This commentary was written by Dr. Daniel Thornton of D.L. Thornton Economics.

In response to my previous essay (here), a very good friend of mine, Peter Clark, commented:

|

The Fed has been using the federal funds rate as its policy instrument since May 1988, according to your analysis, and there was little talk of the politicalization of the Fed until Trump came on the scene and has attempted to dictate monetary policy. Thus, what has changed is the appearance of Trump, not targeting the funds rate as the policy instrument. Moreover, you agree that this is the Fed’s only option. Finally, I do not see how your ERMP solves the problem, as Trump, for example, could still berate the Fed to stimulate the economy to enhance his chances of reelection. The only solution is to get rid of Trump. |

Peter is correct in saying nothing could prevent Trump from criticizing the Fed. That’s what Trump does. Historically, presidents have worked behind the scene to influence the Fed. However, Trump has taken influencing the Fed to an entirely new level, which could ultimately harm both his presidency and the Fed.

The belief that the Fed can move interest rates up or down at will provides Trump with a broad base of supporters. They applaud his efforts to lower interest rates, even if some don’t approve of his method. Trump would find less support if the public didn’t believe the Fed can move interest rates—a belief that the Fed has done more to promote than discourage.

Trump’s attack would be more difficult and less effective had the Fed continued to operate as it did before it adopted the federal funds rate as its policy instrument in the late 1980s. So I stand by my claim that the Fed’s adoption of the funds rate as its policy instrument opened up the Fed to more political pressure.

As for Peter’s statement that my suggestion that the Fed adopt what I call economic-reality monetary policy (ERMP) would not end Trump’s criticism, I totally agree. Nothing will stop him. Nevertheless, I do believe ERMP would reduce the number of his supporters and provide what Stanford University economist, John Taylor, calls rule-like monetary policy. ERMP will produce more rule-like monetary policy without adopting a specific numeric policy rule as suggested by Taylor and others. [Taylor and other prominent economists have signed a letter in support of Section 2 of the Fed Oversight Reform and Modernization Act (H.R. 3189), which passed the House of Representatives on November 19, 2015, and would require the Federal Open Market Committee (FOMC) to adopt a specific numerical monetary policy rule]. In the chapter I’ve written for the Oxford Handbook of the Economics of Central Banking, I point out that no central bank has ever adopted a numerical policy rule and present several reasons why none ever will.

To better understand my ERMP proposal and how its adoption will provide more rule-like monetary policy, it is helpful to recall that there was a time when the Fed and most economists believed that interest rates were determined by the supply and demand for credit.

Most also believed that the Fed’s influence on the supply of credit was so small that its actions had little, if any, effect on interest rates generally. This view all but vanished when the Fed adopted the federal funds rate as its policy instrument and became increasingly open about its target.

