THE HEDGEYE EDGE

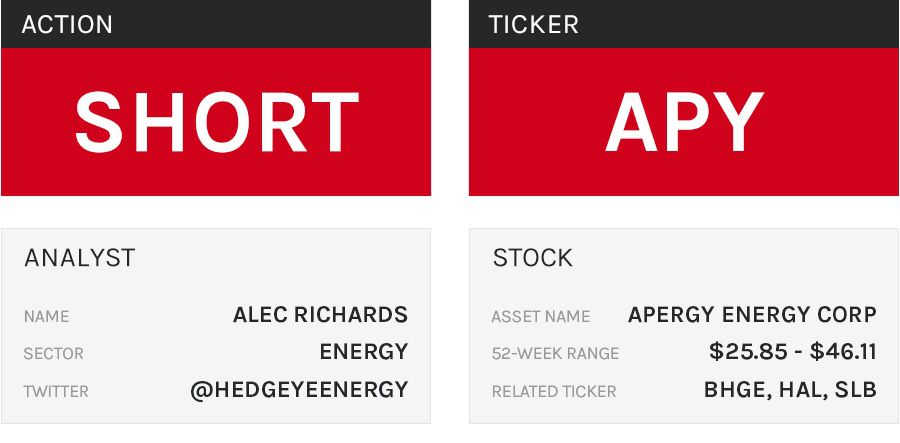

Apergy Energy Corp (APY) is a ~$3.0 billion EV oil field services company that was spun out of industrial conglomerate Dover Corp (DOV) in April 2018. Since the spin-off, APY has traded at a 2-3x premium to OFS peers and its market value has been resilient despite persistent weakness in OFS equities.

The company touts itself as a diversified, fast-growing business whose product lines are technologically advantaged, high margin, capital light, and less sensitive to oil field cyclicality. In our view, APY is just another cyclical, commoditized OFS company.

Artificial lift is the company’s most significant business driver. APY wants investors to focus on its technological advantage, but in reality, the company operates in a commoditized sector of the OFS universe. The company has no demonstrable technological advantage.

APY’s cyclicality will surface with bubbling macro headwinds. The E&P sector is being forced by the market, both commodity and capital, to rationalize spending. Focus on FCF over growth at the E&P level will hurt APY. Furthermore, estimates for overall E&P production growth continues to fall alongside lower rig count and E&P efficiency requiring fewer wells with artificial lift, a limiting factor for both APY segments.

