Less SNAP is Good

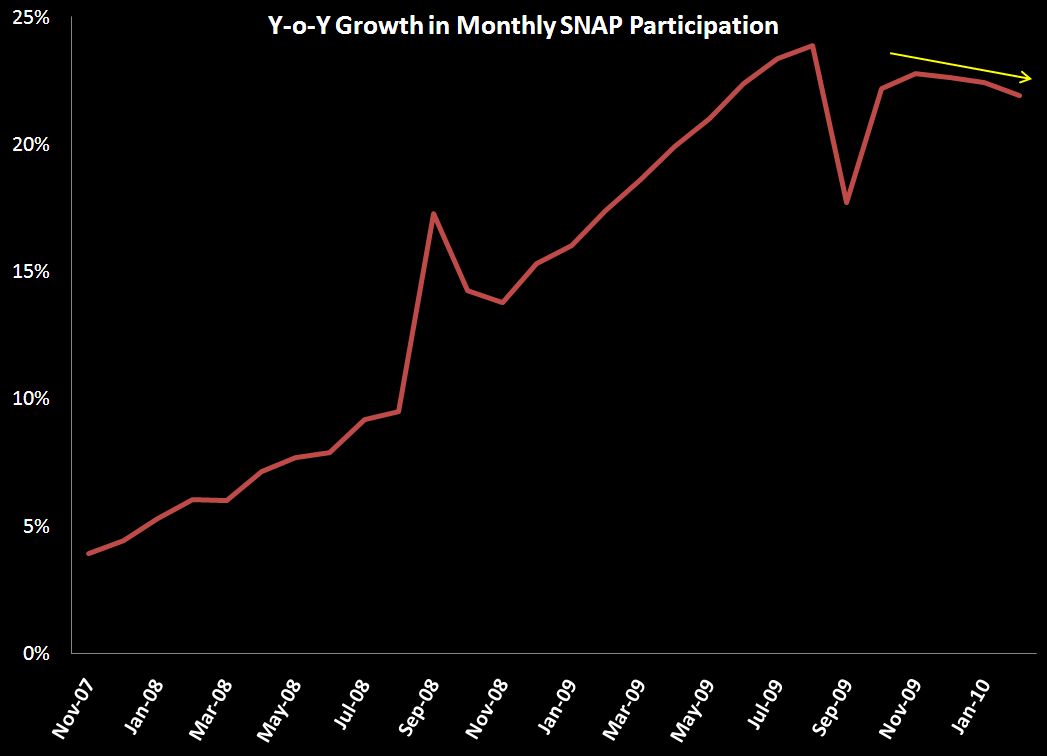

Another month of SNAP (formerly known as the Food Stamp Program) data is in, and for the third month in a row the rate of change in participation has slowed. This is hardly a victory for the American consumer or the country in general, given the absolute levels of those currently receiving benefits is still high by any measure. As of February, there are 39.7 million people on SNAP representing 18.3 million households. The USDA predicts 43 million people could be on the program by September of 2011. Let’s hope their forecasting is as “challenged” as the rest of the government.

On the plus side, we are beginning to finally see an erosion in the growth of those lining up for the government subsidy. Is this the end of the dollar stores and deep discounters as we know them? Probably not, but what has been a clear tailwind is beginning to finally subside as it pertains to low income food purchase subsidization. Unfortunately the latest data point is still two months behind, but it is now becoming clearer that the growth in those falling into the lowest income brackets (as defined by need for SNAP) is beginning to slow. Marginally good news overall for those concerned about the state of the US consumer and slightly negative news for those businesses benefitting from those needing monetary assistance to feed their families.

Eric Levine

Director