity between US$1.25-$1.50 and at a mid-high-teens multiple would represent a meaningful downside from here.

APHA

Click here to read our analyst's original report.

Aphria (APHA) CEO Irwin Simon talks a lot about building a long-term sustainable company in the U.S. over the last 25 years. Hain Celestial, the company he built, was merely a roll-up story, that he eventually destroyed through cost cutting, lack of brand investment and an eventual dry up in the well of small fast-growing companies he could tack on top to maintain top-line growth profile.

We think the same will happen to his plan with APHA, but investors may have already figured it out given the “discount valuation,” APHA is likely going to be a supplier of raw materials to extraction and branding companies in the future.

CMI

Click here to read our analyst's original report.

Cummins (CMI) has had 4Q19 estimates cut from about $3.40 to about $2.50… and the share price has actually gone up! From a local high in a share price, that would usually have generated significant alpha. For those planning to look through the truck cycle for CMI, that light at the other end is MD electrification, we think.

MDLA

Medallia (MDLA) completed its initial public offering of equity in July 2019. Despite being a ~19-year-old company, Medallia showed just two years of financial results to prospective investors in its S-1. Only in the recent investor frenzy for enterprise software IPOs could an omission of this magnitude be dismissed. Even Slack (WORK), which was a ~6-year-old company at the time of its’ listing (June 2019), shared more years of financial disclosure in its S-1.

We investigated and filled in the years of revenue disclosure missing in the company’s registration statement. We found decelerating annual revenue growth on both percentage and incremental dollars bases. Continue the initial short thesis.

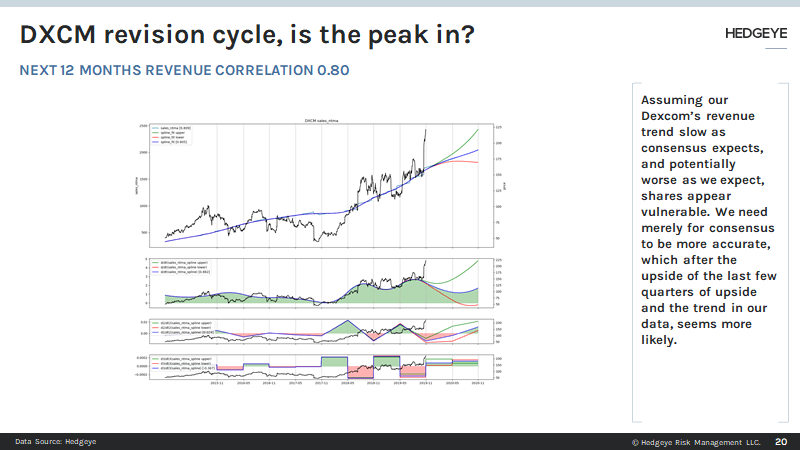

DXCM

Click here to read our analyst's original report.

You always remember the suspect oyster you ate a few hours ago as you run for a bathroom, and it is with similar clarity we remember our mistake with the Dexcom (DXCM) short. The mistake oyster in that case was sticking with the position as our claims data didn't fully corroborate the thesis. With the mistake already made, we've taken the time to have a closer look at the underlying continuous glucose monitoring (CGM) data in greater detail, and remain short DXCM as a result. Irrespective of your positioning, the data we've collected should be of interest, including a list of practices with the largest number of patients on CGM.

BLL

Aluminum cans! Everyone’s favorite cocktail party conversation. Ball Inc. (BLL) was in a growth industry around the time of the statement that “aluminum cans are better for the environment than bottles.” With this narrative there was expected to be above average growth.

News Flash: That is not what is currently happening. Sales are lower than a year ago, starting from the first half of 2018. Few cans were shipped, so in 2019 we saw against an easy comp what looks like mid single digit volume growth that kind of confirmed the idea of “cans are a growth industry.” They’re not. Over the 4th quarter and continuing further, we have very tough comps that make the growth story very difficult. Trucking rates are down. Marginal cans have been shipped and on a sequential basis we think it will be shown that it will not be a growth industry for BLL.

