Who is going to stir the pot on WEN?

Over the years, Trian Partners has been extremely successful at creating value from mispriced securities. In the almost two years since creating the Wendy’s/Arby’s Group, it has now created one of those mispriced equities. Can Trian and senior management fix WEN again? Our sum of the parts analysis concludes that WEN is right back where it was in 2005 – except this time, there is no value in the current security for the Arby’s brand.

In 2005, Trian and a host of other high profile hedge funds, put pressure on Wendy’s management to unlock value by allowing the market to value the separate parts of the company (resulting in the spinoff of Tim Horton’s). Almost two years after the merger of the Wendy’s and Arby’s’ brands, the company finds itself right back in the same position. In 2005, the Tim Horton’s brand accounted for more than100% of the value of the equity, as compared to today when the Wendy’s brand accounts for more than 100% of the value of the company.

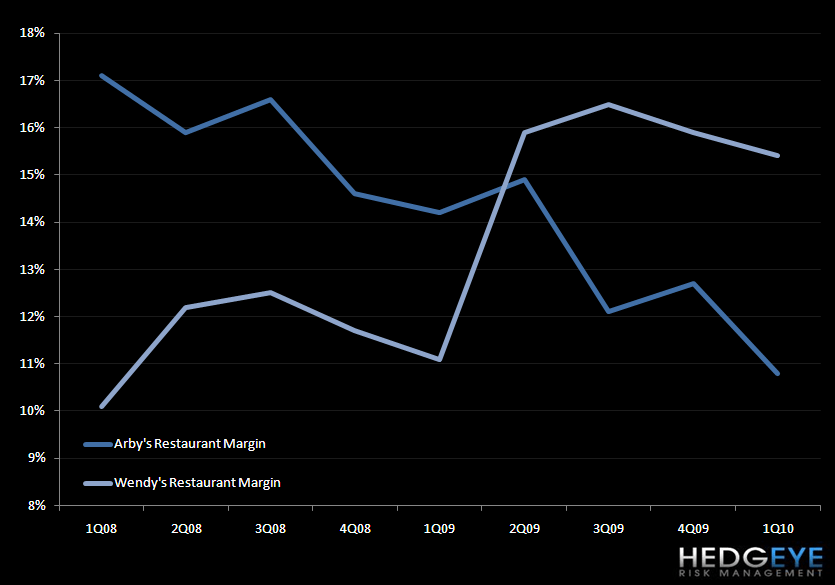

Over the past two years, management has done a commendable job restoring Wendy’s margins despite a very sluggish overall sales environment. Ironically, at the time when Trian was pressuring Wendy’s management to spin off Tim Hortons’s, Trian pointed to the higher margins at Arby’s as proof of the company’s success as operators. The relatively lower and declining margins at Wendy’s, at the time, acted as evidence of a concept that was being mismanaged.

Given the quick turnaround in restaurant-level margin trends at Wendy’s, it would seem that Trian was correct in its conclusion that the concept was being mismanaged. In the most recent quarter, the progress at the Wendy's brand was evident, but Arby's trends continued to decelerate and are overshadowing the company’s overall performance.

Arby’s restaurant margin, which closed out 2007 at an impressive 19.7%, has since declined to 10.8% in the most recent quarter, not much higher than Wendy’s reported 10.1% restaurant margin in 1Q08, just before the two companies announced the merger. The obvious conclusion would be that WEN management lost its focus on Arby’s while working to turnaround Wendy’s. That being said, it is important to remember that Arby’s performance was already suffering when it merged with Wendy's in September 2008, and the economy has exasperated the declines at the concept.

The recent sales trends are somewhat disappointing. Company-operated same store sales at Wendy's turned negative in April to -0.5% (excluding a negative fiscal month calendar shift from Mother's Day) from +0.2% in 1Q, while Arby's company-operated trends remained very negative, at -8.4%, albeit with traffic up 4% and check down about 12%.

This -8.4% and positive traffic in April marks a significant improvement from the first quarter when company-operated same-store sales declined 11.6%. Management attributed the sequentially better trends to the systemwide launch of the Arby’s $1 Value Menu in April, combined with national advertising beginning on April 11. During the weeks when the company advertised its $1 Value Menu nationally, transactions improved to +7%. And, as management correctly pointed out on its 1Q10 earnings call, “getting more customers into [its] stores is the first step in successfully turning around the Arby’s brand.”

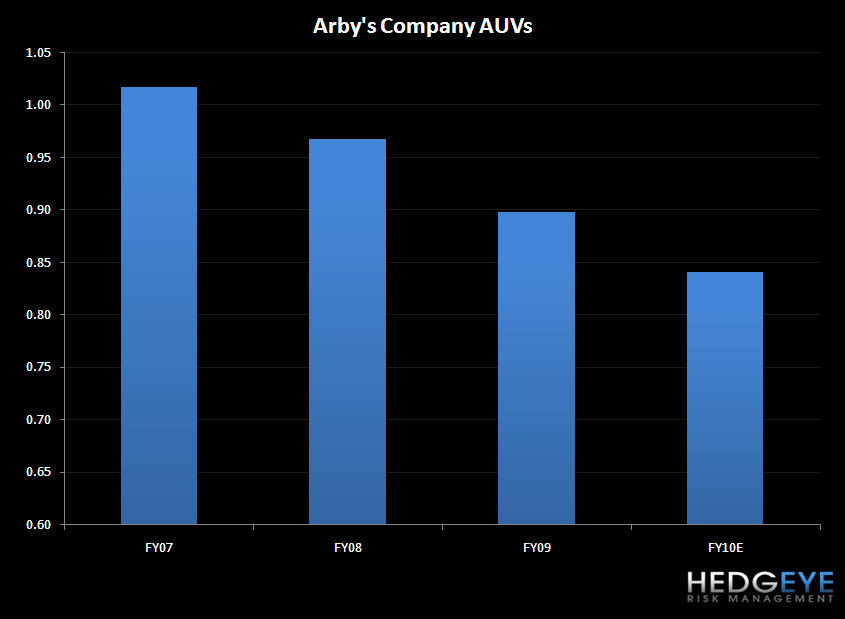

The company expects that the everyday value offering will lead to continued improvements in the second quarter as awareness grows. Investors seem less convinced as WEN is currently trading down nearly 8% since reporting 1Q10 results. Arby’s business is in free fall, relative to same-store sales, AUV and margin trends (shown below). The deteriorating trends at Arby’s are overshadowing the improvements at Wendy’s. Based on my sum of the parts analysis (also shown below), which assumes continued margin expansion at Wendy’s in FY10 (though not to the same magnitude as we saw in 2009) and continued margin erosion at Arby’s, WEN is being undervalued. In fact, at its current price, it would seem that investors are getting Arby’s for free. Given the current trends at Arby’s, this might not seem like too much of a bargain, but my numbers also suggest that WEN’s current price does not reflect the true value of the Wendy’s concept alone.

As I said earlier, Trian Partners has been extremely successful in the past creating value from mispriced securities. No, I do not think WEN will spin off Arby’s any time soon but the company will work to address the issues at Arby’s. If Arby’s shows some sign that it has at least bottomed, WEN should reflect the full value of Wendy’s, which would suggest a move higher of nearly $2. The potential longer-term upside is reliant on management’s ability to return Arby’s margins to peak levels. I don’t think this will happen in the near future but we have seen what management has been able to accomplish at Wendy’s in a short amount of time. Time will tell.

Howard Penney

Managing Director