R3: REQUIRED RETAIL READING

May 12, 2010

TODAY’S CALL OUT

Macy’s reported 1Q earnings this morning of $0.05, a penny ahead of recently revised guidance and in-line with the Street. After hosting an analyst day two weeks ago and reporting April same-store sales late last week, there are few surprises with today’s release. As is always the case with Macy’s the conference call tends to add a bit of color to the quarter, but there are a couple of highlights worth noting at first glance:

- Guidance remains unchanged (albeit recently revised upward) for the year at $1.75 to $1.80, driven by a 3-3.5% same store sales increase. Management says “it is premature to raise annual guidance further at this time given the macro-economic uncertainty.” With same store sales coming in at 5.5% in the recently reported quarter, the current comparisons for 2Q almost identical to 1Q, and demand through early May remaining solid, this seems like an overly conservative statement to make. With that said, the Street is at $1.87 and with so much riding on 4Q profits we expect conservative posturing to continue.

- E-commerce appears to be building as a key contributor to the business, finally. Sales from Macys.com and Bloomingdales.com increased by 34% in the quarter, contributing 90 basis points to the overall same store-store sales result. This outperformance is amongst the stronger online results we’ve seen from traditional retailers.

- Inventories remain in very good shape, down 7% year over year. With total sales up 7%, the 14% sales/inventory spread is noteworthy and sequentially improved from 4Q.

- Management mentions the success of the quarter is in part due to the company’s My Macy’s strategic initiatives. While these internal efforts have been underway for a couple of years, it’s hard not to notice the company’s success coinciding with 1) the overall pick up across the mall and 2) similar margin and sales performances out of other department store operators.

Eric Levine

Director

LEVINE’S LOW DOWN

- With clogs back on the runway and toning shoes all the rage, it was only a matter of time before the two products became one. Enter the “Fitflop Gogh”, a clog built around the company’s Microwobbleboard technology. Keep an eye out for the patent leather, metal studded version slated to pop in NYC boutiques in a matter of weeks.

- In a yet another sign that the off-price channel is seeing less quantity of “quality” brand name goods, Fossil pointed out that its sales to the off-price channel were down 50% in its first quarter to about $5 million. Management also noted that the run rate for off-price sales from Q408 to Q209 was about $10 million per quarter. Clearly tight inventory and growing demand is helping to dramatically reduce FOSL’s reliance on off-price.

- With a deal announced between Zale and Golden Gate Capital, it appears the company has bought some time (and raised some capital) to execute another iteration of a turnaround strategy. While the details of the merchandising and marketing plan were not discussed, it was clear from management comments that Zale’s store base is not expected to shrink from here. In fact, the interim CEO made it a point to say with the current assets acting as a base, the goal is to grow the business from here. Easier said than done, but time now appears to be on ZLC’s side.

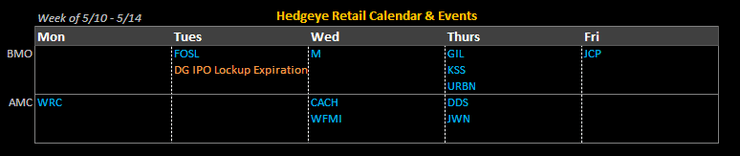

HEDGEYE CALENDAR

MORNING NEWS

GSI Acquires E-Commerce Supply Chain Solutions - GSI Commerce Inc. has acquired VendorNet, a Boynton Beach, Fla.-based multichannel e-commerce supply chain solutions provider to more than 100 retailers and brand marketers. <sportsonesource.com>

Macy's May Offer Exclusive New Clothing Line from Hugo Boss in Fall 2011 - Sources say Macy's is in talks to sell "White Label," which will be a range for men and women priced below most Hugo Boss offerings, the NY Post reports. The mid-priced line is part of Hugo Boss CEO Claus-Dietrich Lahrs's plan to double US revenues. <streetaccount.com>

Macy's Launches Web Site Geared Towards Travelers - The site includes a hotel search and booking engine powered by Kiwi Collection. <internetretailer.com>

International Spend in UK Hit by Flight Ban in April - International shopper spend in the UK fell 16% year-on-year in April as the volcanic ash cloud impacted tourism. <drapersonline.com>

