Below is a brief excerpt transcribed from a recent edition of The Macro Show hosted by CEO Keith McCullough. The below explains why share buybacks hit an all-time high of $806.4 billion in 2018.

At Hedgeye, when we make fun of “stahks” and the U.S. stock market, it's because this industry has made many, many people rich by selling investors on the idea to "just buy stocks," whether that be brokers, bankers, and fund managers. We have designed an entire economy on making rich people richer. It's not like this everywhere else in the world. That’s why I call it a uniquely American FOMO.

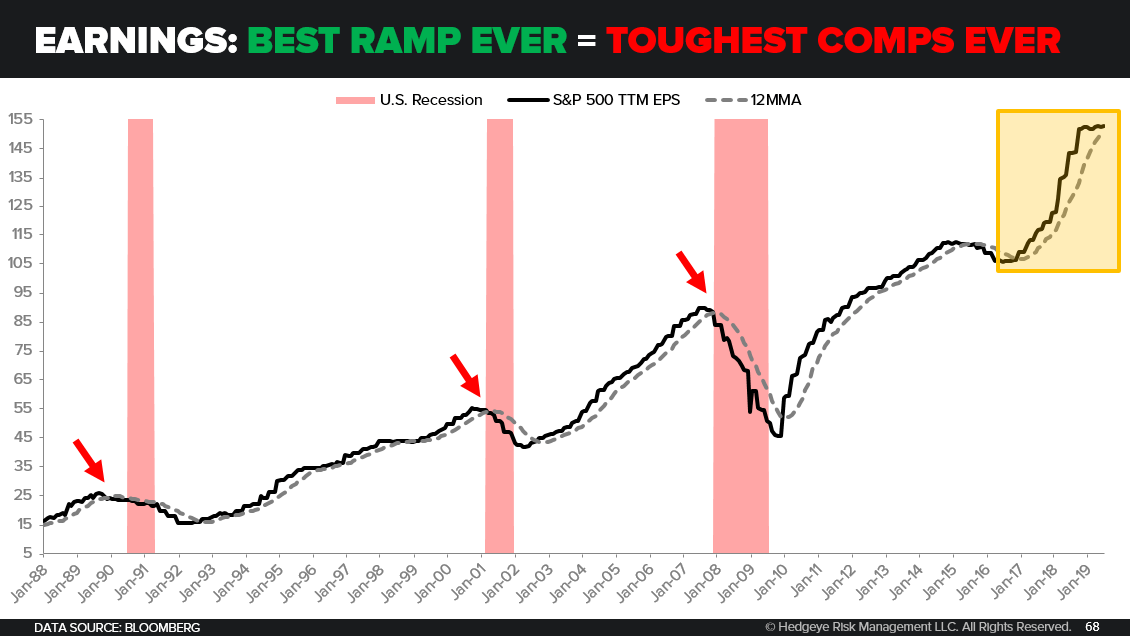

This is all part of U.S. economic cycle dynamics too. And that’s why you have company executives who say, “We have earnings at the highest point in US history. I've got a lot of cash. Maybe I’ll buy back the stock or, moreover, maybe I’ll go lever up and buy back the stock because I know there's demand.”

So when you have S&P 500 trailing twelve month earnings at all-time highs, CapEx and buy backs rip alongside that procyclically. You can see all of these things are interrelated.

What do you think happens when earnings slow? You see, all of this works both ways.

The entire industry is stacked up to perpetuate these dynamics. The average tenure of a CEO for a company in the S&P 500 is less than 5 years. That’s not long term, that’s pay me now! We know the culture. We know what it is when we say FOMO.

Moreover on the buy side, there is a putrid level of performance going back 3, 5, 10 years. People are under the gun and its career risk management 101 to chase. That is uniquely American.