Position: Long Germany (EWG); Short France (EWQ)

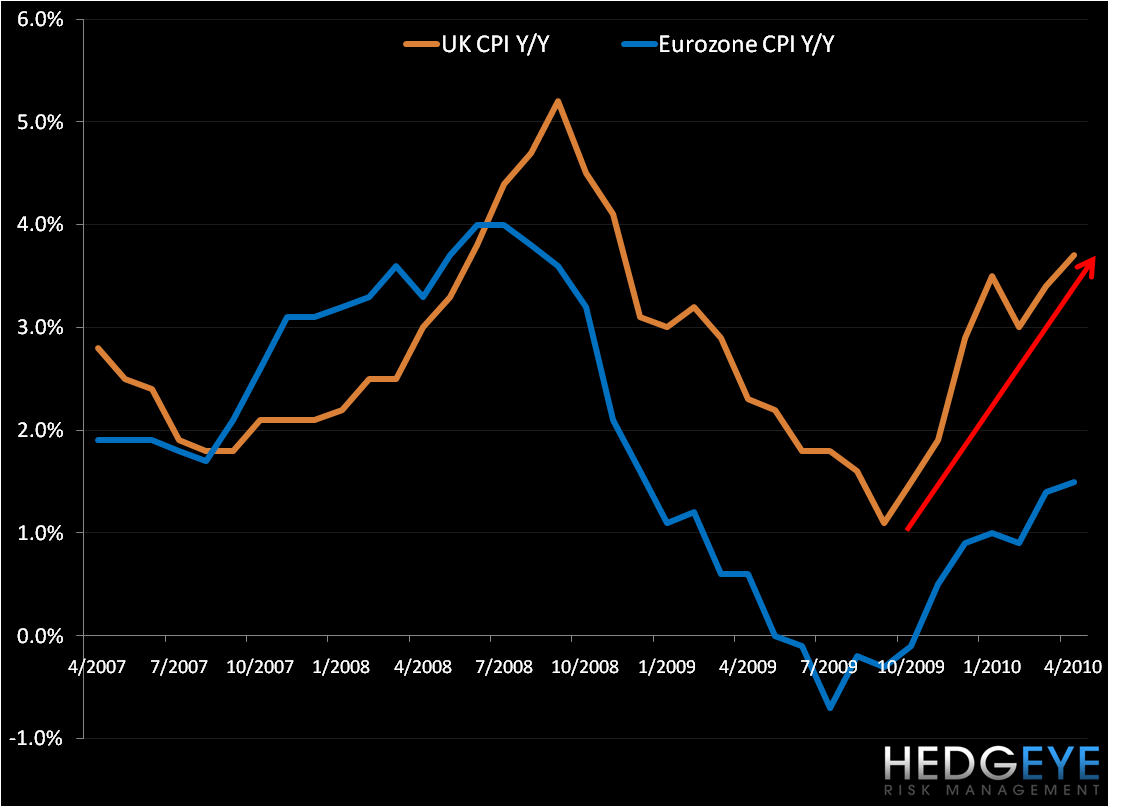

We’ve been on the tape warning of mounting inflation pressures in the UK. Earlier in the month the UK Producer Price Index for April measured +13.1% on an annual basis. Today, the UK Consumer Price Index for April registered +3.7% year-over-year, up from March’s rise of 3.4%.

For context, we’ve charted UK CPI versus Eurozone CPI below. Within the Eurozone (16), only Greece (at +4.7%) has a higher inflation rate than the UK; and among the EU states (27), only Romania and Hungary (in addition to Greece) have higher inflation rates than the UK, at 4.2% and 5.7% respectively.

Although inflation has surpassed the top-side limit of 3% set by the Bank of England for the last two months, Governor Mervyn King downplayed the rate as “temporary” in a statement today, citing “substantial spare capacity.” We’ll take the other side of the trade, namely that rising inflation is not just a near-term issue in the UK. As Keith has noted in his work, “US sovereign debt problems are only different than Western European ones in one key factor – timing. The darkest days for professional US politicians who perpetuate a fiat currency policy are coming.” Alongside the US, we’d add the UK to our theme of Duration Mismatch. Stay tuned.

Matthew Hedrick

Analyst