Management struck a satisfied but cautious tone during the conference call.

Led by extremely strong top and bottom line results, DPZ posted an extremely strong quarter yesterday that had largely been priced into the stock which, before yesterday, had run up over 90% YTD. Over the past couple of years the company has contended with softer consumer environments and high inflation in food costs. Of late, consumer spending has been stronger and personal consumption expenditures have rebounded strongly on a year-over-year basis. Additionally, while the commodity basket was up 4.1% for DPZ during 1Q, the company is not significantly exposed given contracts currently in place with suppliers.

It was interesting to note that, even with the company maintaining cheese guidance of $1.50-$1.70 per pound for later in the year, there seem to be no plans to adjust pricing. Promotions such as “two medium two-topping pizzas for $5.99 each” have proved profitable, according to management’s commentary, once “Coke, chicken and bread size” are included.

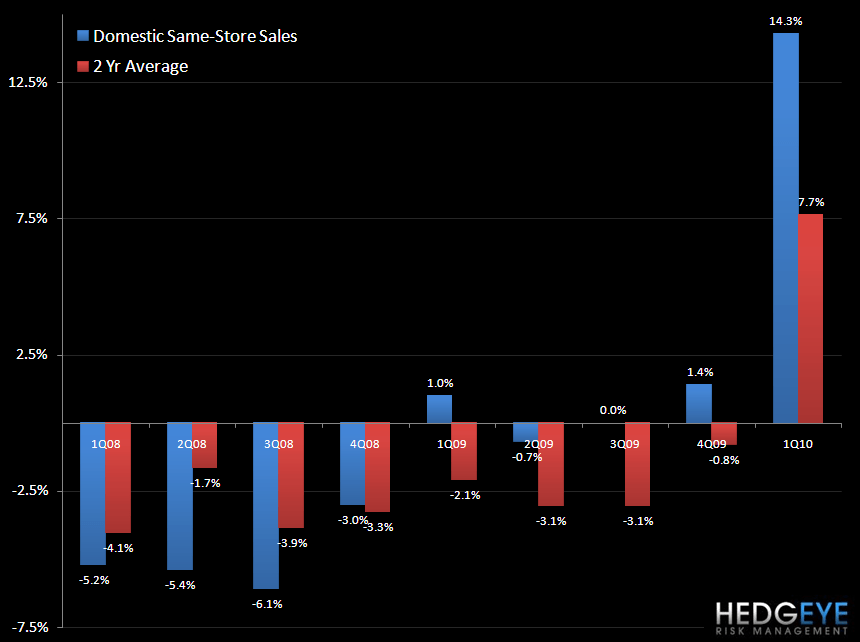

Later in the call, a discussion of comps revealed that the +14.3% domestic comp was driven exclusively by traffic, with check “slightly down”. Clearly any move injurious to comps would be a mistake for DPZ and the two obvious drivers of traffic were promotions and the new advertising campaign which, management said, had a high correlation with the sales improvement. The company emphasized the new pizza as the key driver of trial and repeat customers this quarter but long-term guidance being maintained at +1% to +3% for domestic comparable store sales, despite the +14.3% growth in 1Q10, seems to have been insufficient to maintain investor confidence in the stock’s run (traded down nearly 13% yesterday). FYI, the 14.3% domestic comp was versus +1.0% in 1Q09. The quarterly comps to hurdle for the remainder of the year (-0.7%, 0.0%, and +1.4% for 2Q09, 3Q09, and 4Q09, respectively) are in line with those lapped so successfully during the just-reported quarter so guidance assumes a significant deceleration in trends.

Specifically, management said, “we’re certainly expecting solid results in the second quarter. This is a company that had 12 years without a negative comp … But we feel very good about getting back to consistent, positive comps as a company in our domestic business. Not only did we have good trial on this new pizza, but our repeat numbers were great, our frequency has increased. There was strength across all consumer metrics. So, we feel very good about where we are. All of that said, our long-term guidance remains positive comps of 1% to 3% on the domestic business.” Beyond that, management wouldn’t get into specifics when questioned further on trends in 2Q.

DPZ Notes from the earnings call

- Strong start to the year

- EPS up 75% yoy on broad-based performance

- Business is stabilized and company is poised to develop well

- US momentum

Performance

- Global retail sales grew 17.4% incl. FX

- Robust domestic SSS growth

- Strong int’l SSS growth

- Int’l store growth

Domestic

- One of the best quarters ever

- SSS +14.3% vs +1% in 09

- Franchise up 14.2%, company 14.7%

- Closed 17 stores

- Shifting towards opening

- Ending 2010 with flat domestic growth

International

- 54 new stores

- SSS +4.2% constant dollar vs +6.6% in ‘09

Total revenues

- Up 18.4%

- All operating divisions saw revenue growth

- 2/3 of revenue increase attributable to supply chains

- Higher volumes due to new pizza

- Higher royalties

- SSS and store count growth

Operating margin

- Increased 70 bps vs last year

- High volumes QoQ

- Offset by higher cheese and meat prices

- Company owned margins increased 1.4% YoY

- 20%+ margin levels at company owned stores

- Labor and occupancy costs dropped as a results of the increased leverage due to higher volume

Commodity

- $1.44 vs 1.23 last year for cheese

- Some predicting increases/decreases…we see $1.50 to $1.70 range by end of year but not apparent yet

- Supply chain margins benefitted from product mix changes, offset by higher commodity costs

