Position: Long Germany (EWG)

With Europe’s €750 Billion loan package facility headline news (and rightfully so), below are two incremental charts we’re looking at.

1. Piling on Debt, has consequences, including inflation. While Europe’s loan package mutes the immediate term threats of contagion across Europe, it does not excuse Greece (or the other PIIGS) from issuing the necessary austerity measures to cut its deficits.

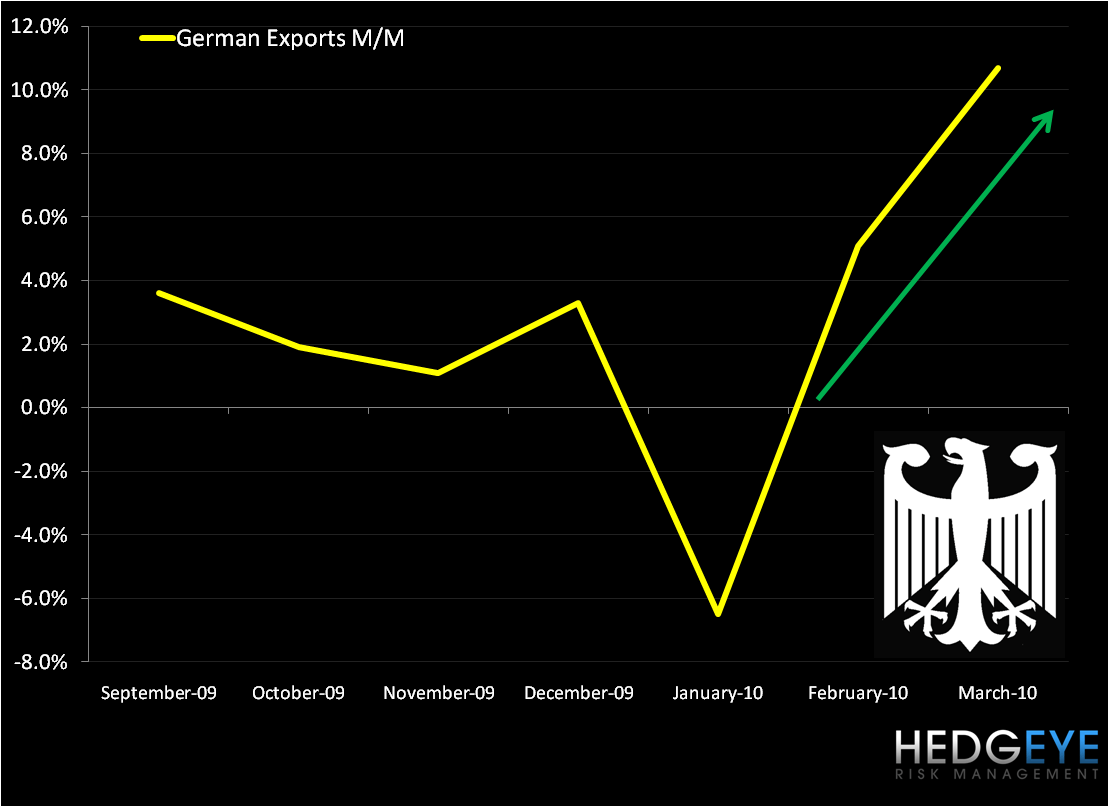

2. German exports received a boost in March, rising 10.7% versus the previous month. As part of our Q2 Theme Sovereign Debt Dichotomy, we’re bullish on Germany, especially as a weaker Euro benefits exports.

Matthew Hedrick

Analyst