“Any intelligent fool can make things bigger, more complex, and more violent. It takes a touch of genius - and a lot of courage - to move in the opposite direction.”

-Albert Einstein

At this stage of the Sovereign Debt Dichotomy, it’s fascinating to observe how little professional politicians know about what they don’t know. From Athens to Albany, finding resolve in Piling Debt Upon Debt Upon Debt via fiat currencies is not going to end well. Anyone who isn’t paid to be willfully blind gets this by now.

With Ben Bernanke and Jean-Claude Trichet printing moneys from the Keynesian heavens, we thought we’d do some minting of our own this morning and introduce Fiat Fools as our new Hedgeye nickname for politicians running European and American monetary policy.

Adam Smith be damned - there is nothing invisible about the heavy hands of these governments. When it comes to their latest storytelling of a “fat finger” causing volatility in the US stock market, take their word for it. It’s a big fat middle finger from the creditors of our broken promises.

In Latin, the word fiat means “let it be done” … and so our modern day Roman Gods of finance will do exactly that. Let us debauch the value of our currencies and inflate our way out of this colossal mess. All the while, let us hope that our creditors and citizens alike don’t notice Main Street inflation while Wall Street gets paid to underwrite it.

Alas, we all know that hope, unfortunately, is not an investment process for anyone other than the Fiat Fools. The inconvenient truth of history reveals that debtor nations who become hostage to foreign lenders are just that – hostages. As David Walker points out in his latest book “Comeback America”, “the British Empire learned this in 1956, when Britain and France were contesting control of the Suez Canal with Egypt.” All US President Eisenhower needed to do was threaten to sell the British Pound.

What if the Chinese or Japanese imposed that credible threat on the US? Up until Greenspan went global with the Fiat Fool system of US economic policy, US public debt held by foreigners was less than 20%. Now it’s pushing north of 50%, and that’s the point. The Buck stops there - and don’t think for a New York minute that America isn’t setting herself up on the trolley tracks to get run right over by the same oncoming train that European pigs have.

This is why we call it the Sovereign Debt Dichotomy. There is simply a Duration Mismatch between when the Fiat Fools of Europe and America will see their debts come due. There is absolutely no irony that Greece started to unwind before Spain did. Nor will there be as Spain starts to unwind before France and the US do. The timing of debt maturities matters. Only a Fiat Fool who has never traded a market in his life couldn’t tell you that.

As our head of US Strategy, Howard Penney, recently wrote, America has to roll over 40% of US Treasury debt by 2012. Even compared to a country like the UK that has already been forced to devalue its fiat currency, that’s more than a double versus UK gilt maturities as a percentage of the total outstanding!

Altogether, this is the #1 reason why we have sold into US stock market strength this week. The duration gap is finally starting to narrow between the Fiat Fools of Europe having their pants pulled down in front of the world and the tide rolling out on our professional US politicians.

This morning the Euro is making another lower-low, and remains broken across all 3 of our investment durations (TRADE, TREND, and TAIL). As a result, since 58% of the US Dollar Index is Euros, the Buck Breakout that we have been calling for since the beginning of 2010 continues as the US Dollar hits higher-highs.

At a point, and we are not there just yet, the US Dollar is going to be a raging short again. There is a reason why we called for the Burning Buck last year. That reason hasn’t gone away. The European Fiat Fingers are simply taking their turn at the wheel. Unless Ben Bernanke stops behaving like Arthur Burns did between 1, and gets this US currency and the sovereign debt that underpins it under control, we are going to go to a very scary societal place.

From a risk management perspective, the US Dollar Index looks like a short again up at the $86.97 level. As both the US Dollar and gold push to higher-highs as a refuge away from a Euro that continues to make lower-lows, I don’t see why we don’t test that upward boundary. The Buck Breakout will continue until the Euro finally becomes the most consensus trade in modern day Rome.

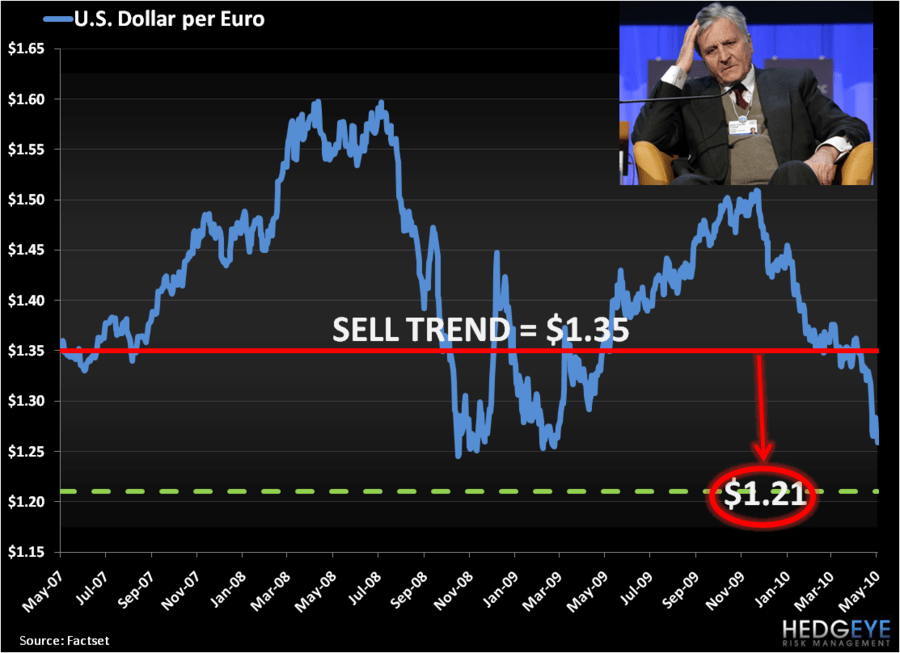

Our immediate term TRADE range for the Euro is now $1.24-1.28 and until Spain has its Greek moments in June/July, I’d stay with the Euro short bias as the most obvious way to be short the decision making process of the Fiat Fools. In terms of the capitulation zone, I am now looking at an ultimate 2010 bottom for the Euro at $1.21. That quantitative risk management view lines up pretty well with where I see the US Dollar Index finding its final crescendo.

Politics may indeed be local. Fiat Fools, unfortunately, have gone global.

My immediate term support and resistance lines for the SP500 are now 1144 and 1186, respectively.

Best of luck out there today,

KM