Below is a chart and brief excerpt from today's Early Look written by Hedgeye CEO Keith McCullough.

|

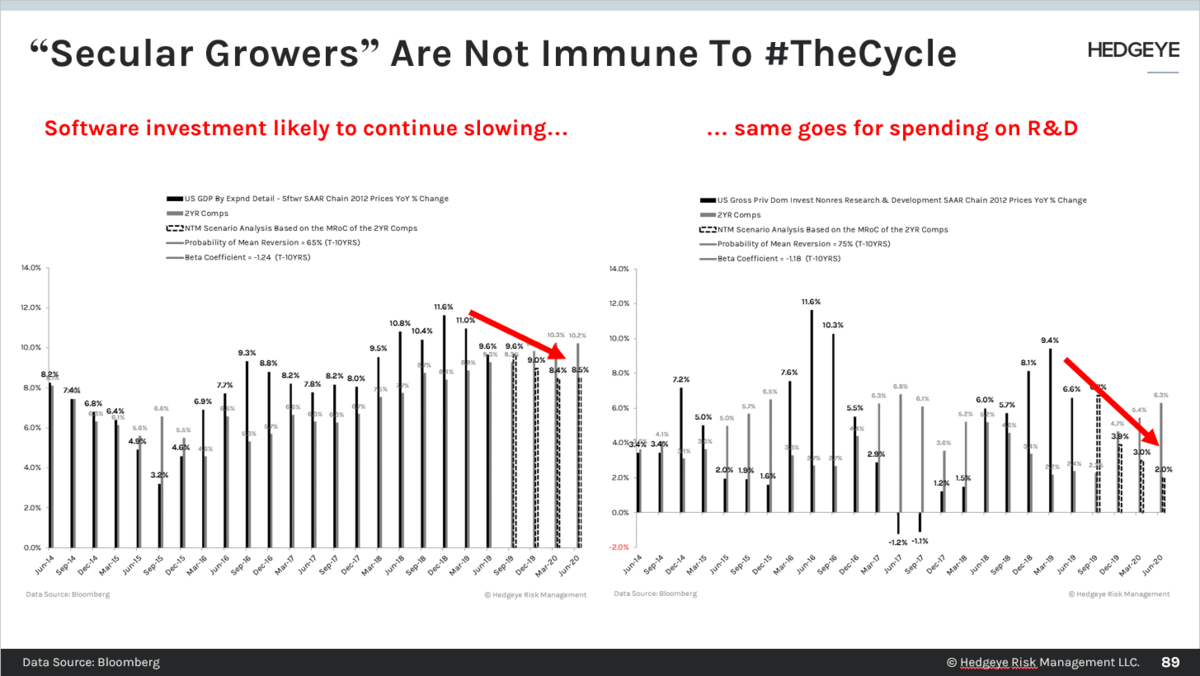

Why is it that self-perceived experts of “Secular Growers” struggle so much with The Cycle? At least we ROC (rate change) heads who start with the macro know we don’t know what we don’t know! Top-down, what we know about the US economic cycle as of yesterday is as follows: A) US Durable Goods #slowed to a new cycle low of -5.4% year-over-year In other words, it was definitively #Quad4 in Q3… and there’s a high and rising probability that no matter what #BeanDeal America gets, both aggregate and US Tech/Software Capex will continue to slow throughout Q4 of 2019. |