Access Technology analyst Ami Joseph's presentation HERE and Industrials analyst Jay Van Sciver's presentation HERE.

Is your portfolio prepared for the year ahead? Are you prepared for a #LateCycle economy?

Hedgeye CEO Keith McCullough discussed our current Macro outlook and its investing implications during a free webcast. Keith was joined by our Industrials analyst Jay Van Sciver and Tech analyst Ami Joseph. The three of them discussed how an increasingly challenging Macro environment is impacting various pockets of U.S. and global equity markets.

We transcribed a small sliver of key excerpts below from this deep-dive webcast and included some critical charts.

* * * *

Keith McCullough: I’m going to walk you through our Macro process and then bring in two of my partners here – Technology analyst Ami Joseph and Industrials analyst Jay Van Sciver – who are going to help prepare you across their sectors, fully loaded with the top-down Macro view.

On slide 6, we’re showing where we’re at in what we call the Quads. The Quads are the second derivative move in growth and inflation. Quad 1 and Quad 2 are pro-growth. Wall Street is long of Quad 2 this year. They think that growth and inflation are accelerating at the same time.

They think that up until they see the latest data point which is today’s ISM, which was quintessentially Quad 3. Quad 3 is where you have inflation accelerating and real growth slowing. So you can see in the Quad chart that green dot is the Nowcast of GDP and Inflation. You can see we’re squarely in Quad 3. Quad 3 is also called economic stagflation. It’s where the cost of living goes up and consumption goes down.

This environment is not as bad as Quad 4, where the U.S. economy was last year and which we proactively prepared people for. Again that’s when both Growth and Inflation slow at the same time.

If you jump to slide 8 that’s the Quad-by-Quad breakdown of what we do in each Quad across asset classes. We’re in Quad 3, which is why we’re long Energy (XLE). That’s a new idea.

We’re long REITs (VNQ) which is not a new idea, because that’s a long in both Quad 4 and Quad 3. What I did on the pivot to Quad 3 is I started to short the Consumer and buy Energy. That’s the playbook and we’re sticking to it.

If you look at the current GDP Nowcast for the U.S. economy, it shows you that the rate of change continues to slow. What you’ve seen is that U.S. growth was accelerating all the way up into the second quarter of 2018. That’s where U.S. growth started to slow.

Now, what does that all add up to on the U.S. GDP report that is pending in January for Q4? We have a forecast that has a “0” in front of it. You can see on a headline basis our GDP estimate is right around half a percent – 0.5%. What you’ll note in this picture is that there are no other zeros. Zero is bad. And it certainly doesn’t align with others who are cheerleading the ISMs and PMIs have “bottomed” and moreover that GDP will be just fine at 2%.

So you’re going to see some investors wake up to that reality. Moreover, you’re going to see companies have to deal with the inventories associated with that reality.

In Q3 of 2018 you had a triple peak. A peak in GDP growth, inflation and profits. Now all three of those things have changed direction and inflation is the only thing that’s about to go back up.

