R3: REQUIRED RETAIL READING

May 5, 2010

TODAY’S CALL OUT

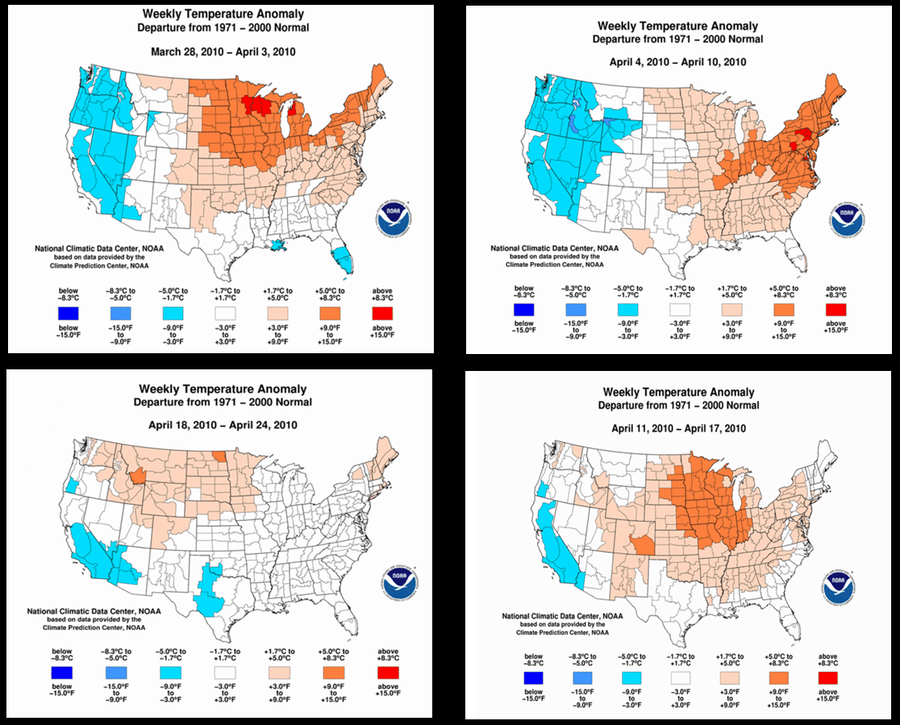

March’s strong sales results, which resulted from a near perfect confluence of positive events (great weather, tax refunds, easy compares, Easter shift, pent-up demand , etc…) inevitably make for difficult comparisons when tomorrow’s April sales are reported. There’s no question that results will appear to have slowed this month and we’re already seeing some rumblings as to why. We’ve seen weather being used recently as an excuse, especially in the golf sector. So, in advance of tomorrow’s releases, we want to make sure we at least get facts straight on the meteorology. It is clear from the weekly trends, that there was a divergence between cooler weather on the West coast and warmer weather on the East coast. What this amounts to is a little bit of something for everyone. Those with a national footprint may actually net out to “normal” weather exposure, while those with West coast exposure are likely to express the “blues” .

Eric Levine

Director

LEVINE’S LOW DOWN

- Amidst the flurry of congratulatory comments on the True Religion conference call, a subtle detail may have been overlooked. The company’s same-store sales, which were only released for the second time (given the inherent youth of the store base), slowed sequentially in 1Q10. With a comp base of 46 stores, same store sales increased by 18.7% in the quarter vs. 22.3% in 4Q09 (36 store base). Interestingly, same store sales including e-commerce were 18.2%, indicating that the .com platform was negative for the quarter.

- Despite a normal seasonal shift, Steve Madden noted that boots and booties were a strong category in the recently reported Q1 results. Given the strength, AUR’s were strong in the quarter. Overall booties made up 52% of the company’s mix in the quarter, up 1100 bps year over year. Given this strength and the strong order book for deliveries slated for 6/25 and 7/25 management is confident that boots will remain strong through the Fall. However, the company is not planning as aggressively for the category given last year’s very strong results.

- It’s important to know where the competition stands, especially in the global athletic footwear environment. On yesterday’s Adidas conference call, management stated, “On market shares when we talk about market share then we mainly talk about market share within our main competitors [like] Nike. Nike is in the first half growing faster than us because they started earlier to clean [up their business and inventories].” Recent sell-side concerns about Adi’s success at the expense of Nike were clearly overblown.

- It’s hard to believe that Dr. Martens may be making a stateside comeback, but the opening of the brand’s first NYC outpost may be a starting point. After celebrating the brand’s 50th anniversary by giving away free shoes at the London store, this may be the first credible attempt to revive 90’s fashion.

HEDGEYE CALENDAR

MORNING NEWS

USITC Investigation Could Lead to Higher Duties for Certain Footwear with Textile Outsoles - The USITC has conducted an investigation under Chapter 64 relating to certain footwear featuring outer soles of rubber or plastic to which a layer of textile material has been added. These changes would reflect decisions on the classification of that particular footwear. If the proposed recommendations are accepted by the USITC and green-lighted by the president, foreign footwear manufacturers would no longer be able to use glued on/slapped on and appliqué textile outsoles to lower the duty rates on several footwear items, including 19 types of rubber/fabric and plastic/protective footwear that are still manufactured in the United States. This footwear would be classified under heading 6404 (footwear with outer soles of rubber, plastics, leather or composition leather and uppers of textile materials) with duties ranging from 20% to 67.5% instead of heading 6405 (other footwear) with duties ranging from 7.5% to 15%. <fashionnetasia.com>