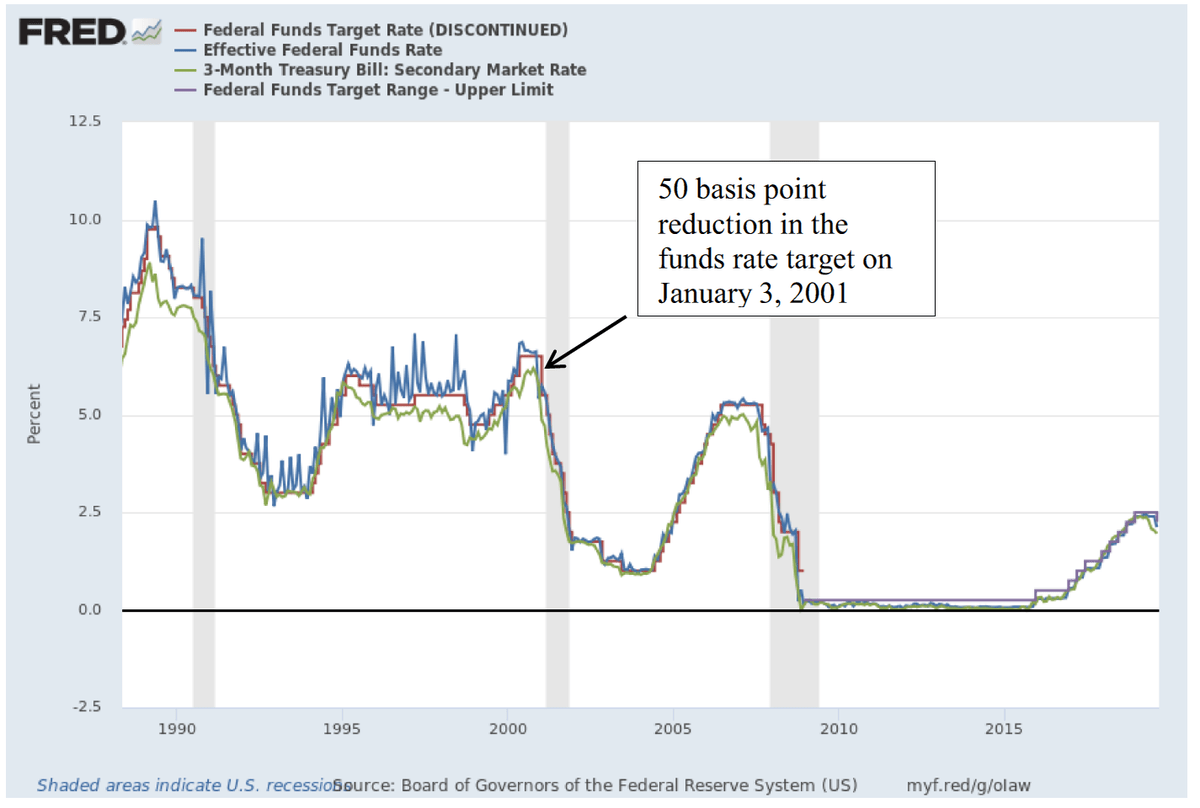

The Fed became completely open about its funds target in its June 2000 policy statement when, for the first time, it said it was “keeping its target for the federal funds rate at 6-1/2 percent.” Prior to this announcement, the Fed was intentionally vague about its funds rate target.

With the ambiguity eliminated, the funds rate moved immediately with target change announcements. This is shown in the figure below which shows daily data for the FOMC’s funds rate target through December 15, 2008 and the upper limit of the FOMC’s target range since December 16, 2008, the federal funds rate, and the 3-month T-bill rate.

The first target change after June 2000 occurred on January 3, 2001, when the FOMC announced a 50 basis point reduction in its federal funds rate target. The figure shows that since then the funds rate has moved immediately with the target. Other short-term rates, such as the 3-month T-bill rate, also have tended to track the federal funds rate closer.

My ERMP would allow the FOMC to continue to use the federal funds rate as its policy instrument. However, it would not be able to put the target too high or too low for too long. Specifically, I propose that two fundamental economic principles that most economists still believe guide the FOMC’s policy decisions: (1) credit is most efficiently and effectively allocated by the market, and (2) actions taken by the FOMC to affect interest rates necessarily distort interest rates and the allocation of both credit and economic resources. Credit and, hence, economic resources can be misallocated if the FOMC sets the target too high or too low for too long.

Concern about the effect of the FOMC’s interest rate targeting on the allocation of economic resources was raised at the March 2004 FOMC meeting. The FOMC had reduced its target to the then historically low level of 1% at its June 2003 meeting.

At the March 2004 meeting Federal Reserve Board vice chairman, Don Kohn, and other FOMC participants were becoming concerned about the effect of the abnormally low rate on the allocation of resources. Kohn noted:

|

Policy accommodation—and the expectation that it will persist—is distorting asset prices…We have attempted to lower interest rates below long-term equilibrium rates and to boost asset prices in order to stimulate demand. But as some members of the Committee have been pointing out, it’s hard to escape the suspicion that at least around the margin some prices and price relationships have gone beyond an economically justified response to easy policy. House prices fall into this category… If major distortions do exist, two types of costs might be incurred. One is from a misallocation of resources encouraging the building of houses, autos, and capital equipment that won’t prove economically justified under more-normal circumstances. Another is from the possibility of discontinuities in economic activity down the road when the adjustment to more-sustainable asset values occurs. |

Kohn’s remarks had little effect. The FOMC kept the funds rate target at 1 percent until June 2004 and then proceeded to remove the “policy accommodation” at a slow pace. Specifically, it increased the target 25 basis points at each of the next 17 meetings, so that by July 2006 the target reached 5.25 percent.

While I don’t believe the Fed’s excessively low interest rate policy is solely responsible for the financial crisis and the accompanying recession, there is no doubt that it was an important contributing factor.

If the FOMC had committed to conduct its interest rate policy in accordance with the two economic realities I propose, it would have been reluctant to keep the target at 1% for a year. Moreover, it wouldn’t have engaged in its quantitative easing (QE) program with the expressed purpose of allocating credit to specific markets. Nor would it have kept its funds rate target at zero 6.5 years into an economic expansion.

During normal times, the Fed would simply adjust its target up or down with changes in market rates. The FOMC could tell the public when it is changing its funds rate target simply to keep its target in line with the market or adjusting the target for policy reasons.

Knowing that the Fed would conduct monetary policy in accordance with these realities, market participants would understand that the Fed won’t keep the target too high or too low for too long. Watching the FOMC’s behavior over time, the public would learn to anticipate when the FOMC will start moving the target back in line with the market when the target has been changed for policy reasons. Hence, ERMP will make the Fed more predictable and, hence, make monetary policy more rule-like.

Of course, as Peter pointed out, ERMP would not prevent Trump from criticizing the Fed. But nothing can prevent that.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor piece written by Dr. Daniel Thornton. During his 33-year career at the St. Louis Fed, Thornton served as vice president and economic advisor. He currently runs D.L. Thornton Economics, an economic research consultancy. This piece does not necessarily reflect the opinion of Hedgeye.