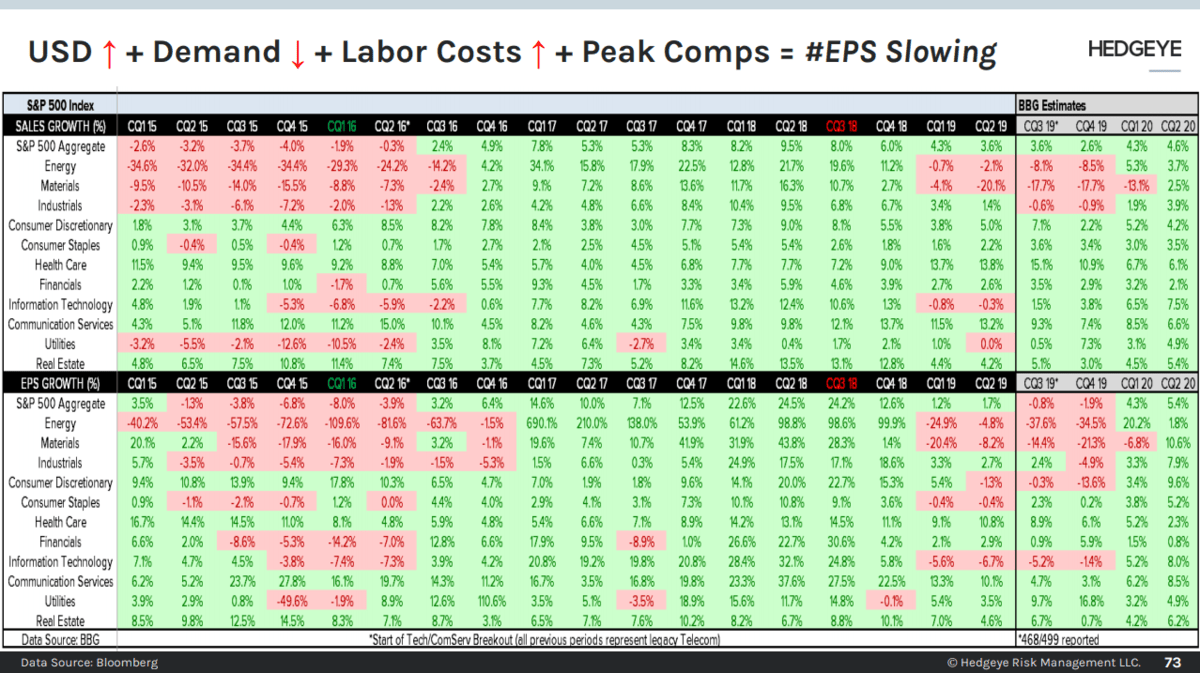

McCullough: Now before I bring in our analysts, I want to hit on Wall Street earnings expectations. The cycle peaked at 24.5% in Q2 of 2018. Then it got cut in half. And cut in half again. Then it was 1%. And now it’s “better than expected” because it was “only” -1%. But by the time we get to Q1 and Q2 of 2020 Wall Street sees a big acceleration.

No. They’re going to be slower than that in the fourth quarter and they could be slower than that in the first quarter. That’s essentially the big mismatch. So when people ask what’s the catalyst, that’s it. The stock market generally peaks in Quad 3 then goes down in Quad 4.

That’s the set-up that we have into Q2 of next year. We have two quarters of Quad 3 followed by Quad 4 coming back. Earnings continuing to go negative. We have more leverage in the system than we’ve ever seen in the history of corporate credit. I can’t imagine how that would pose a problem.

McCullough: Ami, you have some great slides on the Macro view of Tech.

Ami Joseph: Sure. I want to talk a little bit about a trend that we saw in Tech that gets to how we’re different here at Hedgeye. It’s the term “digital transformation.” Digital transformation is a hype cycle. It’s something Marc Benioff loves to talk about right now at Salesforce because that’s how he’s shoveling the manure. That’s the stuff that he’s selling.

The more he says “digital transformation,” the more I think it should be a drinking game at this point.

The truth is if you talked about “digital transformation” in 2011, 2012, 2013, 2014, 2015, you’d have been on the right side of the curve. Talking about it in 2019? It’s falling off. Now that’s not a hard and fast reason to short something but when everyone is preaching “digital transformation” and rallying around that you gotta look the other way and how fast is that really growing.

That digital transformation fueled a lot of IPOs in the last few years. What you can see in the next chart you can see IPOs through July. It’s been very rich in IPOs.