Web Shoppers' Experiences Improved - According to the latest survey from research group ForeSee Results that monitors 100 internet retailers, web sellers mostly garnered more positive ratings than they did a year ago, when many were in survival mode. This year, the poll’s composite score set a record high of 78 on the survey’s 100-point scale, up almost 5 points from a drop-off last year. L.L. Bean led among the 23 apparel and accessories retailers on the list with a score of 82 (80 and above is excellent), and was followed by Coldwater Creek Inc., at 80. Abercrombie & Fitch Co., Polo Ralph Lauren Corp. and the Victoria’s Secret unit of Limited Brands Inc. each logged a 79. In the mass merchant category, J.C. Penney Co. Inc., Kohl’s Corp. and Wal-Mart Stores Inc. all made the top 10 with a score of 80. Beauty firm Avon Products Inc. came in third in the overall rankings with a score of 83, while Web giants Netflix Inc. and Amazon.com Inc. took first and second, respectively. <wwd.com/business-news>

E-Retailers Top 500 Guide Take Aways - This year’s Top 500 Guide reveals several trends that emphasize consumers’ continuing shift to online buying and the shift to large retailers:

- The Top 500 retailers’ sales grew 8.7% to $126.38 billion in 2009 from $116.28 billion in 2008.

- Total traffic to the Top 500 increased 22.9% year over year to 2.58 billion monthly visits from 2.10 billion visits in 2008.

- Web sales now account for 6.5% of retail sales, up from 6.2% a year earlier.

- Web sales were the only growth area for most chain retailers( 26 of the 50 biggest chains)

- The Top 100 grew 11.6% and the retailers number 401 to 500 in the Top 500 Guide grew 2%, further evidence that a shift to bigger online retailers is taking place.

By category, last year’s results show:

- Combined sales for all top 500 web-only merchants grew year over year by 19.8% to $42.94 billion from $35.83 billion.

- Consumer brand manufacturers in the Top 500 grew web sales by 3.8% to $15.30 billion from $14.74 billion in 2009.

- Retail chains in the Top 500 grew combined web sales last year by 6.6% to $49.80 billion from $46.71 billion.

- Catalog companies posted a drop in sales last year, declining by 3.1% to $18.32 billion from $18.91 billion. <internetretailer.com>

Sears Making a Major Apparel Push - The mandate to turn around apparel was emphasized at the outset and underscored throughout the three-hours-plus shareholders meeting. Kmart is performing well with an apparel turnaround while moving to everyday pricing and significant improvements to the in-store experience. Revitalizing the Sears apparel brand is a top priority. New brands exclusive to Sears and Kmart, such as Bongo and Dream Out Loud with their younger demographic, will be key drivers. John Goodman, executive vice president of apparel and home, is building a new culture around apparel with significant talent. <wwd.com/business-news>

Athleta Opens 1st Store - Athleta, Gap Inc.’s online women’s sportswear and activewear company, is taking a first step into the world of bricks and mortar. Less than two years after Gap acquired Athleta for $150 mm in cash, the specialty retail giant will roll out the first Athleta test store in Strawberry Village Center in Mill Valley, Calif. The test store, which will be 2,424 square feet, is slated to open before the end of this month, said a spokeswoman at the Strawberry Village Center Mall. <wwd.com/business-news>

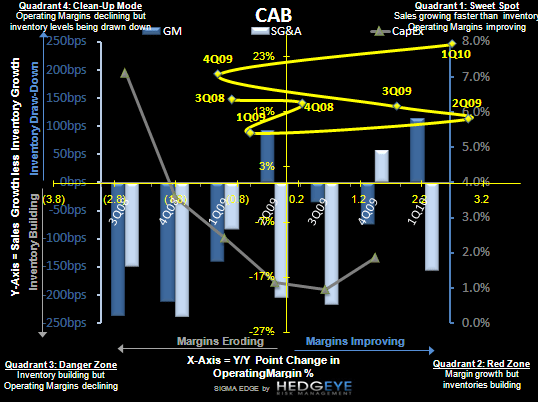

Cabela's Reports -1.7% Comps - Cabela's Incorporated reported total revenue for the quarter of 2010, adjusted for divestitures, increased 5.1% to $559.6 million; retail store revenue decreased 1.5% to $271.3 million; direct revenue increased 2.1% to $222.7 million; and comparable store sales decreased 1.7%. Cabela's Plans Stores for its third store in Texas and its first in Oregon. <sportsonesource.com>

Overstock.com Starts Off the Year with Stronger Sales and a Profit - For the first quarter ended March 31, Overstock reported an increase in revenue of 42.3%. Net income was $3.7 million compared with a net loss $4 million in the prior year. <internetretailer.com>

Girl Obesity Rises 2x Rate of Boys - The percentage of obese girls in the United States increased more than twice as much as the percentage of obese boys from 2003 to 2007, according to a study released Monday by researchers at the Health Resources and Services Administration. Potential tailwind for plus sized women's specialty retailers such as CHRS. <sportsonesource.com>

Guess COO Steps Down - Carlos Alberini has stepped down as president and chief operating officer of Guess Inc., the Los Angeles retailer and wholesaler, to become co-chief executive officer of Restoration Hardware, effective June 1. Alberini, 54, has been at Guess since December 2000 and has agreed to remain on the board at Guess for two more years. <wwd.com/retail-news>