This commentary was written by Dr. Daniel Thornton of D.L. Thornton Economics.

In 2016 I wrote an essay pointing out that economic growth has been trending down since the late 1940s. Some economists have suggested the economic growth could be brought up to the post-war average of about 3%, but I argued this would be very difficult. In the 13 quarters since I wrote that essay, economic growth has average 2.5% compared with 2.3% during the prior 13 quarters.

In 2017 marginal tax rates were lowered for every income level and the corporate tax rate was reduced from 35% to 21%. These and other changes in the tax code were supposed to stimulate economic growth. The federal debt has increased by more than $1.5 trillion over this period.

According to many economists, the increase in federal spending should have produced a marked increase in output. Not surprisingly, it didn’t. Output growth has averaged 2.5% since 2018Q1 and is expected to grow at that or slower rate for the next couple of years—much slower if there’s a recession. This essay shows the trend in output growth, provides several reasons why output growth has trended down, and discusses if and how the trend can be reversed.

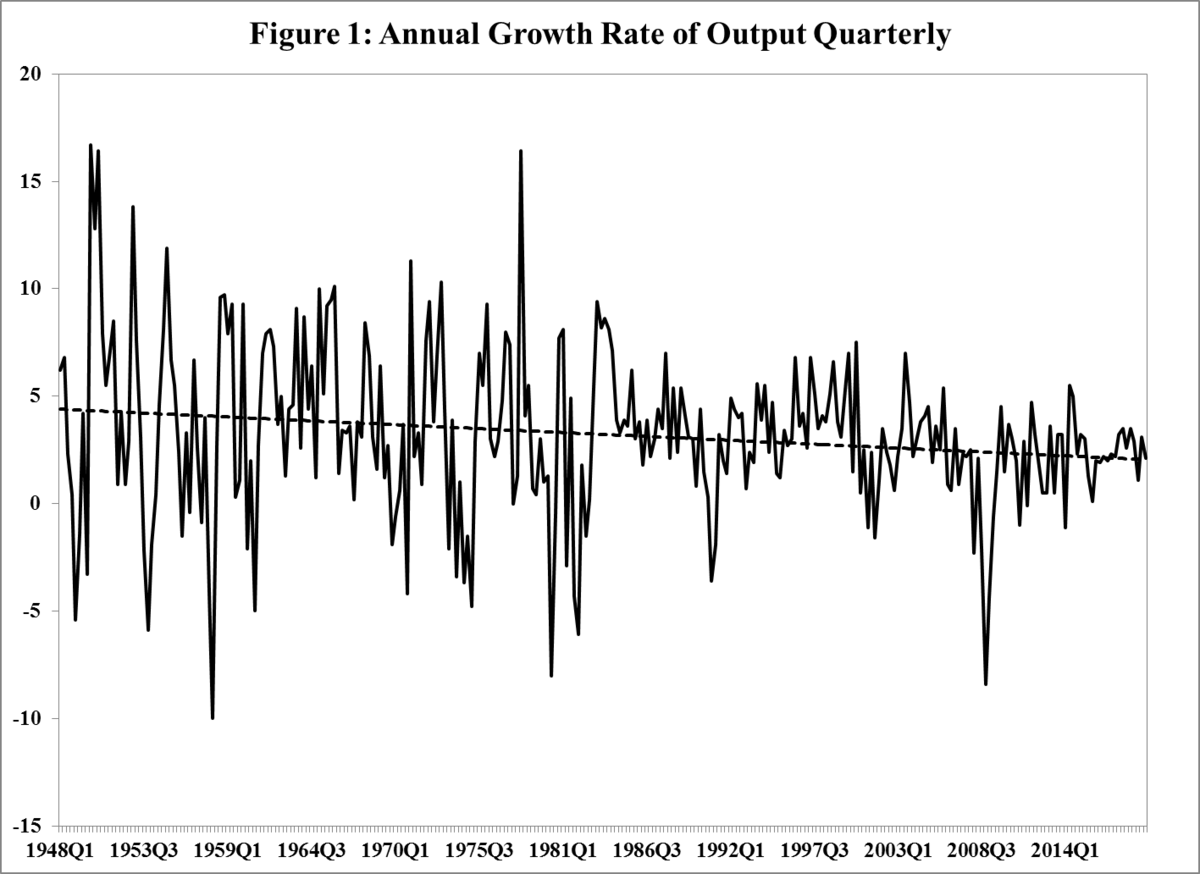

Figure 1, shows the annual growth rate of real GDP from 1948Q1 to 2019Q2. Note that swings in output growth were less frequent and less severe from the early 1980s to the onset of the recession in 2007. Economists refer to this period as the Great Moderation, but have failed to explain exactly why it happened. Figure 1 also shows a trend line based on data from 1948Q1 to 1994Q4 and extrapolated to 2019Q2. Since, 1994Q output has grown at the same trend rate as before.

To better understand why output growth has been trending down it is useful to realize that output is determined by labor, capital (plant & equipment) and the efficiency with which labor and capital are used to produce the output, which is called productivity. Aggregate productivity is difficult to quantify, but a frequently used is output per hour of labor.

Figure 2 shows the growth rate of this measure from 1948Q1 to 2019Q2. As is the case for output, the growth rate of productivity has declined since the late 1940s—from 2.4% in 1948Q1 to 1.1% in 2019Q2.

The decline in productivity has been accompanied by decline in employment growth. Figure 3 shows the growth rate of non-farm payroll employment from 1939Q2 through 2019Q2. Employment growth has been trending down since the early 1940. Given the trends in productivity and employment growth, it is hardly surprising that output growth is trending down as well. Employment and productivity are essential for output. It is difficult for output to growth rapidly without similarly rapid growth of employment and/or productivity.

The Mid-1990s Productivity Surge

