JPM – generally a good proxy for consensus – issued pretty aggressive estimates and price target.

The sell side seems to have jumped on the momentum bandwagon lately. Maybe it’s me – they may have always been mo – but with the huge run up in many gaming/lodging/leisure stocks, it seems that price targets are being raised by alarming magnitudes and with assumptions that stretch the bounds of rationality.

My friend over at JPM recently raised his price target almost 20% to $64 or 40%+ higher than the current price. The analyst uses a sum-of-the-parts derivation to reach that price target. Anna and I (mostly Anna) will tear those assumptions apart in a later post. In this post, we are taking a look at just the estimates.

The chart below show’s JPM’s EBITDA and RevPAR estimates. RevPAR is projected to grow 7%, 8%, and 8% in 2010, 2011, and 2012, respectively.

Pretty aggressive in our opinion and not surprising based on the prior recovery in 2004-2007. Indeed, in looking at the next chart, one can see that it took 5 years to recover to peak RevPAR. Using JPM’s own growth estimates implies a 5 year recovery period to 2012 to regain peak RevPAR.

We have several issues with the 5 yr return to peak assumption:

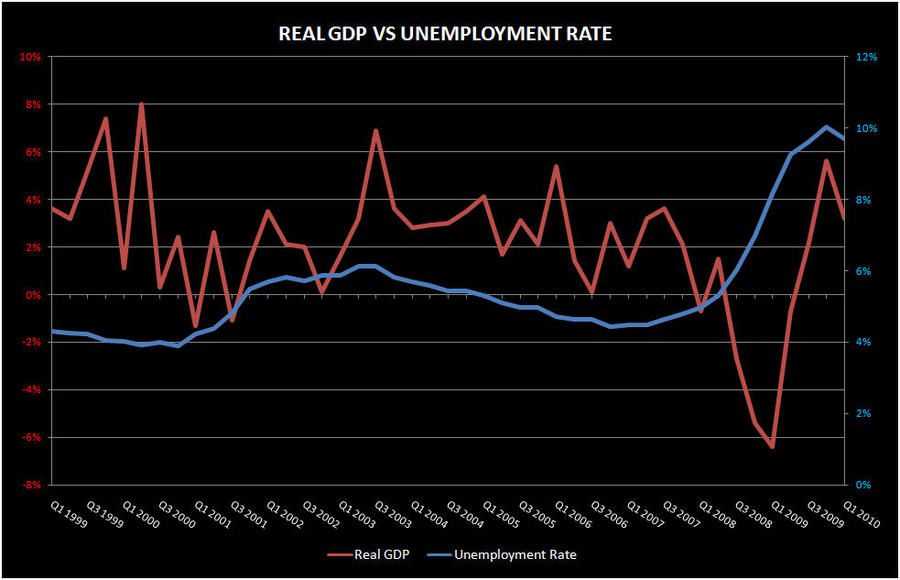

- Unemployment – In a recent note, we showed the growing decoupling between GDP and RevPAR in favor of a tighter relationship with Unemployment. We suspect that the decoupling began to take place as government spending as a percent of GDP exploded beginning in 2008. The problem is that unemployment has not moderated on the same path as it has in previous recoveries and certainly not in the last one. Note in the chart below that unemployment peaked at 6% during the last cycle and improved quickly.

- Housing – We’ve shown that accelerating housing prices were a big component of the explosion in consumer spending from 1. Even during the last recession, housing prices held and provided a buffer to the downturn. The latest downturn was caused by the housing bubble burst, and we remain pessimistic regarding a v-shaped housing recovery.

- Pent-up demand – We did not expect RevPAR to turn as quickly as it did but we cannot help but think that a significant part of it is just pent-up demand. We’ll see over the coming months.

- Sovereign debt issues – Our Macro team remains negative surrounding the impact of all of the sovereign debt issues – including our own – on interest rates and the global economy. Neither would be good for hotel demand.

For these reasons, a recovery similar to 2004-2007 is unlikely, in our opinion. Unfortunately, it appears investors are banking on it.