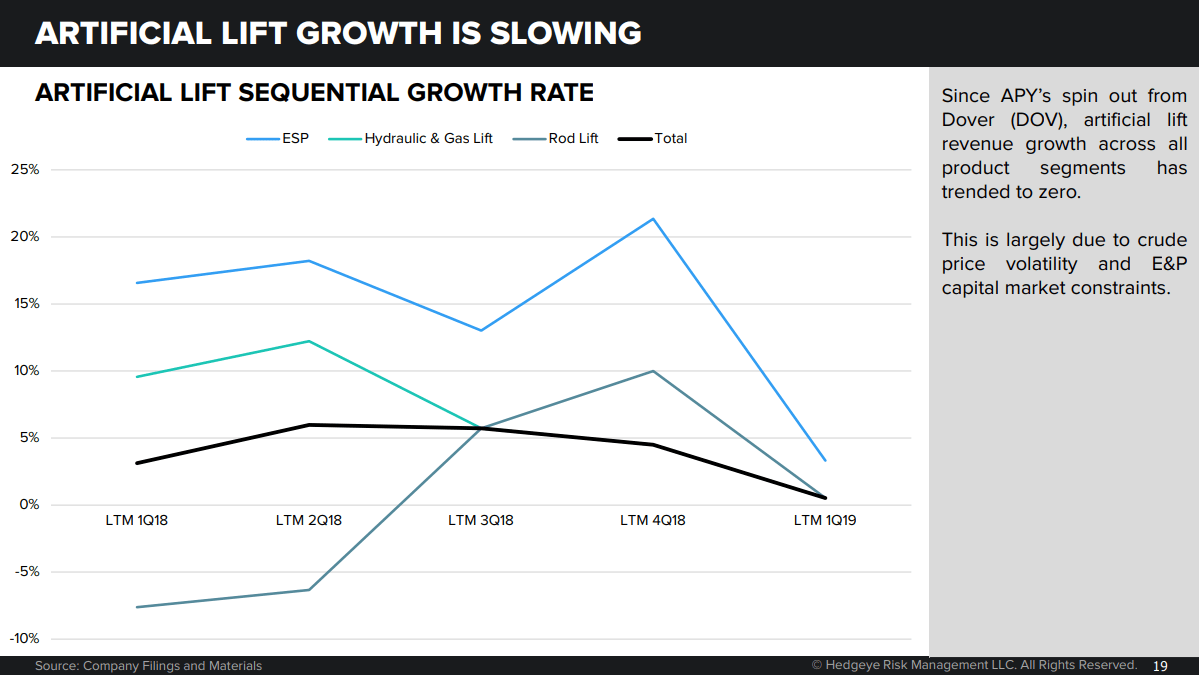

Since APY’s spin out from Dover, artificial lift revenue growth across all product segments has trended to zero. This is largely due to crude price volatility and E&P capital market constraints. APY’s spin pitch deck overestimated the market growth potential. Recent communication has been less clear, but more conservative.

The company is also behind in ESP and spending significantly to catch up. ESP margins are 5-6% lower than rod lift – i.e. APY is investing heavily in a lower margin product into a potential cycle hiccup.

Concurrently, key artificial lift leaders BHGE, HAL and SLB are all competing more aggressively in the marketplace.

In the most recent quarter, APY’s revenue was flat YoY. The artificial lift product line declined 3% YoY, significantly below its better capitalized peers.

Making matters more interesting, though, is that on its 2Q19 call Halliburton outlined a shift in strategy for a prolonged “change in our customers’ behavior.” The new strategy includes a significant reduction in CapEx, but most importantly, it transitions HAL’s focus from completion related business lines, where competition is intense, to production related business lines such as artificial lift. HAL entered the artificial lift market in earnest in 2017 with the acquisition of Summit ESP, which produces electronic submersible pumps (ESP’s) and largely operates in the Permian.

For financial context, HAL grew its artificial lift revenue by 55% from 1Q18 to 1Q19, and again called out the business line as a positive in 2Q19. During 1H19, APY grew revenue in its Production and Automation Technologies segment by ~1%.

We believe estimates for 2019-2020 will be revised down further with a reduced margin and revenue growth outlook. Another potential catalyst is if E&P’s hold flat or lower 2020 capital budgets vs. 2019.

Their current valuation assumes aggressive 10% growth in key businesses as well as continual margin expansion. We see fair value at ~$20-$25 per share, implying -20-30% downside from current levels.

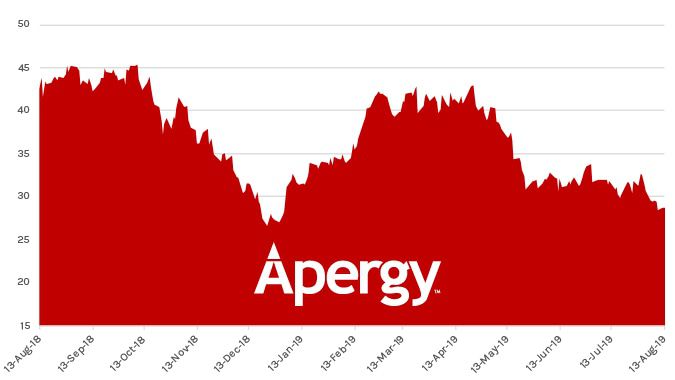

ONE-YEAR TRAILING CHART