Furniture Buying Index Up 6th Month in a Row - The Furniture Buying Index, tracked by America's Research Group, jumped two points this month to a reading of 71, marking the sixth consecutive month the Index has moved up. “Pent-up demand and larger than expected tax refunds helped drive the Index up two points this month,” said Britt Beemer, chairman of America’s Research Group. “When the Index reaches 70 points or higher, the success of retail furniture sales goes up dramatically. “This is a good sign especially considering that Memorial Day weekend is historically a very strong furniture weekend.” <hfbusiness.com>

K-Swiss Boosts Marketing Efforts with Another Athlete - KSWS signed a multiyear deal with France’s second highest ranked tennis player Gael Monfils to represent both footwear and apparel. The 23-year-old tennis phenom, currently ranks at No. 18 in the ATP World Tour and will be the highest ranked player on the K-Swiss team, which also includes tennis players Bob and Mike Bryan and Sam Querrey. Monfils has two career ATP titles and is a seven-time ATP Tour finalist. “He will be a big part of our marketing efforts, not only in Europe, but globally as well,” K-Swiss sports marketing director Erik Vervloet said in a statement. “He is young, talented, and is only going to get better as the years go on.” <wwd.com/footwear-news>

Red Wing Shoe Co Receives Grant to Expand Facilities - Red Wing Shoe Co., the owner of Vasque, Irish Setter Boots, and other shoe brands, has received a $261,270 grant to expand its plant in Potosi, MO, and add 42 new full-time jobs within two years, according to the St. Louis Business Journal. <sportsonesource.com>

Li Ning Tripling Store Size - Chinese sportswear company Li Ning Co. Ltd. is tripling the size of its Pearl District store. The store opened only three months ago. <sportsonesource.com>

Hot Topic Launches Helmetgirls Tees - Urban pop-art artist Camilla d'Errico has paired with Hot Topic to launch a line of T-shirts featuring Helmetgirls designs. The tees by licensee All Pacific Apparel are rolling out to Hot Topic stores now in the U.S. and online. D'Errico's manga-inspired artwork has been on snowboards, magazine covers, toys, clothes and accessories. <licensemag.com>

Yoox Profits Triple in Q1 - Profits at online retailer Yoox Group quintupled in the first quarter, jumping to 2 mm euros. Increase due to currency hedging and lower interest expenses having self-financed most of its investments on the back of its initial public listing last fall. Revenues gained 43.4%, reaching 50.3 mm euros. The 10-year-old company also runs e-commerce sites for designer brands from Marni and Emilio Pucci to Emporio Armani, Valentino and Roberto Cavalli. This division reported a 109% increase in sales. At the end of March, Yoox counted 20 online stores, eight more than in March 2009. In the first quarter, Yoox launched online stores for Coccinelle, Giuseppe Zanotti, Napapijri and Alberta Ferretti. In February, the firm extended its collaboration with Giorgio Armani SpA in Europe, the U.S. and Japan until Jan. 31, 2015. Under the new agreement, the Armani Jeans brand also will be included on emporioarmani.com. Geographically, sales in Italy grew 21.1% and 38.7% in Europe. Revenues in North America rose 111.6%. <wwd.com/business-news>

Maidenform Brands Inc. Doubles Profits - Strength due in part to strong gains in its shapewear business. The firm also raised its guidance above Wall Street’s estimates. Sales rose 25.1%: Wholesale sales increased 27.4%, Retail sales rose 3.7%. Top- and bottom-line results exceeded analysts’ expectations. Leaner inventories and reduced promotional activity drove the firm’s gross margin up 430 bps. Shapewear sales, up 34%, were key to the quarter’s performance. “Shapewear now makes up more than a third of Maidenform’s global business and is the fastest-growing category in intimate apparel,” said CEO Maurice Reznik. <wwd.com/business-news>

R.G. Barry Quadruples Profits - Higher sales and margins helped R.G. Barry Corp. more than quadruple its third-quarter profit. The marketer of slippers and accessories footwear, recorded 5.1% sales growth and 690 bps gross margin expansion. “Our spring business benefited from the growth initiatives undertaken during the past several years and is being measured against our very healthy results from the equivalent period last year,” said Greg Tunney, president and CEO, in a statement. <wwd.com/footwear-news>