JACK is one of the better-run restaurant companies; unfortunately, the concept is in a “box.” It’s a QSR company serving food to consumers who are unemployed in a part of the country that has significant economic challenges. For reference, management highlighted today that 44% of its Jack in the Box restaurants are located in the 10 states with the highest levels of unemployment. In addition, a mere 2% of stores are in the 10 states with the lowest levels of unemployment.

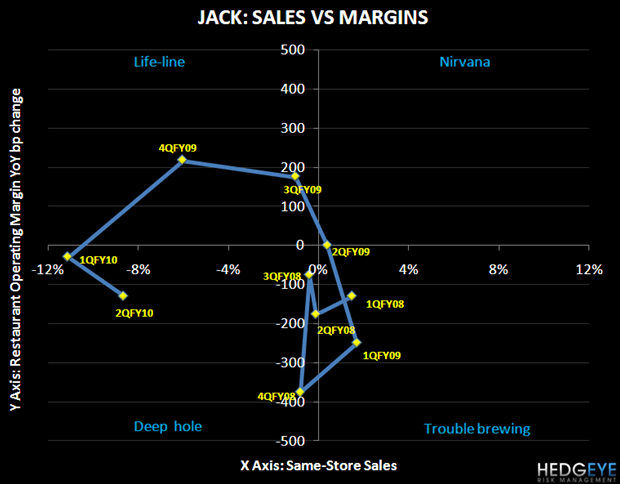

Looking at the chart below, the company was operating in what we call the “life-line.” In this quadrant margins are defying gravity because they are continuing to rise while same-store sales are declining. These trends are not sustainable, as evidenced by the company’s performance in fiscal 1Q10 and 2Q10. During the second quarter, the company moved further into the “deep hole.” The outlook for top line trends remaining negative (though at a lesser rate as we trend through the year) and since there is no reason to get excited about commodity costs, JACK will likely remain in this deep hole. From where I sit, the likelihood of JACK climbing out of this hole in the next 6 months is slim.

Management stated today that commodity costs are expected to increase by approximately 2% in 3Q10 and 3% 4Q10. The increase is being driven by higher beef costs; the increase in beef costs will be partially offset by lower chicken and bakery costs. The company benefited from lower YOY commodity costs in the first half of the year (down about 7% in 1Q10 and -1% in 2Q10). Even if same-store sales begin to improve sequentially, higher commodity costs will put increased pressure on margins.

Management’s fiscal 3Q10 same-store sales guidance of -7% to -9% at Jack in the Box, however, does not point to a sequential improvement in 2-year average trends, but instead, implies trends that are flat to -90 bps. Given that same-store sales are not expected to improve materially, commodity costs are moving higher and the company is lapping its most difficult restaurant-level margin comparison from FY09 in 3Q10, we could see JACK move deeper into the deep hole before it improves.

For those looking to buy a contrarian name, buying a stock in the hole is the place to be. That being said, I’m going to let at least another quarter pass by until I have some visibility on the company’s ability to move up and to right in the chart below.

EARNINGS CALL NOTES:

- Quarter in line with expectations

- Lower gains from refranchising

- Transaction closed in 3Q instead of 2Q

Jack in the Box

- SSS: -8.6%

- In line with guidance

- Sequential improvement in TC and check

- Some improvement in CA and TX, but no improving fundamentals until unemployment begins to improve

- 44% of stores are in the 10 states with highest unemployment, 2% in 10 states with lowest

- Best way to drive traffic is to target advertising to focus on value and premium

- Continued to reinforce position with premium brand with varied and innovative brand

- Grilled sandwiches, promotions have drawn good response and high attach rate

- Higher quality French fry – shorter cook and longer hold time

- Some margin family promotions allow guest to mix and match small items

- Added smoothie and ice cream shake flavors

Qdoba

- SSS: +3.1%

- Higher consumer confidence and spending patterns among fast casual

- Effective advertising campaigns

- Continued improvement in guest satisfaction score

On track with growth plans for both concepts including expanding Jack in the Box into new markets

- Opened restaurant in Tulsa and Oklahoma City

- Sales volumes at new markets exceed market average

- Focused on reducing cost structure while positioning the brand

Financials

- EPS was $0.32 vs $0.51 last year

- Refranchising gains were $0.15 lower than last year due to the 3Q close of the transaction which has generated $0.10 per share

- JACK provided no financing for refranchising

The rest of the P&L was in line with expectations

- Food and packaging improved 70 bps

- YoY commodities were ~1% lower in the quarter

- Beef costs favorable in the quarter despite rising beef costs

- Labor up only 20 bps despite the 8.6% decline in SSS

- Lower turnover also helping

- Franchise margins were lower due to franchise sales deleverage

- 8.8m has been cut out YTD from SG&A

- Roughly half of the $3.7 million decrease in advertising costs in the quarter and $9.2 million year-to-date was due to franchising

- Important to maintain advertising weighting

- $5-6m dollars incremental spending for 3Q and 4Q, reflected in guidance

Other costs

- Facility costs declined and might fluctuate by quarter

- Expect non-cash charges to be higher in the back half of the year due to timing of the reimaging schedule (also reflected in SG&A guidance)

- Repurchased 2.6m shares of stock at ~$19 YTD and have approximately $47m in buy backs under credit facility and authorized by board

- Repaid 21m under term loan

Distribution sales

- Up 35% in quarter vs last year, 14% increase in 1Q

- Driven by refranchised stores and more franchise locations now being supplied by company distribution centers

Commodity costs

- Expected to increased by ~2% in 3Q and 3% in 4Q

- Driven by higher beef costs (20% of spend)

- Full year beef costs expected to be flat

- 0% of our import 90s covered through May at $1.44 per pound versus current market prices in the $1.75 to $1.78 per pound range

- Lower chicken and bakery costs (combined also account for ~20% of spend)

- Lower by 6% for balance of year

Guidance for 2010

- 3Q SSS for Jack in the Box should be -7% to -9%

- Full year -6.5% to -8.5%

- 3Q SSS for Qdoba should be +2% to +4%

- Full year +1% to +3%

- EPS range is unchanged at $1.85 to $2.05

Involved in bankruptcy of a former franchisee

- 70 restaurants involved

- One restaurant acquired by the company

- Three closed

- The rest are being transferred

Q&A

Q: Is competitive discounting easing?