Figure 4 shows the downward trend in output growth from the perspective of the level of real output. The figure shows real output from 1948Q1 to 2019Q2 and a quadratic trend line based on real output from 1948Q1 to 1994Q4 and extrapolated to 2019Q2. Output was growing along the trend line until the mid-1990s when it increased dramatically above trend until the 2007-2009 recession, when it decline precipitously. Output essentially returned to the trend level in 2009Q2 when the recession ended. Output was slightly above the trend line owing to the fact that output was way above trend from 1995Q1 to 2007Q4.

This surge in output was the consequence of exceptionally strong productivity during this period. Figure 2 shows that productivity growth was above trend from 1995 through 2005—for much of this period, substantially above trend. The increase in productivity coincided with advances in technology and the launching of the World Wide Webb in 1991.

Other factors, such as wide-spread use of securitization and other financial innovations, and a large increase in residential construction and supporting infrastructure, fueled by marked decline in lending standard and lax oversight of the mortgage market, also contributed to this anomalous rise in output. However, the increase in output would have been much smaller without the significant increase in productivity.

My conclusion is that the negative trend in economic growth is caused by similar negative trends in productivity and employment. Factors such as the decline in the education of our citizens (especially in math and science), the aging population, the transition from a manufacturing to a service economy, and a dramatically enlarged safety net may have contributed to the decline in employment growth and, to a lesser extent, in the decline in productivity growth. But it’s impossible to know the relative importance of such factors.

In any event, I believe it will be impossible to permanently increase the growth rate of output much above 2% or so without reversing the trends in productivity and employment growth. But there is little governments can do to increase the growth rate of productivity beyond supporting research and development, and fostering an economic environment that supports and rewards private sector initiative and innovation.

As for employment growth, the best thing a government can do is to have a policy promoting the immigration of a large number of intelligent hard-working people. Absent a marked increase in productivity growth, immigration is the only thing that can significantly increase economic growth.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor piece written by Dr. Daniel Thornton. During his 33-year career at the St. Louis Fed, Thornton served as vice president and economic advisor. He currently runs D.L. Thornton Economics, an economic research consultancy. This piece does not necessarily reflect the opinion of Hedgeye.