“Prediction is very difficult, especially when it is about the future.”

-Niels Bohr

Keith has taken his young lad, wife, and daughter up to his ancestral home of Thunder Bay, Ontario, so I’ve been handed the baton on the Early Look. In a similar spirit, I thought I’d quote someone from the land of my ancestors, Denmark.

One would think that Niels Bohr was a Danish version of Yogi Berra given the quote above. In fact, Niels Bohr was a physicist. Well, much more than a physicist really, Bohr was the Nobel Prize winner in Physics in 1922 for developing the Bohr model of the atom.

The man basically discovered how the most discrete parts of life work, and for such fine work his home country put him on a postage stamp, put him on the 500 kroner bill, had two elements named after him, and, get this, he even has an asteroid named after him. (As an aside, I’m starting to think my good friend and 12-time Olympic medalist in swimming, Jenny Thompson, got the raw end of the deal when she only got a swimming pool in her hometown named after her.)

Bohr also developed the principle of complementary, which states that “items could be separately analyzed as having several contradictory properties.” As we stare at our screens this morning trying to predict the future, this might have been his most valuable contribution.

While Europe is up small this morning, Asian got pounded over night. China is down more than 4% to a 8-month low and the Nikkei in Japan is down almost 3.5% (after a holiday earlier this week), its largest single day decline in over a year.

Yes, friends, the world is starting to have a freak out moment about sovereign debt. Global markets are getting pounded, Spain is seeing its cost of debt rise to levels not seen since the global financial crises of 2008, and Moody’s has piled on this morning saying contagion could threaten banks in “Portugal, Spain, Italy, Ireland and the U.K.”. While I woke up with a cold, the world, it seems, has Caught the Contagion.

When the world is freaking out though, it’s best to go back to science and facts when trying to predict the future. As it relates to the immediate term future, I’m going to focus on Bohr’s principle of complementary. These freak outs usually create the best buying opportunities, and within the European Union our favorite set up of long Germany and short Spain is one to focus on as they have “very contradictory properties”.

I’ve asked our European Analyst Matt Hedrick to provide a brief overview of some key economic metrics for these two countries, which are outlined below.

On Spain:

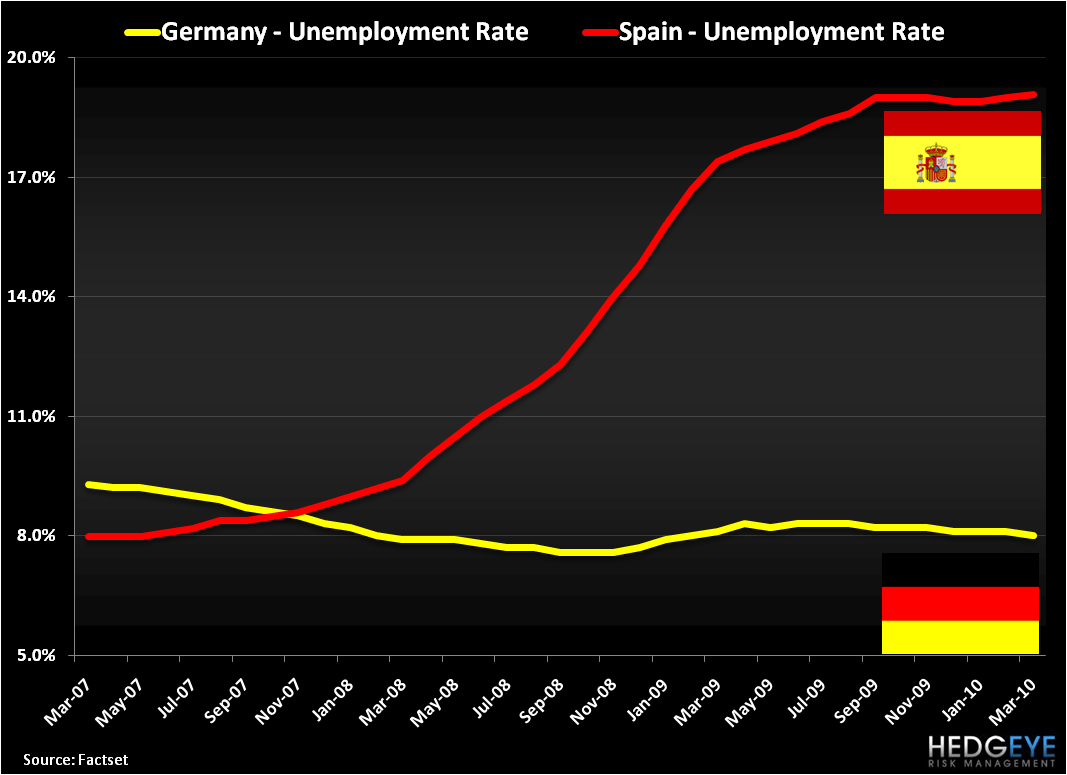

- Spain’s unemployment rate is north of 20%, which is almost 2x the EU average. The unemployed consists largely of recent immigrants (unemployment rate closer to 35%) and construction workers, which will be difficult to re-employ, and thus will keep unemployment high for some time.

- Spain’s budget deficit-to-GDP was 11.2% at the end of last year and has expanded this year. This is well beyond the danger zone of 10%, which typically highlights the increased potential for a debt default and increased borrowing costs.

- Spain’s economy at its peak was more than 20% driven by construction and real estate, which will not rebound any time soon. As a result, growth in the “recovery” has been anemic and GDP is expected to decline -0.4% in 2010.

On Germany:

- German unemployment has held steady in the low 8% level over the past 12 months, with recent improvement coming in last two months, falling to 8.0% in March and 7.8% in April. This outperformance over the Eurozone average (currently at 10%) is due to the success of the government’s short-time work program (Kurzarbeit), which buffered the impact of the economic downturn on unemployment.

- Germany’s budget deficit stands at 3.5% of GDP. We see this low figure as an extreme advantage, especially as the cost of capital rises for European states over the medium term.

- The decline of the Euro versus the USD stands to boost Germany’s large export base. Year-to-date the Euro is down 10.8% versus the USD. While GDP is forecast to grow under 2% this year, we expect Europe’s largest economy to outperform, especially as many of its peers are mired in sovereign debt.

While the points above are somewhat of a science in and of themselves, we’ve also represented this Sovereign Dichotomy in our Chart of the Day attached below. This chart outlines the divergences of unemployment in the two countries. Spain’s unemployment parallels that of economic leaders like Sudan and the West Bank, while German unemployment is amongst the lowest in the industrialized world and improving.

When the world Catches the Contagion, volatility will spike (as it has) and investors sell stocks, assets classes and countries indiscriminately. A quick application of Bohr’s principle of complementary tells the science-fearing team at Hedgeye one thing, not all members of the European Union are created equal.

“Prediction is very difficult” . . . especially when we make it so.

Keep your head up and stick on the ice,

Daryl G. Jones

Managing Director