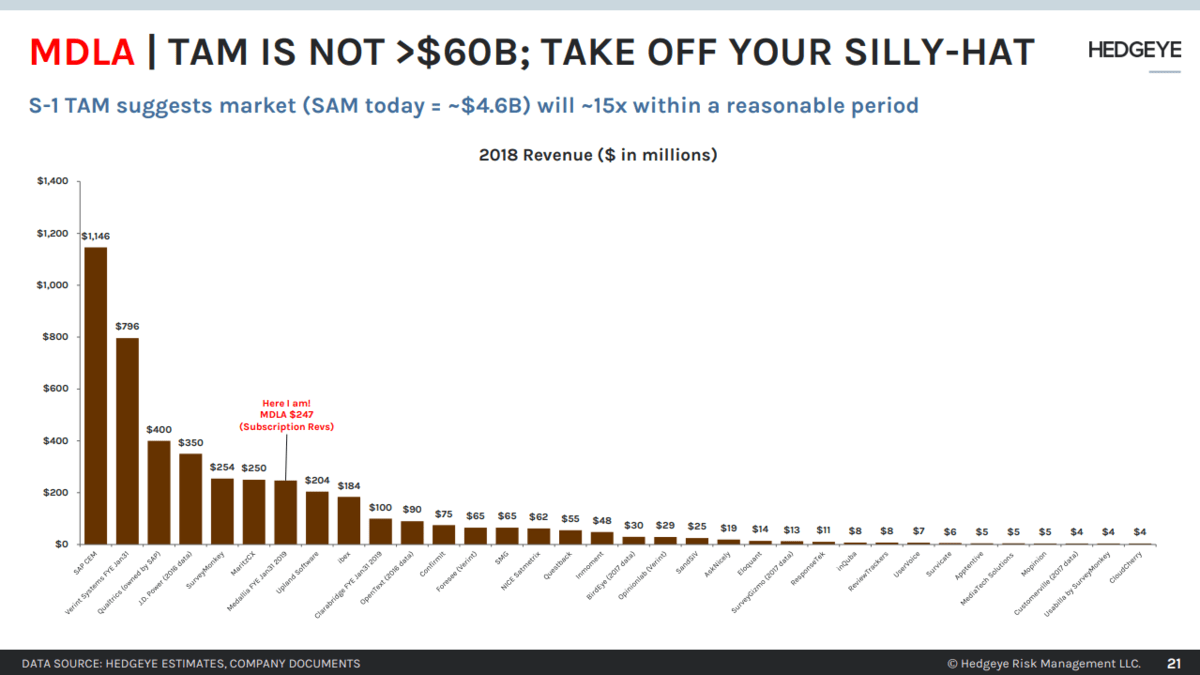

So I want to talk about Medallia, a company we went short in the Summer time. This is a good example when you think about Software companies. So the company goes public in the middle of this great software bubble. The company tells you that it has a greater than $60 billion TAM (total addressable market). I know, TAMs are silly and everybody poo-poos them.

But the rate of the silliness on the TAM is almost a tell on the shortability of the stock. This one is in the super silliness category. The entire bottoms-up tier of companies making money in the space is less than $5 billion. The company is suggesting the whole market is going to 15x in a reasonably short period of time.

McCullough: Next up is Industrials analyst Jay Van Sciver.

Jay Van Sciver: Thanks. We have the ISM report out today, which is a topical moment to be talking about Industrials because a lot of the real-time data that we track continues to slow. There was an expectation of stabilization and they are just not right. We can see this in the data. We can see this in web traffic to industrial distributors.

We see this in backlogs. This chart is really important. Backlogs are critical because that’s what factories base investment on. If you know you have six months of orders, you feel good about adding headcount, building a little extra capacity into the line. When your orders and your backlog are evaporating and you run that forward, you get a lot more tentative about your willingness to invest.

There’s a reflexive element to that where bad data tends to generate more bad data.

Van Sciver: I’ll talk a little bit about our Tesla (TSLA) short call now because people are always interested in it.

The survey on the left of this chart shows whether consumers think Tesla is a great brand relative to other brands. It’s been decreasing. You can also see the used market on the right side. Used markets often reflect what’s going on in the new car market. These are U.S. used Tesla prices coming down. We can also look at test drive activity that’s been lower. Teslas have basically been filling orders overseas.

What’s really going to define this company over the next year is what we call the first loser disadvantage. That was actually the title of our June 2017 short call on Tesla. Whether it’s the Ford Mach E or the iPace or other competitive entries into this market will have a $7,500 tax credit. Tesla will not. There are a lot of competitive entrants that will be subsidized while Tesla will not. That’s, certainly for the U.S. market which is a core market for Tesla, a significant downside catalyst for 2020.