G&A

- Increased due to strong operating performance

- Bonuses and expenses

Income tax

- 38% this quarter

- 39% will be normalized tax rate

EPS

- $0.41 (or $0.35 adjusted)

- Improvement is from

- Lower interest expense

- Foreign currency ($0.02)

- Lower tax ($0.01)

- Higher share count negatively impacted

Balance sheet

- Bought back and retired ~$60m of principle on outstanding fixed rate senior notes at a discount

- Leverage at 6.1x

- 28m unrestricted cash

- 27.4m of FCF in 1Q

- Anticipating improving FCF on 2009

SSS increase is unprecedented

- MCD posted a similar comp in 1Q04 at the beginning of a strong period for their business

- Rare pace of sales growth is not something expected to continue at this level

- DPZ responded to critics and produced an improved product

Trends

- Suburban and high income customers coming on board

- Online ordering nearing 25% of sales

- Transparency has won a lot of custom and positive PR

Lessons learned

- No tolerance of poor operators in system

- Weeding out franchisees that won’t operate at the higher level

- Reduction of store closure speaks to progress on that front

International

- Retail sales will surpass domestic sales in just a few years

- Want to nearly double the top ten international store counts internationally

- International was 34% of operating income in 2009

- Only YUM, MCD and BKC’s international businesses contributed more

- International DPZ is larger than the system of any of its competitors

India

- Potential is strong

- Demographics are favorable

- 1.2 billion people

- DPZ is the largest QSR brand there

- Median age is 25 vs 34 in China

- Economy growing at high single digit rate

- Great franchisee in that market

Bain Capital has done some distributions recently that brought down their holdings

- No surprise to see them continue to distribute these shares

- Recently bought into the master franchise project in Japan

- Distributions were easily absorbed by demand

Q&A

Q: Sales outlook? How is the category growing? Taking share from frozen pizza? Dynamics besides the new pizza launch that may be driving comps?

A: Expecting solid results in 2Q, repeat numbers were great, frequency picked up, strength across all consumer metrics. Long term guidance remains 1%-3% on domestic business. Unclear if there is share being taken from frozen. Category has some weakness in ’08 and ’09 and some of this is recapturing those consumers. Pizza is the fastest growing category vs the rest of the restaurant industry at the moment

Q: Weather impact?

A: If weather had any impact, the new pizza overwhelmed that impact.

Q: Comment on day part/day of week/geographies?

A: More strength in dinner day part. Lunch and sandwich business all held up well. Relative strength in dinner part versus a sea of strength! International markets at 4.3% vs long term guidance of 2%-3% shows that we were strong really across the board.

Q: Flat unit growth…with the improving unit economics your seeing are you getting more interest from possible franchisees?

A: the improving results are encouraging, particularly for existing franchisees. The vast majority of growth going forward is going to come from existing franchisees.

Q: Commodities?

A: Not seeing serious pressure – margins are up, sales are up, feel good about unit economics… we’re still running the same promotion that was started at the start of December.

Q: In light of earnings growth, any thoughts on share repurchase?

A: Near term we’ll continue to buy back debt. FCF at 1.5m per week rate…we’ll continue to buy back debt and will be focused on returning best returns possible for the shareholders. We think that’s the right strategy right now.

Q: Other platforms, sandwiches?

A: These new platforms, like American Legend, have provided higher price points and the American Legend offers room for customers to trade up. Although that’s been the focus of conversation, other platforms have done well.

Q: Sensitivity of cheese to earnings?

A: looking at commodities being stable. For the quarter, basket up 1.1%. cheese is most significant. Inventories and production are up. Maybe cheese will hit the $1.50 to $1.70 range in back of year but not seeing it. Wheat, meat and poultry all look stable.

Q: Check was down? Comment on check and traffic mix, please.

A: It was all traffic. We drove a lot of traffic. Check was slightly down and all of the growth was from traffic.

Q: On G&A line, in January you saw a pickup in G&A, did a fair amount of that go in 1Q or is it going to be loaded in 2Q?

A: 3m of G&A and offset in revenues…call center is an example. Primarily front loaded to first half. The 1Q increase is related to sales growth and sales awards and incentives and bonus plan.

Q: Marketing…any unusual laps?

A: Strong all year, we had franchisees commit to a new contract that started on January 1 that moves spend to 5% of sales. Record weeks on air this year.

Q: Considering how to spend your cash going forward?

A: We’re seeing the results of previous investments. This is the best quarter a major US QSR chain has had. The sales boost puts a lot of pressure on capacity and the system coped very well.

Q: International opportunity to invest more equity? Given growth and scale would the company not look to put equity in international markets?

A: Never say never, but we like the model we have.

Q: Advertising in Q1, was there a high correlation between sales improvement and spend? Is 1Q heavier in terms of advertising?

A: The day we went on air we saw an increase in sales, so consumers reacted quickly. Advertising clearly worked. It will continue to be strong through 2010.

Q: Online sales were at 25%? Does it have a higher average ticket…with ticket down, why was that if online sales increased by 5% as % of sales versus 4Q?

A: Online sales were up by almost 5% and it continues to grow. Skews heavily towards delivery. It does have a higher ticket than phone or carry out sales but there are higher levels of customer satisfaction when orders come through online.

Increase in sequential online sales by 3/4% but on a year over year basis the impact on check isn’t that big.

Howard Penney

Managing Director