AXP

Click here to read our analyst's original report.

American Express (AXP) reported third quarter GAAP and adjusted EPS (diluted) of $2.08, up +11% Y/Y and +3% above street estimates for $2.02 / share. With net income up +6% Y/Y, owing to a +7% Y/Y rise in pretax income, the remainder of AXP's +11% EPS growth was driven by lower share count. Regarding consensus estimates, AXP booked a provision expense -13% below street numbers, largely powering the slight earnings beat.

SQ

Adjusted for the completed sale of Caviar to DoorDash on 11/01/2019, Square (SQ) issued adjusted revenue guidance for the fourth quarter of $571-$581, with FY19 guidance coming in at $2,095-$2,105. Management increased FY19 guidance, ex.Caviar, by +$35M and +$15M on the low-end and high-end of the previously given range, respectively. Relative to street expectations ahead of the print, the midpoint of management's new 4Q19 and FY19 guidance for the adjusted top-line of its core business (i.e. ex.Caviar) came in +2.4% and +0.8% higher, respectively.

DIN

There is so much hot air coming out of the Dine Brands (DIN) management team it’s hard to take them seriously. This quote from the CFO is a great example of what we are talking about.

|

“But in response to your question about what's going to take us to the next level for both brands, we see catering as the major opportunity because we think that space has been underserved.” |

Catering is not underserved and every restaurant company has a catering angle! If Chili’s sees accelerating revenues from delivery it’s going to come directly from Applebee’s. We remain firm on our initial #Quad3 short call going forward.

CHEF

Chefs Warehouse (CHEF) is an over-valued food service distribution roll-up story who’s better days are in the rear-view mirror. Since the beginning of 2012, CHEF has acquired 10 businesses and operating margins have gone from 6.0% to 3.2% over the same period.

The central tenant of our CHEF short has always been the sustainability of margins, especially EBIT margins. There is more clarity around that theme after the company reported 3Q19 earnings, which was yet another disappointing quarter. There is no change to our conviction, that given the optimism baked into consensus numbers for CHEF the stock remains a core SHORT.

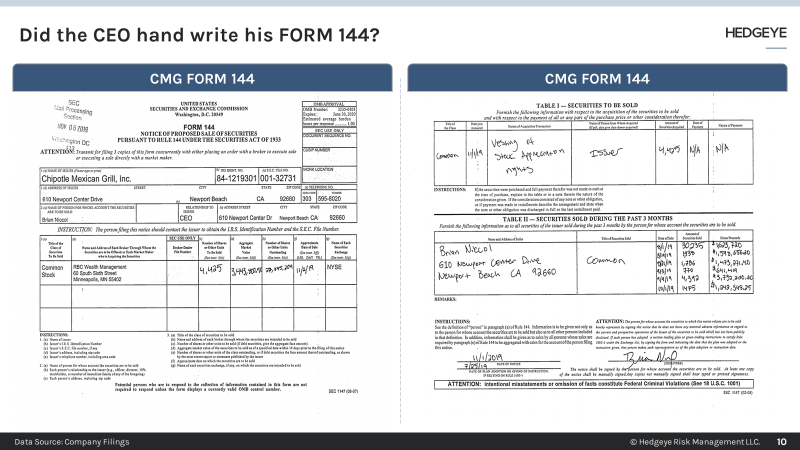

CMG

In the case of CMG, it’s not surprising to see insider selling given the run-up in the stock, as Pershing sold stock at the end of September. Now at the beginning of November the CEO is selling stock, but why would the CEO fill out the form by hand?

In the digital age, I would imagine that this took more time to do by hand than to do it electronically. If the CEO did fill it out by himself, what does it say about his ability to use technology? Put that in the context that CMG is leading the way for “digitally enabled” restaurant companies, and things just look weird and even a little bush league.