A: Chili’s bringing back their 3 for $20 deal so we are seeing a lot of couponing. Heavier discounting in CA. BKC has come off the $1 double cheeseburger but the buck double is there. Perhaps it is a little less competitive than a couple of quarters ago. Breakfast was JACK’s best performing day part despite MCD.

Maintained media weight in 1Q and 2Q. Will continue with marketing strategy in three areas; premium products, value messaging (bundled meals), breakfast.

Q: 10 cent addition from 21 unit sale in Q3?

A: The $0.15 is referring to the delta from last year’s 2Q. The $0.10 per share is from the deal closing in the third quarter that we had anticipated for 3Q.

Q: How satisfied are you with the balance of value across the menu with current premium given sales mix?

A: We are seeing some good results from bundled meals. Have to provide value, without hurting margins or brand.

Q: MCD mentioned that commodity pressure won’t cause them to raise prices, how do you guys cope with that?

A: We’ll be working with consultants to see if there is an opportunity to take price.

Q: Beef prices have spiked…how many days or weeks can you be out of the market (B 50’s) before you have to succumb to higher prices.

A: The 50s are fresh so not as much flexibility as with the 90s.

50’s expectations are at plus or minus $1/lb.

Q: Insurance settlement…how much was that in G&A, as a benefit in 3Q last year.

A: Not sure.

Q: On the last call you said CA was outperforming other markets?

A: TX is a more challenged market, CA is outperforming them. Young, Hispanic males are suffering.

Q: When do the TX comparable store sales normalize with the ?

A: Texas was positive up until Q4 of last year.

Q: Premium versus value…how do you measure whether or not you are spread too thin…

A: The incremental spend is coming from company, not franchisees. We do a promotion and then analyze the sales, traffic, and margin impact.

We have done several different scenarios and we believe that over time, weight can go behind both messages effectively.

Q: Restaurant reimage program, how much more time until that’s fully completed.

A: 50% on full remodels. All exteriors are done. We’ve said that the remodels locations’ sales are holding up better than the ones that were not reimaged.

Q: Hand-wringing over higher beef prices…but you contract well and I’m just curious about the 3Q and 4Q guidance…how much of the higher margin commodities can you offset with mix?

A: we have done a good job of putting together promotions that are margin friendly and have a lower food cost.

Q: G&A guidance as a % of revenue, including distribution sales…can you give us a range on an absolute basis?

A: Not giving it to you today but we’ll consider it going forward.

Q: Despite MCD $ menu at breakfast, you saw strength at breakfast time. How were breakfast products mixing across the whole day? Did you get trade down from lunch or dinner products during the day that pushed check down?

A: Generally we don’t see breakfast sales in large volumes past noon…

Q: Long term averages for refranchising program. How should we be thinking about averages for the last three years of the program.

A: Proceeds will average about 450 this year and average gains of about 325 based upon the midpoint again.

30 restaurants we sold in 2Q. Visibility of one additional larger deal in 3Q or 4Q that will also have lower than average proceeds and gains.

Q: Refranchising in Q2 and 3Q, was there a geographic concentration?

A: Yes, the deals that closed in 2Q were in Pacific Northwest. Early 3Q deal was in central California.

Q: Bad weather? Can you quantify the impact?

A: Don’t like to use it and we lap it next year.

Q: Improving environment for refranchising process…should we think about refranchising rate accelerating?

A: expectations of being 70% to 80% refranchised by the end of 2013 gets you there. Not anticipating anything faster than that.

Q: Use of cash?

A: Authorization for share repurchased expires in November of this year. Besides that we’re going to reinvest and pay down debt only as much is required.

Q: Thoughts on market trends? Are you going to wait and then contract?

A: If we could extend current coverage we would do so. We are monitoring it daily. Current guidance is that we would have no coverage going past May.

Q: On marketing, 1H10 you were able to maintain the media weights?

A: We did maintained the media rates and did some shifting from national to local.

Q: On beef, the 50’s are at $1.15 right now…does it have to come down quite a bit for your guidance to hang together?

A: We are expecting around $1 for the entire year.

Q: Why 5-6m more on marketing?

A: Because of the sales situation

Q: Chicken plus baked items are down and count for as much as beef does…what are you seeing in soft drink prices and dairy?

A: Cheese and pork are around 5% each. They will be up in the double digits. On the downside, a down-low-double-digits number in potatoes, beverages flat. That’s how we get comfortable with the increase in 3Q and 4Q.

Q: After B90’s coverage expires, what does your guidance assume?

A &1.75-$1.78

Q: Confidence in hitting ROP margins between 15% and 16% with commodity outlook and comps looking as they are, should we be looking at the low end, towards 15%?

A: We’re right at the mid point of our range in EPS. But if we end up hitting $1.85 we would be at 15%, anything north of $2 is more like 16%. We did 15.2% this quarter on a down 8.6% comp.

Howard Penney

Managing Director